Family Budgeting Tips: Complete Guide for 2024

October 20, 2025

Nearly 60% of families struggle to track their spending every month. Managing money can feel overwhelming, yet small shifts in how you plan can make a huge difference. Simple strategies help turn chaos into clarity, guiding your family toward financial stability and peace of mind. By understanding proven budgeting methods, anyone can start building smarter habits for a brighter financial future.

Key Takeaways

| Point | Details |

|---|---|

| Effective Budgeting is Collaborative | Involve the entire family in financial planning to foster shared goals and accountability. |

| Understand Your Financial Health | Use techniques like the 50/30/20 or 60/30/10 methods to effectively allocate income amidst changing economic conditions. |

| Track Spending and Adjust Regularly | Utilize digital tools to monitor expenses, allowing for timely adjustments to your budget. |

| Avoid Common Pitfalls | Sidestep frequent budgeting mistakes, such as neglecting small expenses and unrealistic expectations, to maintain a sustainable financial strategy. |

Table of Contents

- Understanding Family Budgeting Basics

- Popular Budgeting Methods Explained

- Key Steps To Building Your Budget

- Managing Expenses And Maximizing Savings

- Common Budgeting Mistakes To Avoid

Understanding Family Budgeting Basics

Managing family finances isn’t about restriction—it’s about strategic planning that gives you control and reduces financial stress. Budgeting is the foundational tool that transforms money management from a confusing maze into a clear roadmap. According to NerdWallet, determining your after-tax income and selecting an appropriate budgeting method are critical first steps in creating a sustainable financial plan.

Research reveals powerful strategies for balanced financial health. The “one-third rule” offers a mathematical approach to household financial planning, recommending equal allocation of income across three key areas: needs, savings, and debt repayment. This method not only provides structure but also significantly lowers bankruptcy risk. Different budgeting techniques can help achieve this balance:

- Envelope System: Physically or digitally allocating cash to specific spending categories

- Zero-Based Budgeting: Assigning every dollar a specific purpose

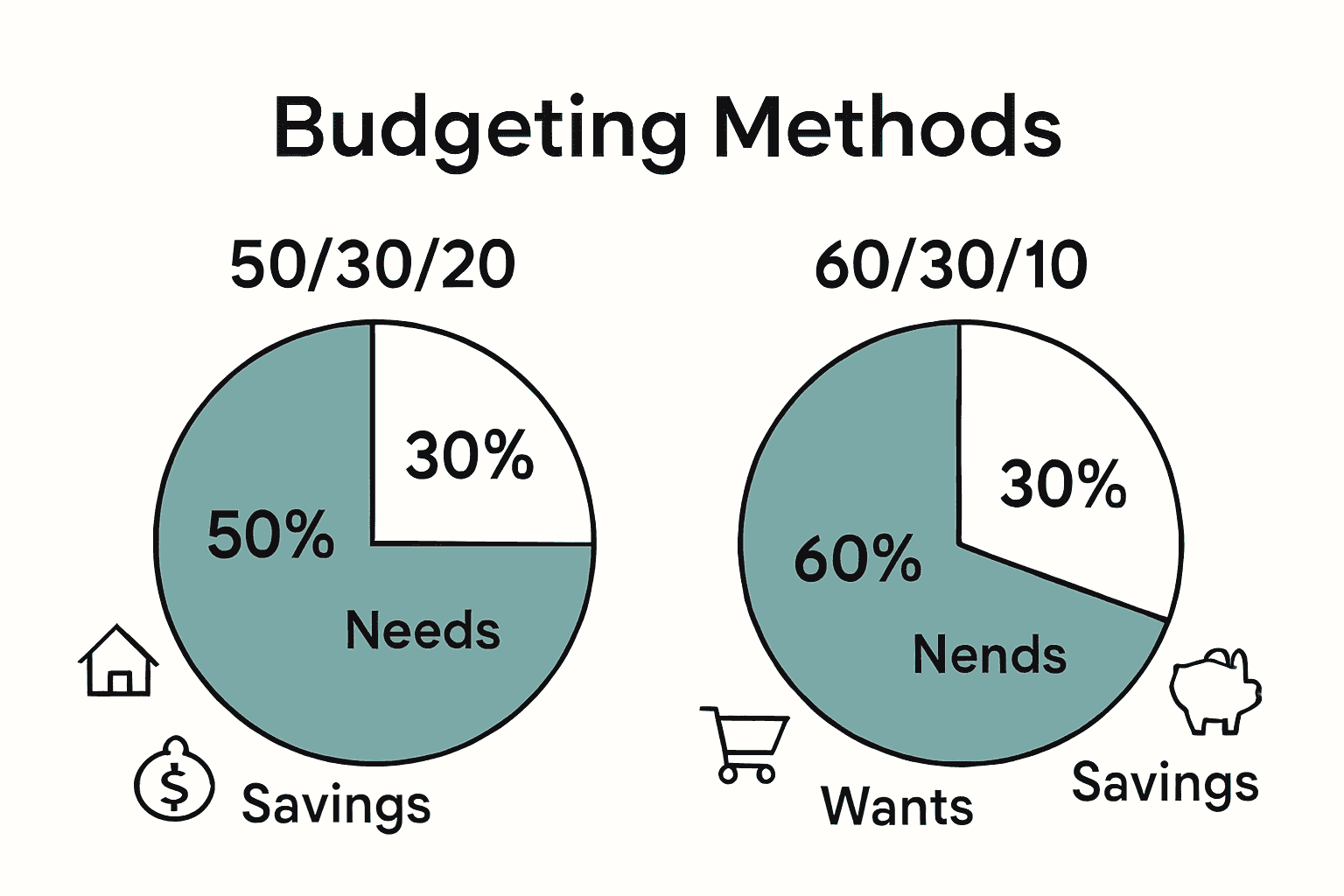

- 50/30/20 Method: Allocating 50% to needs, 30% to wants, 20% to savings and debt

Successful family budgeting requires consistent communication, flexibility, and a shared financial vision. Start by having open discussions about money goals, track expenses together, and regularly review your budget. Remember, a budget isn’t a punishment—it’s a powerful tool that empowers your family to make informed financial decisions and build long-term economic stability.

Popular Budgeting Methods Explained

Budgeting isn’t a one-size-fits-all strategy. Different methods can help families track spending, save money, and achieve financial goals more effectively. Each approach offers unique advantages that can be tailored to your specific financial situation and personal preferences.

One powerful method is Zero-Based Budgeting, where every dollar is assigned a specific purpose before the month begins. According to Wikipedia, this approach requires justifying every expense anew each period, offering precise control over spending and savings. Here’s how it works:

- Start with zero at the beginning of each budgeting period

- Allocate every dollar of income to specific expense categories

- Justify each expense as if you’re starting from scratch

- Regularly review and adjust allocations based on changing needs

Another popular technique is the Envelope System, a visual and tactile method for managing spending. Wikipedia explains this approach involves allocating cash into physical or virtual envelopes for different expense categories. This method helps prevent overspending by creating clear, tangible limits. Whether you use actual cash envelopes or digital tracking apps, the core principle remains the same: once an envelope is empty, you stop spending in that category. This approach transforms budgeting from an abstract concept into a concrete, manageable process that makes financial discipline feel more achievable and less restrictive.

Here’s a comparison of popular family budgeting methods:

| Method | How It Works | Key Benefit |

|---|---|---|

| Envelope System | Allocate cash to spending categories | Visual control |

| Zero-Based Budgeting | Assign every dollar a job | Precise tracking |

| 50/30/20 Method | 50% needs 30% wants 20% savings/debt |

Simple structure |

| One-Third Rule | Divide income equally: needs savings debt |

Reduces bankruptcy risk |

| 60/30/10 Method | 60% needs 30% wants 10% savings |

Adapts to inflation |

Key Steps to Building Your Budget

Creating a successful family budget requires more than just crunching numbers—it’s about building a financial strategy that works for everyone involved. According to CNB’s personal banking insights, the most effective budgets are collaborative efforts that involve the entire family in financial planning and decision-making.

To get started, follow these critical steps to develop a robust family budget:

-

Calculate Total Household Income

- Combine all sources of regular income

- Include wages, freelance work, investments, and any consistent additional earnings

-

Categorize Your Expenses

- Separate expenses into fixed costs (rent, utilities, insurance)

- Identify variable expenses (groceries, entertainment, dining out)

- Distinguish between needs and wants

-

Set Shared Financial Goals

- Discuss family priorities

- Create short-term and long-term savings objectives

- Ensure everyone understands and agrees on financial targets

Consistent tracking is the final crucial component of successful budgeting. Use digital tools like budgeting apps, detailed spreadsheets, or even traditional pen and paper to monitor your spending. Regular family finance meetings can help everyone stay accountable, adjust strategies as needed, and celebrate financial milestones together. Remember, a budget isn’t about restricting fun—it’s about creating financial freedom and security for your entire family.

Managing Expenses and Maximizing Savings

Effective expense management is more than just cutting costs—it’s about making strategic financial decisions that balance your family’s needs and goals. According to UBS Wealth Management, understanding the difference between needs and wants is crucial for building a sustainable financial plan.

Traditionally, the 50/30/20 budget rule guided households, but recent economic pressures have shifted perspectives. New York Post reports that experts now recommend a 60/30/10 allocation to better reflect current economic challenges:

- 60% for Needs: Housing, utilities, groceries, transportation

- 30% for Wants: Entertainment, dining out, subscriptions

- 10% for Savings: Emergency fund, retirement, investments

Utilize digital budgeting tools like Credit Karma or PocketGuard to track spending, identify unnecessary subscriptions, and highlight potential savings opportunities. These apps can provide real-time insights into your financial habits, helping you make informed decisions. Remember, maximizing savings isn’t about deprivation—it’s about creating financial flexibility that allows your family to pursue both immediate needs and long-term dreams. Small, consistent adjustments can lead to significant financial improvements over time.

Common Budgeting Mistakes to Avoid

Budgeting isn’t just about tracking numbers—it’s about creating a sustainable financial strategy that supports your family’s goals. According to Chase’s financial education resources, many families sabotage their financial success by making common and preventable budgeting errors.

Some of the most critical mistakes to watch out for include:

-

Not Creating a Budget at All Failing to have a budget means flying blind financially

-

Ignoring Small Recurring Expenses Those $5 subscriptions and daily coffee runs add up quickly

-

Basing Budget on Gross Instead of Net Income Always budget using your actual take-home pay, not pre-tax earnings

-

Relying Too Heavily on Credit Cards Credit can create a false sense of financial flexibility

As Step’s financial experts highlight, the most dangerous budgeting pitfall is setting unrealistic expectations that are destined to fail. The key is creating a flexible plan that allows for unexpected expenses while maintaining clear financial boundaries. Build in a ‘wiggle room’ of 5-10% in your budget, track your spending honestly, and be prepared to adjust your strategy as your family’s needs change. Remember, a budget is a living document—not a rigid set of rules that will crush your financial spirit.

Take Your Family Budget Further With ReVroom’s Upfront Savings

Ready to put your new family budgeting strategies into action? If you are looking for a proven way to stretch your hard-earned dollars, start right where big spending happens: your next vehicle. As this guide shows, family budgets thrive on transparency, smart allocation, and protecting every dollar. That is where ReVroom completely reimagines how you buy and sell rebuilt title vehicles. We eliminate sticker shock and unwanted surprises by showing you full vehicle history and photos of every car before repairs. This ensures you always get clarity, not guesswork.

Your budget can go further fast. See for yourself how rebuilt title cars can be up to 50% less expensive than traditional options without sacrificing peace of mind. Take the stress and confusion out of car buying by discovering how ReVroom makes value and transparency standard. Shop smarter today. Your next great deal is waiting.

Frequently Asked Questions

How do I start creating a family budget for 2024?

To create a family budget, begin by calculating your total household income, categorizing expenses into fixed and variable costs, and setting shared financial goals with your family. Regularly track spending and adjust your budget as necessary.

What are the most effective budgeting methods for families?

Some effective budgeting methods for families include the Envelope System, Zero-Based Budgeting, the 50/30/20 method, and the One-Third Rule. These methods help organize finances according to needs, savings, and debt repayment.

What are common mistakes to avoid when budgeting?

Common budgeting mistakes include not creating a budget at all, ignoring small recurring expenses, basing your budget on gross income instead of net income, and relying too heavily on credit cards. It’s essential to set realistic expectations and allow for flexibility in your budget.

How can digital tools help manage my family’s budget?

Digital budgeting tools, such as apps, can assist in tracking spending, identifying unnecessary expenses, and highlighting saving opportunities. They provide real-time insights, making it easier to manage finances and stick to your budget.