What Insurance Covers Rebuilt Titles: Complete Guide

November 4, 2025

Did you know that over half a million vehicles in the United States carry rebuilt titles each year? Many buyers are drawn to these cars for their lower upfront prices, but insuring them can bring unexpected challenges. Understanding what a rebuilt title means and how it affects your insurance options can help you avoid costly surprises and make smarter decisions when shopping for your next ride.

Table of Contents

- Defining Rebuilt Titles And Coverage Basics

- Types Of Insurance Available For Rebuilt Titles

- Factors Influencing Premiums And Coverage Eligibility

- Coverage Limits, Exclusions, And Claim Payouts

- Tips For Insuring A Rebuilt Title Vehicle

Key Takeaways

| Point | Details |

|---|---|

| Rebuilt Title Definition | A rebuilt title indicates a vehicle previously classified as salvage has been restored and meets safety standards after passing inspections. |

| Insurance Complexity | Insuring rebuilt title vehicles is often more challenging with limited coverage options; consult with insurers to understand available policies. |

| Impact on Premiums | Insurance premiums for rebuilt vehicles can be higher due to previous damage; quality of repairs and documentation significantly influence insurability. |

| Preparation for Insurance | Obtain a professional inspection and maintain detailed repair records to improve coverage chances; transparency with insurers is essential. |

Defining Rebuilt Titles And Coverage Basics

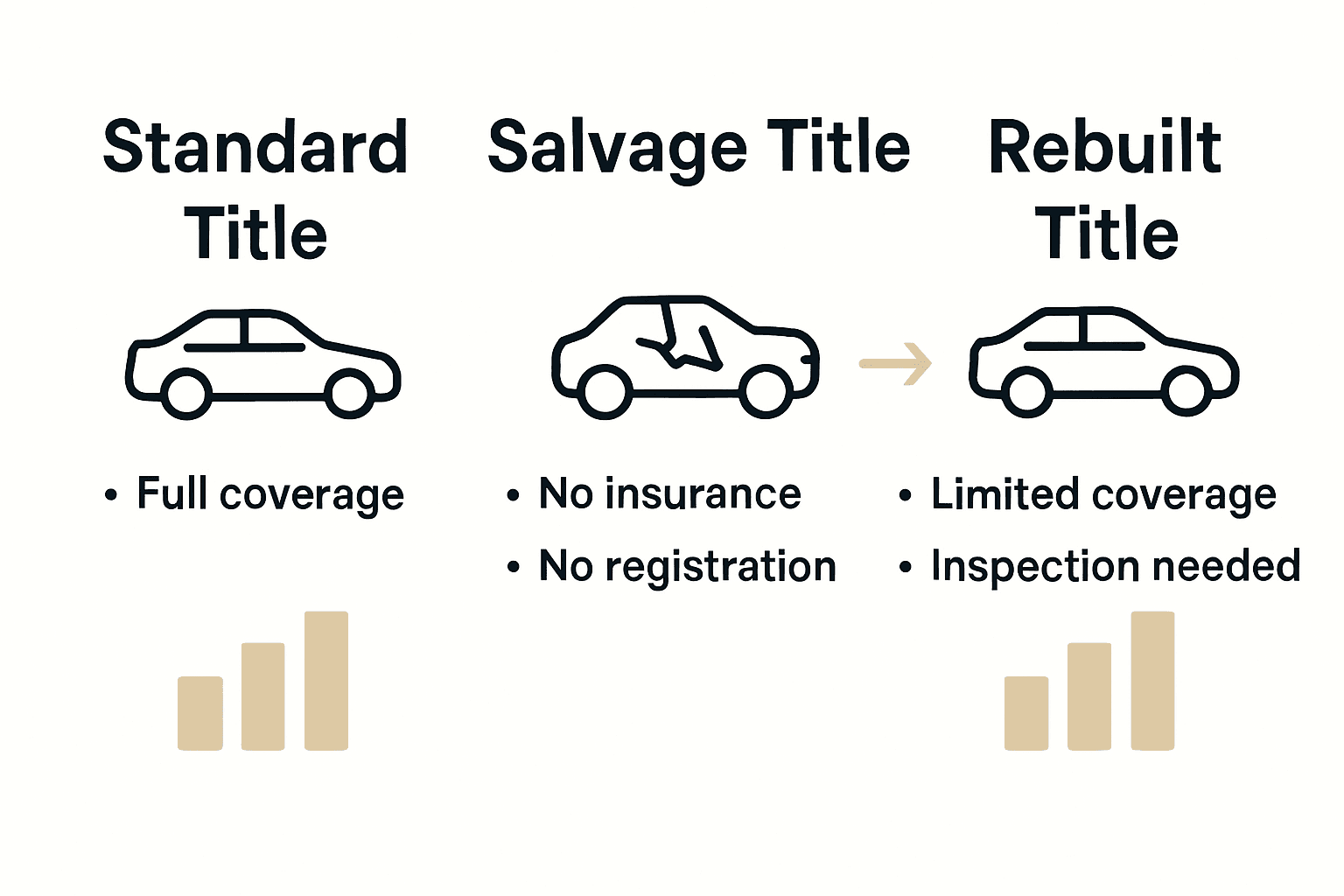

A rebuilt title represents a vehicle that was previously designated as a total loss or salvage but has since been repaired and restored to roadworthy condition. According to txdmv, a rebuilt vehicle is one that was previously branded as ‘salvage’ but has been restored to meet safety standards and passed necessary inspections.

The journey from salvage to rebuilt involves several critical steps. When an insurance company declares a vehicle a total loss due to extensive damage, it receives a salvage certificate. dmv.org explains that this certificate indicates the vehicle cannot be sold, driven, or registered in its current condition. However, after comprehensive repairs and a successful safety inspection, the owner can apply for a new title marked as ‘Rebuilt’ or ‘Revived Salvage.’

Rebuild standards vary by state, but generally involve rigorous checks to ensure vehicle safety. Key components of the rebuilding process typically include:

- Complete structural repair

- Replacement of damaged mechanical systems

- Passing comprehensive safety inspections

- Obtaining official state certification

While rebuilt titles might seem intimidating, they represent an opportunity for budget-conscious buyers to access vehicles at significantly reduced prices. These cars have been carefully restored and, when properly inspected, can offer reliable transportation.

Understanding the nuances of rebuilt titles is crucial. They differ from standard used cars in their history and potential insurance considerations.

Always conduct thorough research, get professional inspections, and understand the vehicle’s complete background before making a purchase decision.

Always conduct thorough research, get professional inspections, and understand the vehicle’s complete background before making a purchase decision.

Types Of Insurance Available For Rebuilt Titles

Insuring a rebuilt title vehicle can be more complex compared to standard used cars. dmv.org highlights that insurance options for rebuilt vehicles are typically more limited, with many insurers offering only basic coverage. Most insurance providers will typically provide liability insurance, which covers damages you might cause to other vehicles or property in an accident.

Before purchasing a rebuilt title vehicle, txdmv recommends checking with your insurance agent to confirm potential coverage. Some insurance companies may be hesitant to offer comprehensive or collision coverage due to the vehicle’s previous damage history.

Typical insurance options for rebuilt title vehicles include:

Here’s a summary of insurance coverage and requirements for rebuilt title vehicles:

| Coverage Type | Availability | Typical Requirements |

|---|---|---|

| Liability | Widely available | Proof of repairs Inspection report |

| Uninsured/Underinsured Motorist | Limited | May require detailed history Inspection |

| Personal Injury Protection | Sometimes offered | State-specific Medical records |

| Comprehensive | Rare/Limited | Full documentation Professional appraisal |

| Collision | Rare/Limited | Detailed restoration records Photos |

- Liability Coverage: Mandatory in most states

- Uninsured/Underinsured Motorist Protection: Additional safety net

- Personal Injury Protection: Covers medical expenses

- Basic Comprehensive Coverage: Limited availability

While insurance might seem challenging, understanding your options for insuring rebuilt title cars can help you navigate the process effectively. Many insurers will require a professional inspection and detailed repair documentation before providing coverage.

The key is preparation. Gather all repair records, obtain a professional vehicle inspection, and shop around with multiple insurance providers. Some specialized insurers are more open to covering rebuilt title vehicles, so don’t get discouraged if your first few inquiries are unsuccessful.

Factors Influencing Premiums And Coverage Eligibility

Insurance premiums for rebuilt title vehicles are uniquely complex. dmv.org emphasizes that the extent of previous damage and the quality of repairs significantly influence an insurer’s willingness to provide coverage. Insurers conduct meticulous assessments, examining detailed documentation and potentially requiring professional inspections to evaluate the vehicle’s current condition and potential risk.

According to txdmv, several critical factors determine a rebuilt title vehicle’s insurability and premium rates. These include:

- Repair Quality: Thoroughness and professional standard of previous repairs

- Vehicle Age: Newer vehicles might receive more favorable consideration

- Damage Extent: Original reason for total loss declaration

- Inspection Reports: Professional assessments of current vehicle condition

- Repair Documentation: Comprehensive records of all restoration work

Most insurance providers will evaluate rebuilt title vehicles through a rigorous risk assessment process. They’ll typically request:

- Complete repair records

- Professional mechanical inspection reports

- Photographic evidence of restoration

- Vehicle identification number (VIN) history

Understanding insurance options for rebuilt vehicles requires patience and thorough preparation. While premiums might be higher, many insurers are becoming more open to providing coverage for well-documented, professionally restored vehicles.

Ultimately, transparency is key. The more comprehensive documentation you can provide about the vehicle’s restoration, the better your chances of securing favorable insurance coverage. Work closely with insurance agents who specialize in or have experience with rebuilt title vehicles to navigate this unique insurance landscape.

Coverage Limits, Exclusions, And Claim Payouts

Insurance coverage for rebuilt title vehicles presents unique challenges. dmv.org reveals that policies for these vehicles typically come with higher premiums, more restrictive coverage limits, and specific exclusions that differ significantly from standard vehicle insurance.

According to txdmv, rebuilt vehicles are inherently valued lower than similar clean title vehicles, which directly impacts potential claim payouts. This diminished value means insurance companies often provide reduced compensation in the event of an accident or total loss.

Typical coverage limitations for rebuilt title vehicles include:

- Reduced Comprehensive Coverage: Limited protection against non-collision damages

- Lower Collision Coverage: Decreased payout for vehicle damage

- Minimal Replacement Value: Significantly reduced total loss settlements

- Specific Repair Exclusions: Potential restrictions on certain types of repairs

Key considerations for claim payouts involve:

- Documenting pre-existing repair work

- Understanding precise policy limitations

- Getting professional vehicle appraisals

- Maintaining comprehensive repair records

Understanding insurance claim processes requires careful preparation and realistic expectations. While coverage might seem challenging, many insurers are developing more nuanced approaches to rebuilt title vehicles.

Ultimately, transparency and thorough documentation are your best allies. Work closely with insurance providers who specialize in rebuilt title vehicles, carefully review policy details, and be prepared to negotiate based on your vehicle’s documented restoration quality and condition.

Tips For Insuring A Rebuilt Title Vehicle

Vehicle insurance for rebuilt titles demands strategic preparation. dmv.org recommends obtaining a thorough inspection from a qualified mechanic and maintaining detailed repair records to improve your chances of securing comprehensive coverage. These proactive steps can significantly enhance an insurer’s confidence in your vehicle’s condition.

According to txdmv, verifying the extent of previous damage and ensuring proper repairs are critical before attempting to insure a rebuilt vehicle. Insurance agents will typically require extensive documentation to assess the vehicle’s current roadworthiness.

Key strategies for successfully insuring a rebuilt title vehicle include:

- Professional Inspection: Get a comprehensive mechanical evaluation

- Detailed Repair Documentation: Collect all repair records and receipts

- Multiple Insurance Quotes: Shop around with different providers

- Transparency: Disclose complete vehicle history upfront

- Specialized Insurers: Seek out companies experienced with rebuilt titles

Practical steps to prepare for insurance application:

- Gather all original repair documentation

- Obtain a professional pre-insurance vehicle inspection

- Compile comprehensive photographic evidence of repairs

- Research insurers specializing in rebuilt title vehicles

Understanding insurance options for rebuilt cars requires patience and thorough preparation. Some insurers are more open to rebuilt titles than others, so don’t get discouraged by initial rejections.

Ultimately, your goal is to demonstrate the vehicle’s safety and reliability. Be prepared to invest time in documentation, be transparent about the vehicle’s history, and approach the insurance process as a collaborative effort to protect both you and the insurance provider.

Navigate Rebuilt Title Insurance with Confidence and Transparency

Understanding what insurance covers rebuilt titles reveals the challenges of hidden histories and limited coverage options. You want a vehicle that fits your budget but also a partner in your journey who respects the importance of transparency and thorough documentation. This article shows that securing insurance for rebuilt title vehicles requires patience, detailed repair records, and smart shopping — a process that can feel overwhelming without the right support.

That is exactly where ReVroom steps in. We are the only online marketplace built specifically for rebuilt title cars. With us, the guesswork fades because every listing includes accident history information and photos of each vehicle before repair. This upfront transparency lets you make informed decisions quickly with less time and money spent. Our mission is clear: to help you find reliable vehicles priced up to 50 percent less than their clean title counterparts while avoiding surprises and frustration.

Ready to take control and shop smarter for your rebuilt vehicle insurance needs?

Discover the difference at ReVroom. Start exploring listings with full history and photo proof now and see why buyers trust us to make rebuilt title cars safe, fair, and straightforward. Don’t wait — your next vehicle and smarter insurance experience await at ReVroom. Go further with confidence and clarity today.

Frequently Asked Questions

What is a rebuilt title?

A rebuilt title indicates a vehicle that was previously declared a total loss or salvage but has been repaired and restored to meet safety standards and passed necessary inspections.

What types of insurance are available for rebuilt title vehicles?

Insurance options for rebuilt title vehicles typically include liability coverage, uninsured/underinsured motorist protection, personal injury protection, and in some cases, limited comprehensive and collision coverage.

How do insurance premiums differ for rebuilt title vehicles compared to standard vehicles?

Insurance premiums for rebuilt title vehicles are generally higher due to their prior damage history, repair quality, and the increased risk associated with insuring them.

What documentation do I need to provide to insure a rebuilt title vehicle?

To insure a rebuilt title vehicle, you typically need to provide complete repair records, professional inspection reports, photographic evidence of restoration, and the vehicle identification number (VIN) history.