Rebuilt title auto loans Utah: a budget buyer's guide

May 18, 2026

TL;DR:

- Rebuilt title vehicles in Utah can be purchased at up to 50% lower prices with financing options similar to clean titles.

- Securing a loan requires proper documentation, inspections, and verifying Utah’s legal and safety compliance steps.

- Well-prepared buyers can confidently finance and register rebuilt title cars, benefiting from transparency, affordability, and environmentally friendly choices.

If you’re shopping for a vehicle in Utah on a tight budget, rebuilt title auto loans in Utah might be the most underrated move you can make. Rebuilt title vehicles, meaning cars that were previously declared a total loss by an insurer and have since been professionally repaired and restored to a drivable condition, can cost up to 50% less than comparable clean title vehicles. The catch? Most buyers don’t know how financing actually works for these cars, or what Utah requires before you can legally drive one home. This guide covers all of it, from securing a loan to completing registration, so you can buy with confidence.

Table of Contents

- What you need to know about rebuilt title auto loans in Utah

- Step-by-step guide to securing rebuilt title auto loans in Utah

- Troubleshooting financing hurdles and verifying rebuilt title vehicles in Utah

- Completing registration and ownership for rebuilt title vehicles in Utah

- Why rebuilt title auto loans can be a savvy choice for Utah budget buyers

- Discover your rebuilt title vehicle with ReVroom today

- Frequently asked questions

What you need to know about rebuilt title auto loans in Utah

Let’s clear up the most important distinction first. A rebuilt title is not the same as a title that hasn’t been restored. A vehicle earns a rebuilt title after it has been fully repaired, passed required state inspections, and been deemed roadworthy again. It is a vehicle with a documented history, not a question mark on four wheels.

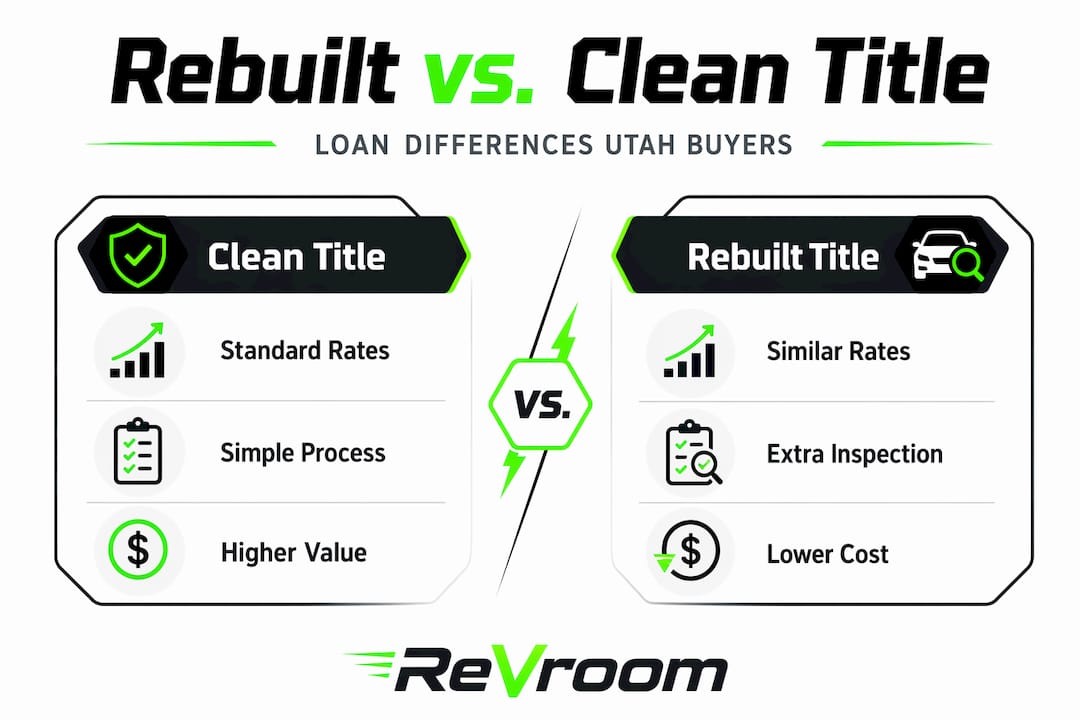

Here’s what that means for Utah auto financing: the process is more accessible than most buyers expect. Financing branded title vehicles in Utah is often comparable to clean title financing, with similar interest rates and loan terms that can stretch up to 72 months. That surprises a lot of people. The assumption that you’ll pay a penalty rate for choosing a rebuilt title car simply doesn’t hold up in practice.

Key facts about rebuilt title vehicles in Utah:

- Rebuilt titles are issued after a vehicle has been repaired and passed a state-required inspection

- They are legally distinct from other title designations and carry full registration eligibility in Utah

- Prices are typically 20% to 50% lower than equivalent clean title vehicles

- Lenders, including credit unions and dealerships, regularly offer used car loans Utah buyers can use for rebuilt title purchases

- Insurance for rebuilt title cars is widely available, contrary to popular myth

What lenders typically look at when you apply:

- Your credit score and credit history

- Proof of income and employment stability

- The vehicle’s appraised value relative to the loan amount

- Inspection certificates confirming the car meets Utah safety standards

- Valid rebuilt title paperwork for the specific vehicle

Understanding Utah rebuilt title legal requirements before you apply saves time and prevents surprises. Utah requires a VIN (vehicle identification number) inspection via Form TC-661 when titling a rebuilt vehicle for the first time, plus safety and emissions inspections where applicable. These aren’t bureaucratic hurdles thrown up to slow you down. They’re the paper trail that gives lenders and buyers alike the confidence to move forward.

Pro Tip: Before you approach any lender, pull together your inspection certificates and rebuilt title paperwork. Lenders who finance rebuilt title vehicles want to see that the car has cleared Utah’s requirements. Showing up prepared puts you in a stronger negotiating position.

| Loan feature | Clean title vehicle | Rebuilt title vehicle |

|---|---|---|

| Typical interest rates | Standard market rates | Often comparable to clean title |

| Loan terms available | Up to 72 months | Up to 72 months |

| Lender availability | Broad | Credit unions, select dealerships |

| Documentation required | Standard | Standard plus inspection certificates |

| Average vehicle cost | Full market value | Up to 50% below market |

For more detail on lenders open to this type of deal, check out our guide on financing rebuilt titles in Utah.

Step-by-step guide to securing rebuilt title auto loans in Utah

Knowing the landscape is one thing. Actually getting funded is another. Here’s a practical walkthrough of how to finance a rebuilt title vehicle in Utah without spinning your wheels.

-

Gather your documents early. You’ll need a government-issued ID, proof of income (pay stubs or tax returns work well), the vehicle’s rebuilt title, inspection certificates, and any repair documentation the seller can provide. The more complete your file, the faster lenders can process your application.

-

Check your credit score before applying. Even if you’re looking at bad credit auto loans Utah lenders offer, knowing your number helps you target the right institutions. Credit unions often have more flexibility than traditional banks for non-standard vehicle titles.

-

Get a pre-approval if possible. A pre-approval letter tells you exactly what you can spend and signals to sellers that you’re serious. It also gives you a baseline rate to negotiate against.

-

Shop multiple lenders. Don’t accept the first offer. Credit unions, community banks, and dealerships that specialize in Utah auto financing for rebuilt vehicles may each quote you different terms. A half-point difference in interest rate over 60 months adds up to real money.

-

Confirm the lender accepts rebuilt titles. This sounds obvious, but not every lender does. Ask directly before submitting a full application. Lenders in Utah, including credit unions and dealerships, often finance rebuilt title vehicles without significantly higher rates, but you want confirmation upfront.

-

Review loan terms against the vehicle’s value. Because rebuilt title cars are priced lower, you want to make sure your loan amount reflects that reality. Overborrowing against a rebuilt title vehicle is a mistake you want to avoid.

-

Finalize and sign. Once terms are agreed upon, you’ll sign your loan agreement and receive your funds or payment arrangement. Keep copies of everything.

Pro Tip: When comparing loan offers, calculate the total cost of the loan, not just the monthly payment. A longer term with a slightly lower rate can still cost you more overall. Run the full numbers before you sign anything.

For a deeper look at lender options specific to this type of purchase, our resource on rebuilt title loan options Utah breaks down who’s lending and what they’re looking for.

Troubleshooting financing hurdles and verifying rebuilt title vehicles in Utah

Even well-prepared buyers run into snags. Here’s how to handle the most common ones.

Common financing obstacles and how to address them:

- Lender says no to rebuilt titles. Move on quickly. This is a lender policy issue, not a reflection of your credit or the car’s quality. Focus on lenders who actively work with rebuilt title vehicles.

- Credit challenges slowing approval. A larger down payment reduces lender risk and can offset a lower credit score. Even 10% to 15% down can shift an answer from “maybe” to “yes.”

- Loan amount doesn’t align with vehicle price. Some lenders cap loan amounts on branded title vehicles. If that’s the case, a different lender or a slightly higher down payment typically resolves it.

Verifying the vehicle before you commit:

This part matters as much as the loan itself. To ensure safety, verify inspection certificates confirming the vehicle passed Utah’s safety and emissions tests, and make sure VIN inspections are consistent with the car you’re actually buying. A mismatch anywhere in the paperwork is a serious flag.

“The rebuilt title process exists precisely because Utah wants these vehicles verified before they hit the road. That paper trail is your best friend as a buyer.”

Always schedule an independent in-person inspection before finalizing any purchase. No online report, however thorough, replaces eyes and hands on the actual vehicle. This is true for any used car, rebuilt title or otherwise.

| Verification step | What to look for | Red flag |

|---|---|---|

| VIN inspection (Form TC-661) | VIN matches title documents | VIN doesn’t match paperwork |

| Safety inspection certificate | Current, issued by Utah-certified shop | Expired or missing certificate |

| Emissions test certificate | Passed within required timeframe | Failed test or no documentation |

| Vehicle history report | Consistent with seller’s description | Major gaps or inconsistencies |

| In-person inspection | Repairs appear thorough and professional | Visible shortcuts or mismatched panels |

For guidance on what to look for when evaluating specific listings, our article on finding reliable rebuilt cars Utah goes deeper on the vetting process. And when you’re ready to tackle the paperwork side, our rebuilt title car registration Utah guide walks you through every form.

Completing registration and ownership for rebuilt title vehicles in Utah

You’ve got your loan. You’ve verified the car. Now let’s get it legally registered in your name.

Documents required to register a rebuilt title vehicle in Utah:

- Completed Form TC-656 (Title and Registration Application)

- VIN inspection completed via Form TC-661

- Valid safety inspection certificate

- Emissions test certificate (required in most Utah counties)

- Proof of insurance

- Government-issued ID

- Proof of purchase or bill of sale

Step-by-step Utah DMV registration process:

- Complete your VIN inspection at an authorized Utah inspection station using Form TC-661.

- Pass the safety inspection at a state-certified facility and obtain your certificate.

- Complete your emissions test if you’re in a county where it’s required (most Wasatch Front counties).

- Fill out Form TC-656 with the vehicle details, your personal information, and the rebuilt title information.

- Bring all documents and your Utah DMV requirements to your local DMV office or submit where online options apply.

- Pay registration fees and receive your plates and registration.

| Requirement | Rebuilt title vehicle | Clean title vehicle |

|---|---|---|

| Form TC-656 | Required | Required |

| VIN inspection (Form TC-661) | Required on first title transfer | Not typically required |

| Safety inspection | Required | Required |

| Emissions test | Required (most counties) | Required (most counties) |

| Proof of repairs/inspection certificates | Required | Not required |

The extra step for rebuilt titles is the VIN inspection. It takes maybe 30 minutes and costs a small fee. That’s it. Once you clear that, the rest of the process mirrors registering a car in Utah with a clean title almost exactly.

Why rebuilt title auto loans can be a savvy choice for Utah budget buyers

Here’s an honest take that runs counter to what most people assume: rebuilt title vehicles are not the risky gamble the internet makes them out to be. They are, in many cases, the most transparent vehicles on the market. Think about that for a second. A clean title car can have a rich history of fender benders, flood exposure, or deferred maintenance and legally wear a spotless title. A rebuilt title car, by contrast, has been formally inspected, documented, and verified by the state of Utah before you ever see it.

The fear around rebuilt titles is largely inherited, passed down from a time before modern inspection requirements and vehicle history transparency. Buyers who do their due diligence, which means reading the inspection paperwork, verifying the VIN, and having the car looked at independently, consistently report that they got significantly more vehicle for their money than they could have otherwise afforded.

There’s also a sustainability angle worth acknowledging. Choosing a professionally restored vehicle over buying new keeps a car on the road instead of in a lot. That’s good for your wallet and a quiet win for the environment.

The financing piece is where the real surprise lives. Cheap auto loans Utah buyers associate with questionable dealerships are not your only path. Credit unions and reputable lenders regularly offer competitive Utah auto financing for rebuilt title vehicles, sometimes at rates that match clean title loan terms. The key is preparation, documentation, and knowing where to look.

The buyers who lose in this market are the ones who skip verification steps or accept incomplete paperwork because the price looks good. The ones who win are the ones who treat due diligence as non-negotiable. For those buyers, smart savings on rebuilt title cars in Utah are not luck. They’re the logical result of buying with information instead of assumption.

Discover your rebuilt title vehicle with ReVroom today

Finding a rebuilt title vehicle you can trust starts with having the right information in front of you before you make any decisions.

ReVroom is the only online marketplace built specifically for rebuilt title vehicles. Every listing includes vehicle history information and photos of what the car looked like before it was repaired, so you can evaluate the full picture without paying for separate reports or chasing down documentation on your own. That’s real transparency, built into every search. Whether you’re exploring Utah auto financing options or just starting to browse, the ReVroom rebuilt auto marketplace puts the best rebuilt title vehicles in Utah right in front of budget-conscious buyers who deserve honest answers and a fair shot at a great deal.

Frequently asked questions

Can I get a car loan for a rebuilt title vehicle in Utah?

Yes, many lenders in Utah offer financing for rebuilt title vehicles with terms and rates similar to clean title cars, especially when supported by proper inspections and documentation. Financing branded title vehicles in Utah often mirrors clean title financing, with terms available up to 72 months.

What inspections are required to register a rebuilt title car in Utah?

You must complete a VIN inspection using Form TC-661 when titling in Utah for the first time, plus a safety inspection and emissions test where required. Utah DMV requirements for rebuilt title vehicles are clearly defined and manageable with the right preparation.

Are interest rates higher for rebuilt title auto loans in Utah?

No, interest rates for rebuilt title vehicle loans are usually similar to those for cars with clean titles. Financing a branded title car is not that different from clean title financing, with comparable rates and terms up to 72 months.

What should I check to verify a rebuilt title vehicle’s safety in Utah?

Ask for inspection certificates confirming the vehicle passed Utah’s safety and emissions tests, and verify that VIN inspection documents match the actual vehicle to protect your purchase. An independent in-person inspection before buying adds an extra layer of confidence.