How to Boost Credit Score in Utah for Car Buyers 2025

August 4, 2025

Buying a car in Utah in 2025 has a hidden price tag many people miss. Some shoppers end up paying over $7,000 more in interest just because of a low credit score. Most think the sticker price is what matters most when shopping for a vehicle. The real difference between saving thousands and overspending comes down to one number—and it is not the one on the car window.

Table of Contents

- Why Good Credit Matters When Buying A Car

- Simple Habits To Raise Your Credit Score Fast

- Credit Score Tips For Students And Young Buyers

- Avoiding Common Credit Mistakes In Utah

Quick Summary

| Takeaway | Explanation |

|---|---|

| Good credit scores lower car loan rates. | High credit scores lead to lower interest rates, potentially saving thousands over the loan’s duration. |

| Pay bills on time for better scores. | Consistent on-time payments significantly impact your credit score, accounting for about 35% of it. |

| Keep credit utilization below 30%. | Maintain low balances relative to your credit limit to improve your score and borrowing potential. |

| Understand the impact of credit inquiries. | Hard inquiries can reduce your score, so consolidate applications to minimize their effects. |

| Check for and dispute credit report errors. | Regularly review your credit reports and promptly challenge any inaccuracies to protect your score. |

Why Good Credit Matters When Buying a Car

Your credit score is more than just a number in Utah’s car buying landscape. It’s the financial passport that determines how much opportunity and affordability you’ll experience when purchasing a vehicle. A strong credit score doesn’t just open doors - it unlocks substantial financial advantages that can save you thousands of dollars over the lifetime of your car loan.

The Financial Impact of Credit Scores on Car Buying

In Utah’s competitive automotive market, your credit score directly influences your borrowing power and loan terms. Explore car loan strategies that can help you maximize your purchasing potential. According to Experian, credit scores dramatically impact the interest rates you’ll qualify for. Buyers with excellent credit can secure rates as low as 4.5%, while those with lower scores might face rates exceeding 15%.

Let’s break down the real-world implications. On a $25,000 car loan over five years, the difference between a prime and subprime interest rate could mean paying an additional $7,000 to $10,000 in total interest. That’s money directly out of your pocket that could be used for other essential expenses or savings.

Here’s a comparison table to illustrate how your credit score can affect car loan interest rates and the total interest paid on a $25,000 loan over five years in Utah:

| Credit Score Range | Estimated Interest Rate | Total Interest Paid (5 Years) |

|---|---|---|

| 720+ (Excellent) | 4.5% | ~$2,950 |

| 660-719 (Good) | 7.0% | ~$4,700 |

| 600-659 (Fair) | 11.0% | ~$7,700 |

| Below 600 (Poor) | 15.0%+ | $9,800+ |

Building a Strong Credit Profile for Better Car Financing

Credit scores aren’t just about getting approved - they’re about getting the most favorable terms possible. Lenders use credit scores as a risk assessment tool, evaluating your likelihood of repaying the loan. A score above 700 typically signals financial reliability, positioning you for the most attractive financing options.

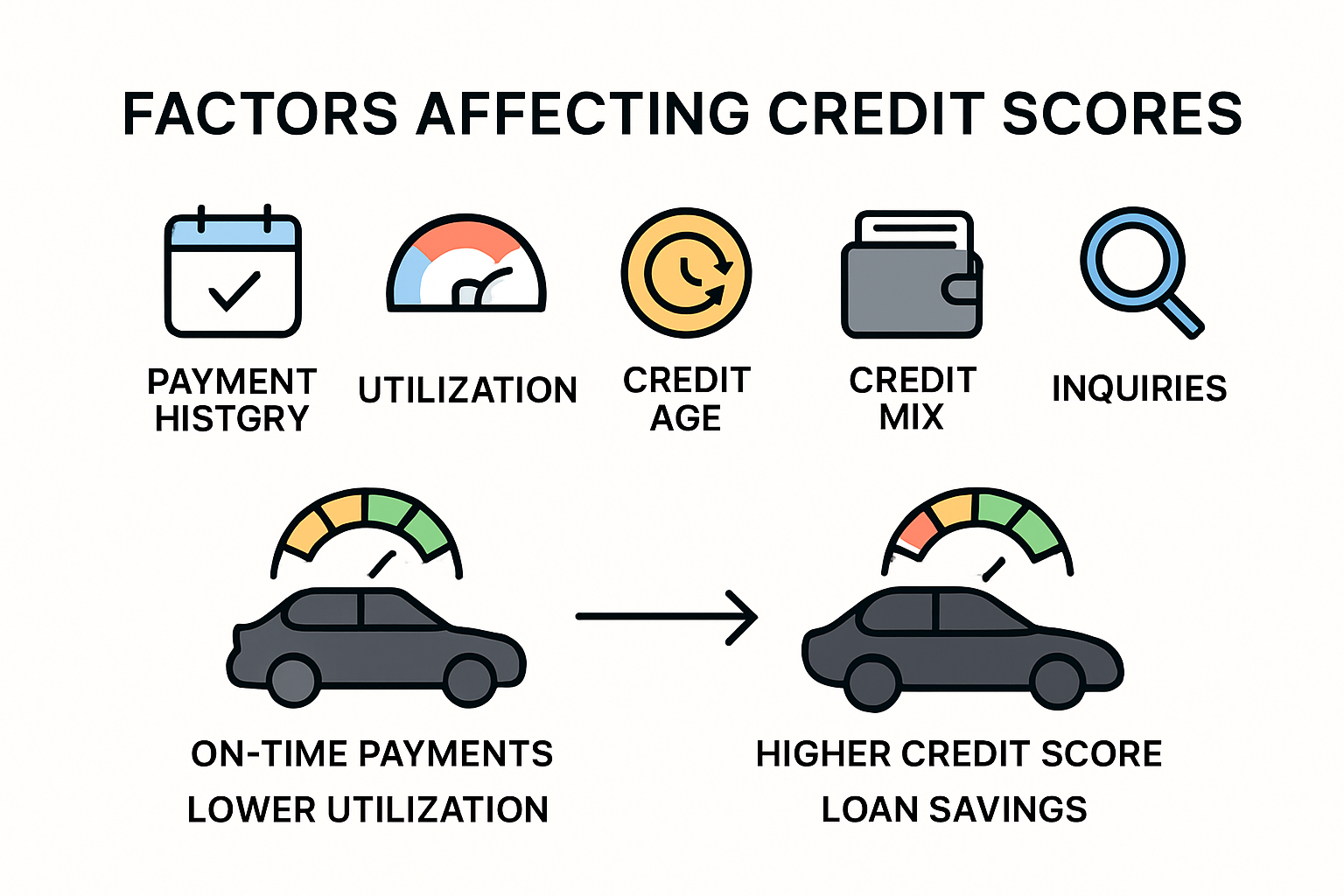

In Utah, where car ownership is often essential, understanding credit dynamics becomes crucial. Key credit factors include:

- Payment History: Consistently paying bills on time

- Credit Utilization: Keeping credit card balances low

- Credit Mix: Having different types of credit accounts

- Length of Credit History: Maintaining long-standing credit relationships

According to FICO, improving your credit score by just 50-100 points can translate into significant savings. For Utah car buyers, this could mean lower down payments, reduced interest rates, and more negotiating power at the dealership.

Understanding your credit score isn’t just about numbers - it’s about financial empowerment. By strategically managing your credit, you transform from a passive borrower to an informed consumer who can confidently navigate Utah’s car buying landscape. Your credit score becomes a powerful tool, opening doors to better vehicles, more favorable financing, and long-term financial flexibility.

Simple Habits to Raise Your Credit Score Fast

Improving your credit score isn’t an overnight miracle - it’s a strategic journey of consistent financial habits. Utah car buyers can implement several practical techniques to accelerate their credit score growth and unlock better financing opportunities.

Strategic Credit Utilization Management

One of the most powerful yet overlooked strategies for boosting credit scores involves credit utilization. Learn more about credit optimization to maximize your financial potential. According to Experian, maintaining a credit utilization rate below 30% can significantly improve your credit score. This means if you have a credit limit of $10,000, try to keep your outstanding balance under $3,000 at any given time.

Credit experts recommend several tactical approaches to manage utilization:

- Pay Multiple Times Monthly: Instead of waiting for the monthly statement, make smaller payments throughout the month

- Request Credit Limit Increases: Higher limits can automatically lower your utilization percentage

- Keep Old Credit Cards Active: Maintaining longer credit histories positively impacts your score

Timely Bill Payments and Credit Repair

Payment history represents the most critical factor in credit scoring. FICO reveals that payment history contributes approximately 35% to your overall credit score. For Utah car buyers, this means developing an ironclad system for consistent, on-time payments.

Effective strategies include:

- Automatic Payment Setup: Configure automatic payments for minimum amounts to prevent missed deadlines

- Payment Reminders: Use smartphone apps or calendar alerts to track bill due dates

- Debt Consolidation: Consider consolidating multiple debts to simplify payment management

Diversifying Credit Mix Strategically

Lenders appreciate borrowers who demonstrate responsible management across different credit types. While this doesn’t mean randomly opening credit accounts, it suggests maintaining a balanced credit portfolio. A mix of revolving credit (like credit cards) and installment loans (such as car loans or mortgages) can positively influence your credit profile.

For Utah residents looking to boost their credit, consider:

- Secured Credit Cards: These provide a low-risk method to build credit with minimal financial exposure

- Credit-Builder Loans: Specialized loans designed to help individuals establish or rebuild credit

- Becoming an Authorized User: Request to be added to a family member’s credit card with a strong payment history

Remember, credit score improvement is a marathon, not a sprint. Consistent, disciplined financial behavior trumps quick fixes. By implementing these strategies, Utah car buyers can systematically enhance their creditworthiness, positioning themselves for better automotive financing options and long-term financial success.

The following table summarizes key habits and strategies mentioned above to help you quickly review actionable steps for boosting your credit score:

| Habit/Strategy | Description / Purpose |

|---|---|

| Pay Multiple Times Monthly | Lowers credit utilization throughout statement cycle |

| Request Credit Limit Increases | Reduces utilization ratio by increasing available credit |

| Keep Old Credit Cards Active | Maintains longer credit history, improving score |

| Set Up Automatic Bill Payments | Prevents missed or late payments |

| Use Payment Reminders | Ensures all bills are paid on time |

| Consider Debt Consolidation | Simplifies payments, can aid on-time payment management |

| Use a Secured Credit Card | Safely builds credit history with low risk |

| Become an Authorized User | Leverages another’s positive payment history on your own profile |

Credit Score Tips for Students and Young Buyers

Navigating the world of credit can feel like a complex maze for students and young buyers in Utah. Building a solid credit foundation early can set the stage for long-term financial success, especially when it comes to major purchases like a car. Discover smart financing options that can help young buyers start their credit journey right.

Understanding Credit as a Financial Tool

For many young Utah residents, credit seems like an abstract concept. According to Experian, establishing credit is crucial for future financial opportunities. A solid credit history isn’t just about buying a car - it impacts everything from rental applications to job prospects.

Students and young buyers should approach credit as a strategic financial tool:

- Start Small: Begin with a secured credit card or student credit card

- Make Modest Purchases: Use credit for small, manageable expenses

- Pay Full Balances: Demonstrate responsible credit management

Building Credit with Limited Income

FICO reveals that young adults face unique challenges in credit building. Limited income and minimal credit history can make traditional credit access challenging. However, several strategies can help overcome these obstacles.

Key approaches for young credit builders include:

- Become an Authorized User: Ask a parent or trusted family member to add you to their credit card

- Student-Specific Credit Cards: Look for cards designed with lower credit requirements

- Credit-Builder Loans: These specialized loans help establish credit history

Avoiding Common Credit Pitfalls

Young buyers often make critical mistakes that can derail their credit journey. TransUnion warns against several common credit traps that can damage long-term financial health.

Critical mistakes to avoid:

- Missed Payments: Even one late payment can significantly impact credit scores

- Maxing Out Credit Limits: High credit utilization damages credit potential

- Applying for Multiple Cards: Too many credit inquiries can lower your score

Building credit is a marathon, not a sprint. For Utah students and young buyers, the key is patience, consistency, and strategic financial management. By understanding credit as a powerful tool rather than a potential trap, young adults can create a strong financial foundation that opens doors to future opportunities - including that dream car purchase.

Remember, every financial decision today shapes your credit landscape tomorrow. Start small, stay disciplined, and watch your credit score grow. Your future self will thank you for the smart choices you make right now.

Avoiding Common Credit Mistakes in Utah

Navigating the complex world of credit requires strategic thinking, especially in Utah’s unique financial landscape. Explore smart financial planning to protect your credit journey and avoid potentially costly missteps that could derail your financial goals.

Misunderstanding Credit Inquiries and Applications

Many Utah residents inadvertently damage their credit by mishandling credit inquiries. According to Experian, not all credit inquiries are created equal. Hard inquiries can lower your credit score by a few points, while soft inquiries have no impact.

Common mistakes to avoid:

- Applying for Multiple Credit Cards Simultaneously: Each application triggers a hard inquiry

- Failing to Understand Inquiry Types: Confusing hard and soft inquiries

- Neglecting to Shop Smart: Not clustering loan applications within a short time frame

Overlooking Credit Report Errors

TransUnion highlights that credit report errors are more common than most Utah residents realize. These mistakes can significantly impact your credit score and financial opportunities.

Strategic error management includes:

- Regular Credit Report Checks: Review reports from all three major credit bureaus annually

- Prompt Error Disputes: Immediately challenge any inaccuracies you discover

- Detailed Documentation: Maintain comprehensive records of your dispute process

Mismanaging Debt and Credit Utilization

FICO reveals that credit utilization plays a crucial role in credit scoring. Utah car buyers often make critical errors in managing their credit limits and debt ratios.

Key strategies to prevent credit utilization mistakes:

- Keep Utilization Below 30%: Maintain low credit card balances relative to your credit limit

- Avoid Closing Old Credit Cards: Longer credit histories positively impact your score

- Strategic Debt Consolidation: Consider consolidating high-interest debts to improve overall credit health

Utah’s financial landscape demands a proactive approach to credit management. Each decision can have lasting consequences on your ability to secure favorable car loans, rental agreements, and other financial opportunities. By understanding these common pitfalls, you can develop a more strategic approach to building and maintaining a robust credit profile.

Remember, credit is not about perfection but consistent, responsible financial behavior. Small, intentional steps can transform your credit journey, opening doors to better financial futures. Stay informed, stay disciplined, and watch your credit potential grow.

Frequently Asked Questions

How does my credit score affect car financing in Utah?

Your credit score directly influences the interest rates you’ll qualify for when financing a car in Utah. Higher scores can secure lower rates, potentially saving thousands over the lifespan of the loan.

What strategies can I use to quickly boost my credit score?

To rapidly improve your credit score, focus on timely bill payments, maintaining a credit utilization rate below 30%, and diversifying your credit mix. Setting up automatic payments and paying down debts can also be effective.

What common mistakes should I avoid when managing my credit?

Common mistakes include missing payments, maxing out credit limits, frequently applying for new credit without understanding the effect of inquiries, and overlooking errors in your credit report that can negatively impact your score.

How can young buyers establish credit when purchasing a car?

Young buyers can start building credit by using secured credit cards, becoming authorized users on family members’ accounts, and applying for student-specific credit cards. Making timely payments on small purchases can also help establish a positive credit history.

Give Your Credit Score a Winning Edge With a Rebuilt Ride

You already know that a better credit score saves you thousands on car loans. But saving money does not have to end there. While you sharpen your credit toolkit and build a strong score, you also want every dollar to work harder when it is finally time to buy. That is where ReVroom comes in. We are the only online marketplace dedicated to rebuilt title vehicles—offering upfront accident history and before-repair photos, so you can spot value without spending extra on third-party reports. Lower sticker prices paired with deeper transparency mean you stretch your credit and cash further, with all the key info in one place.

Smart car buyers use the right credit habits and the right marketplace. Are you ready to accelerate both your budget and your vehicle options in Utah? Come visit ReVroom and browse vehicles built for a second chance. Your journey to owning a reliable ride for less starts now. You have put in the work to boost your credit—now let your money and your next car do the same. View available vehicles and see just how far you can go.