Family Budgeting Tips: Complete Guide for 2025

October 20, 2025

Did you know that over 60 percent of families say unexpected expenses disrupt their financial plans? Managing household budgets can feel overwhelming, especially with common myths clouding what really works. The right budgeting strategy not only supports day-to-day spending but also helps you save for major goals like a new car or family vacation. By learning how to separate facts from fiction, you can build practical systems that keep your family’s finances steady in any situation.

Key Takeaways

| Point | Details |

|---|---|

| Importance of Family Budgeting | Family budgeting is a strategic approach that allocates income across essential expenses, savings, and investments to maintain financial stability. |

| Common Budgeting Myths | Common misconceptions include that small expenses don’t matter and that budgeting must be highly restrictive; both can derail financial goals. |

| Budgeting Methods | Families should choose from various budgeting frameworks, such as the 50/30/20 rule or zero-based budgeting, based on their unique financial situations. |

| Avoiding Budgeting Mistakes | Implement consistent tracking, build flexibility for unexpected costs, and regularly reassess your budget to navigate common financial pitfalls effectively. |

Table of Contents

- Defining Family Budgeting And Common Myths

- Types Of Family Budgets And Their Uses

- How To Create A Realistic Budget Plan

- Choosing Tools And Tracking Expenses Efficiently

- Saving On Major Purchases Like Cars

- Common Mistakes And How To Avoid Them

Defining Family Budgeting and Common Myths

Family budgeting is more than just tracking dollars and cents - it’s a strategic approach to understanding and managing your household’s financial ecosystem. At its core, budgeting represents a deliberate plan that allocates income across essential expenses, savings goals, and potential investments. Think of it like a financial roadmap that helps families navigate economic challenges while maintaining financial stability.

According to Tekaloan, one of the most persistent myths is that small daily expenses don’t significantly impact overall finances. However, those seemingly insignificant purchases - like daily coffee runs or impulse snack buys - can actually derail an entire family’s financial strategy. Tracking these small costs provides critical insights into spending patterns and potential areas of improvement.

Another common misconception is that budgeting must be rigidly restrictive. As Sofi research indicates, an unrealistic or overly strict budget is almost guaranteed to fail. The most effective budgeting approaches are those that:

- Align with realistic spending patterns

- Provide flexibility for unexpected expenses

- Create room for occasional treats and personal enjoyment

- Encourage gradual financial discipline

Successful family budgeting isn’t about deprivation - it’s about making intentional choices that support your household’s short and long-term financial wellness. By understanding these myths and adopting a balanced approach, families can transform budgeting from a dreaded chore into an empowering financial tool.

Learn more in our comprehensive guide on budgeting for car maintenance, which can help you plan for one of the most significant recurring expenses in many family budgets.

Types of Family Budgets and Their Uses

Family budgeting isn’t a one-size-fits-all strategy. Different budget frameworks offer unique approaches to managing household finances, allowing families to choose a method that best matches their spending habits, financial goals, and personal preferences. Understanding these variations can help you find the most effective way to track and control your money.

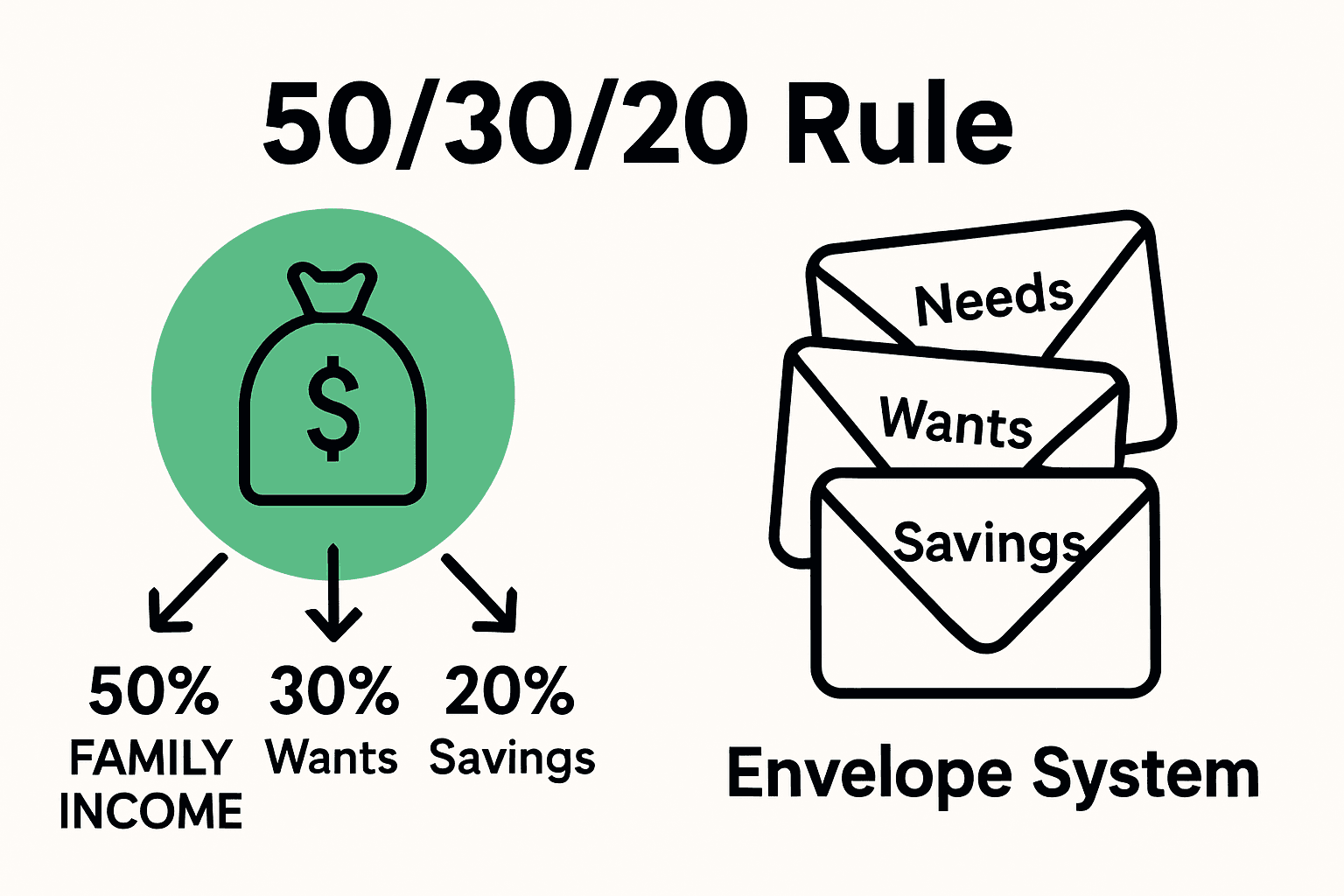

According to NerdWallet, two popular budget allocation methods are the 50/30/20 and 60/30/10 rules. The classic 50/30/20 framework divides income into three key categories: 50% for essential needs like housing and groceries, 30% for discretionary wants, and 20% dedicated to savings and debt repayment. The 60/30/10 alternative offers slightly different proportions, providing families with flexibility to adjust based on their specific financial situations.

Another innovative budgeting approach is the envelope system. As Wikipedia explains, this traditional method involves allocating physical cash into separate envelopes for different expense categories. Modern adaptations have transformed this concept, with families now using multiple checking accounts or sophisticated budgeting software to achieve similar financial tracking and control:

- Zero-based budgeting (every dollar has a purpose)

- Percentage-based budgeting

- Cash envelope method (digital or physical)

- Reverse budgeting (prioritizing savings first)

Choosing the right budget type depends on your family’s unique financial landscape, income stability, and long-term goals.

Explore alternatives to traditional car ownership that can help reduce expenses and provide more financial flexibility for your family’s budget.

Explore alternatives to traditional car ownership that can help reduce expenses and provide more financial flexibility for your family’s budget.

Here’s a comparison of popular family budgeting methods and their main features:

| Budgeting Method | Key Features | Best For |

|---|---|---|

| 50/30/20 Rule | 50% needs 30% wants 20% savings/debt |

Simple allocation Most families |

| 60/30/10 Rule | 60% needs 30% wants 10% savings |

Larger essential expenses |

| Envelope System | Cash or digital envelopes Category limits |

Hands-on tracking Visual control |

| Zero-Based Budgeting | Every dollar assigned No leftover funds |

Detail-oriented planners |

| Percentage-Based | Custom income splits Adjustable categories |

Flexible income situations |

How to Create a Realistic Budget Plan

Creating a realistic budget requires more than just good intentions - it demands a strategic and honest approach to understanding your household’s financial landscape. Financial planning is about crafting a roadmap that reflects your actual income, expenses, and aspirational goals while maintaining flexibility for life’s unexpected twists and turns.

According to PNC, the foundation of an effective budget starts with calculating your accurate net income. This means tallying all sources of household revenue after taxes, then systematically categorizing expenses into fixed costs (like mortgage or car payments) and variable expenses (such as groceries and entertainment). The key is creating a comprehensive view that allows you to compare income against expenditures and make informed adjustments.

To streamline your budgeting process, Dropbox recommends using dedicated worksheets or digital tools to track income and expenses in one centralized location. Your budget strategy should incorporate multiple financial horizons:

- Short-term goals (emergency fund, monthly expenses)

- Medium-term objectives (debt reduction, major purchases)

- Long-term aspirations (retirement savings, investment growth)

Remember that budgeting is an evolving process. Start with realistic, modest savings goals and continuously monitor your spending patterns. When unexpected expenses arise - like car maintenance or repairs - having a flexible budget becomes crucial. Learn smart strategies for saving money on car expenses that can help you maintain financial stability while managing your transportation costs.

Choosing Tools and Tracking Expenses Efficiently

In the digital age, expense tracking has transformed from manual ledger entries to sophisticated technology that simplifies financial management. The right digital tools can turn budgeting from a dreaded chore into an intuitive, almost automatic process that provides real-time insights into your financial health.

According to Wikipedia’s overview of YNAB, modern budgeting apps like You Need a Budget (YNAB) use advanced principles that go beyond simple expense tracking. Their approach emphasizes zero-based budgeting, where every dollar is intentionally assigned a purpose. Key strategies include planning for true expenses, maintaining budget flexibility, and tracking how your money ‘ages’ - essentially measuring your financial progress over time.

Another powerful tool in the expense tracking arsenal is FinanceWorks, which offers comprehensive financial management features. Its platform allows users to:

- Aggregate multiple financial accounts in one place

- Create detailed budgets with precision

- Monitor spending in real-time by category

- Set automatic alerts for potential budget overages

- Track both imported and manually entered transactions

Choosing the right tracking tool depends on your personal financial complexity and comfort with technology. The goal isn’t just recording expenses, but gaining actionable insights that help you make smarter financial decisions. Learn smart strategies for saving money on car expenses that can complement your new expense tracking approach and help you optimize your transportation budget.

Saving on Major Purchases Like Cars

Saving for significant investments like a vehicle requires strategic planning and disciplined financial management. Major purchases don’t just happen overnight - they’re the result of intentional saving, smart budgeting, and clear financial goal-setting that transforms distant dreams into tangible realities.

According to InsureOnTheSpot, successful car savings strategies involve creating a targeted approach. This means setting a precise timeline with realistic weekly or monthly savings targets and opening a dedicated high-yield savings account specifically for your car fund. By applying budgeting frameworks like the 50/30/20 rule, you can strategically redirect discretionary spending toward your automotive goals.

The American Credit Foundation recommends utilizing sinking funds - specialized savings buckets earmarked for specific major purchases. These focused savings strategies help families maintain financial discipline by:

- Keeping car savings separate from emergency funds

- Creating psychological momentum toward the purchase

- Preventing unexpected spending from derailing goals

- Providing clear visibility into savings progress

- Reducing reliance on high-interest financing

To maximize your car savings potential, consider combining multiple strategies like automated transfers, side hustles, and strategic spending cuts. Check out our comprehensive car buying checklist to ensure you’re making the most informed financial decisions throughout your vehicle purchase journey.

Common Mistakes and How to Avoid Them

Budgeting isn’t about perfection - it’s about progress. Financial missteps are common, but understanding and anticipating potential pitfalls can transform your approach from reactive to proactive, helping you build a more resilient financial foundation for your family.

According to Sofi, families frequently fall into predictable budgeting traps that can derail their financial goals. The most prevalent mistakes include failing to track spending consistently, neglecting to plan for occasional or one-time expenses, creating unrealistic budget expectations, and rigidly applying a budgeting method that doesn’t match their unique financial situation.

To navigate these potential challenges, consider these strategic approaches to avoiding common budgeting mistakes:

- Implement consistent, weekly spending tracking

- Build flexible buffer zones in your budget for unexpected expenses

- Regularly reassess and adjust your budgeting strategy

- Create separate savings categories for different financial goals

- Use technology and apps to simplify expense monitoring

Remember that budgeting is an ongoing learning process. Your first attempt won’t be perfect, and that’s okay. Check out our comprehensive car buying checklist to help you make informed financial decisions and avoid potential costly mistakes in major purchases like vehicles.

Stretch Your Family Budget Even Further With ReVroom

You’ve put in the research, tracked your spending, and crafted a family budget that works. But when it comes time for those big-ticket purchases like a car, the biggest hurdle is often feeling locked out by price or worried about getting stuck with hidden surprises. The article above showed how every dollar counts, especially over time. And it made it clear that transparency—knowing exactly what you’re really buying—isn’t just a perk. It is essential for peace of mind and financial stability.

Take your savings game to the next level with rebuilt title vehicles listed on ReVroom. Here, you’ll discover upfront accident history reports, real before-and-after photos, and clear pricing on handpicked vehicles that cost up to 50% less than traditional options. Why pay more for a “clean title” and guess at the history when you can shop with confidence and see the details for yourself? Explore our expert guide to budgeting for car maintenance or kickstart your next purchase with our comprehensive car buying checklist.

Ready to let your dollars go further, just like your next car? Visit ReVroom today to experience a new era of safe, fair, and truly transparent car buying. Your budget, your family, and your journey deserve nothing less.

Frequently Asked Questions

What is family budgeting and why is it important?

Family budgeting is the process of planning and managing household finances to allocate income toward essential expenses, savings goals, and investments. It is important because it helps families maintain financial stability, identify spending patterns, and achieve long-term financial wellness.

What are some common myths about family budgeting?

Common myths about family budgeting include the belief that small daily expenses do not impact overall finances and that budgeting is overly restrictive. In reality, small expenses can add up significantly, and effective budgeting allows for flexibility and enjoyable spending while supporting financial goals.

How do I create a realistic budget plan for my family?

To create a realistic budget plan, start by calculating your accurate net income and categorizing expenses into fixed and variable costs. Use tools or worksheets to track income and expenses, and set achievable short-term and long-term financial goals, allowing for flexibility to accommodate unexpected costs.

What budgeting methods are available for families?

Several budgeting methods cater to different family needs, including the 50/30/20 rule, 60/30/10 rule, envelope system, zero-based budgeting, and percentage-based budgeting. Each method has its unique features and can be tailored to fit your family’s financial circumstances.