Kelley Blue Book Rebuilt Title: What Buyers Must Know

June 6, 2026

TL;DR:

- A Kelley Blue Book rebuilt title indicates a vehicle once declared a total loss, now professionally repaired and legally roadworthy, but permanently branded — which typically means it sells for 20% to 40% less than an identical clean title car. KBB doesn’t auto-adjust its values for rebuilt titles, so buyers apply the discount themselves based on the vehicle’s history, repair quality, and state inspection standards. Understanding those factors is how you find a fair price and a genuinely good deal.

A Kelley Blue Book rebuilt title designation identifies a vehicle that was once declared a total loss, professionally repaired, and legally cleared for road use again. The catch? That title brand is permanent, and it typically means the car sells for 20% to 40% less than an identical clean title vehicle. If you’re shopping with KBB data in hand, you need to know exactly what those numbers mean — and what they don’t. Because KBB gives you a starting point, not a final answer.

How Kelley Blue Book calculates rebuilt title vehicle values

Here’s the thing most buyers don’t realize: Kelley Blue Book does not automatically adjust its pricing for rebuilt titles. When you pull up a vehicle on KBB, you get a clean title baseline. The KBB valuation tool does not incorporate vehicle history details like branded titles into its standard output. That means the number you see is the starting point for your math, not the final price.

What does that mean in practice? You apply the adjustment yourself. The standard approach is a 20% to 40% deduction from the KBB clean title value, depending on the vehicle’s specific history, repair quality, and local market conditions. On a vehicle KBB values at $20,000 with a clean title, a rebuilt version realistically sells between $12,000 and $16,000. That’s a meaningful spread, and it’s why the details behind each vehicle matter so much.

KBB recommends case-by-case appraisal for branded vehicles rather than a blanket formula. The right discount depends on factors like what type of event triggered the total loss designation, how thoroughly the repairs were documented, and what buyers in your market are willing to pay. Treating every rebuilt title as a flat 30% off is too blunt an instrument.

A few things to keep in mind when using KBB for rebuilt title research:

- KBB’s “Fair Market Range” reflects clean title transactions only

- The “Instant Cash Offer” tool will not apply to most rebuilt title vehicles

- Private party values from KBB serve as the most useful baseline for rebuilt title comparisons

- Supplemental tools like vehicle history reports and in-person inspections are necessary to complete the picture

Pro Tip: When using KBB as a rebuilt title reference, pull the private party value for the vehicle in “Good” condition, then apply your 20-40% adjustment based on the specific vehicle history. That gives you a realistic negotiating range.

What factors drive the value reduction on a rebuilt title car

Not every rebuilt title vehicle carries the same discount. The spread between a 20% and a 40% reduction is real, and it comes down to a handful of specific variables. Understanding them helps you figure out where a particular car lands on that spectrum — and where the best deals hide.

-

Type of original event. Vehicles with cosmetic or minor histories, like hail or paint issues, tend to retain 65% to 80% of their clean title value after rebuild. Vehicles with structural or flood histories typically sell for 30% to 60% of clean value. The nature of the vehicle’s history is the single biggest driver of discount depth.

-

Quality and documentation of repairs. Professional repairs backed by photos, receipts, and inspection records push values toward the higher end of the range. Undocumented repairs with no paper trail do the opposite. Buyers and insurers both reward transparency.

-

State inspection standards. The state where a vehicle received its rebuilt title matters more than most buyers expect. Strict states like California, New York, Texas, and Ohio require frame measurements and photo documentation before issuing a rebuilt title. A rebuilt title from a strict state carries extra credibility in the resale market.

-

Market conditions and buyer perception. Local supply and demand affect rebuilt title pricing just like any used car. In markets with high clean title prices, rebuilt title vehicles attract more buyers and hold value better. In slower markets, the discount can widen — which can mean an even better deal for you.

-

Insurance availability. Coverage options affect how much buyers are willing to pay. When a vehicle is easy to insure fully, buyers feel more confident and will pay closer to the top of the range.

| Factor | Effect on value |

|---|---|

| Cosmetic or minor vehicle history | Retains 65-80% of clean title value |

| Structural or flood history | Retains 30-60% of clean title value |

| Strict state inspection (CA, NY, TX, OH) | Higher buyer confidence, smaller discount |

| Lenient state inspection | Lower buyer confidence, larger discount |

| Full repair documentation | Pushes value toward the high end of range |

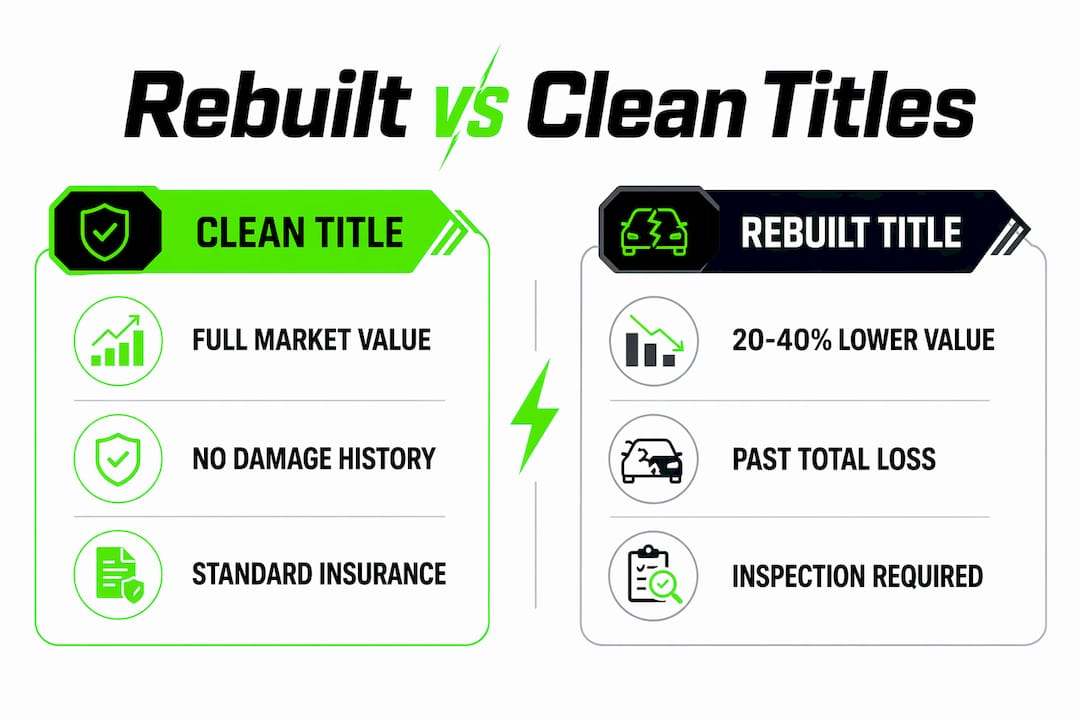

Rebuilt vs. clean title: a side-by-side value comparison

Clean title values from KBB represent the market baseline. A clean title means the vehicle has never been declared a total loss, and it carries no permanent branding. That’s the number you see when you search KBB without any adjustments — and the number you use as your anchor when evaluating a rebuilt title vehicle.

Rebuilt titles occupy a distinct middle ground. They are legally roadworthy after passing state inspection, but the title brand stays with the vehicle. That permanence is what creates the discount — and the opportunity for a buyer who knows how to read it.

Here’s how the math looks across a few real-world scenarios:

| Vehicle (clean title KBB value) | Rebuilt title range | Estimated rebuilt price |

|---|---|---|

| $20,000 sedan | 20-40% reduction | $12,000 to $16,000 |

| $35,000 SUV | 20-40% reduction | $21,000 to $28,000 |

| $50,000 truck | 20-40% reduction | $30,000 to $40,000 |

The opportunity here is real. A $35,000 SUV available for $21,000 to $28,000 is a significant saving, especially when the vehicle’s history involves something minor like hail or a theft recovery. That’s the kind of value that makes rebuilt title vehicles worth a serious look for buyers who do their homework.

Pro Tip: Always check the rebuilt vs. clean title price differences for your specific make and model before negotiating. Regional market data can shift the discount range by several percentage points.

Insurance, financing, and resale: the real-world implications

Pricing is only part of the story. A rebuilt title touches three other areas of ownership worth understanding before you buy.

Insurance. Insuring a rebuilt title vehicle is more straightforward than many online sources suggest — you can insure one, and full coverage is available too. Liability is offered by essentially every carrier, and most major insurers write comprehensive and collision on rebuilt titles as well; a few just ask for a photo inspection first. Carriers like Progressive, USAA, and Geico are among the most accommodating. Premiums can run somewhat higher than a comparable clean title vehicle, so the smart move is to get a couple of quotes before you finalize a purchase, not after.

Financing. Financing a rebuilt title vehicle is very doable. Plenty of banks and credit unions lend on them, with credit unions often the most flexible — the idea that no one will finance a rebuilt title is a myth. Terms vary by lender, so it pays to shop around, and solid repair documentation makes approval smoother. See our full guide on financing a rebuilt title car.

Resale. The rebuilt title brand is permanent and follows the vehicle for life. That means when you eventually sell, you pass along the same discount you enjoyed as a buyer. Rebuilt title vehicles are best suited for buyers who plan to own for a while and get their value through use — buy it to drive it, and the math works strongly in your favor.

Here’s a quick checklist before you commit to a rebuilt title purchase:

- Get a couple of insurance quotes, including comprehensive and collision coverage

- Line up financing — banks and credit unions both lend on rebuilt titles

- Review the vehicle’s full history documentation, including pre-repair photos

- Have the vehicle inspected in person by a qualified mechanic

- Factor the resale discount into your long-term ownership cost

Key takeaways

Kelley Blue Book rebuilt title values require manual adjustment because KBB does not automatically account for branded title history — which makes buyer know-how the most valuable tool in any rebuilt title purchase.

| Point | Details |

|---|---|

| KBB requires manual adjustment | Apply a 20-40% reduction to KBB clean title values for rebuilt title vehicles. |

| Damage type shapes the discount | Cosmetic histories retain 65-80% of value; structural or flood histories retain 30-60%. |

| State inspection quality matters | Rebuilt titles from strict states like California and New York carry more resale credibility. |

| Insurance and financing are available | Most insurers cover rebuilt titles (full coverage included) and banks and credit unions finance them — get quotes and shop lenders. |

| Rebuilt titles are permanent | The brand follows the vehicle for life, which is why long-term ownership is the smartest strategy. |

Reading KBB right on a rebuilt title

The most common mistake is simple: a buyer pulls up KBB, sees a number, and assumes it applies to the rebuilt title vehicle in front of them. It doesn’t. KBB is a clean title tool, and using it without adjustment on a branded vehicle is like using a ruler to measure temperature — the right instrument for the wrong job.

The buyers who come out ahead treat KBB as a starting point and build their case from there. They look at the vehicle’s specific history, ask for repair documentation, get an in-person inspection, and pull insurance quotes before they’re emotionally committed. That process takes a few extra hours. The savings can run into the thousands.

It’s also worth pushing back on the idea that a rebuilt title is inherently a compromise. Some of the best-value cars on the market are rebuilt titles with thorough documentation and histories involving nothing more serious than hail or a minor theft recovery. The brand creates a discount regardless of repair quality, which means a well-repaired car is genuinely underpriced relative to its condition. That’s not a risk — that’s an opportunity, if you know how to evaluate it.

For a deeper look at how a rebuilt title affects car value across different vehicle types and histories, that guide is worth your time before you start shopping.

Find your next rebuilt title vehicle on ReVroom

Navigating rebuilt title valuations is a lot easier when the information you need is already in front of you. ReVroom is the marketplace built specifically for rebuilt and branded title vehicles, and every listing includes vehicle history information and pre-repair photos so you can see exactly what you’re evaluating before you ever contact a seller.

You won’t need to guess at the discount or wonder what the vehicle looked like before it was repaired. ReVroom puts that context directly in the listing, saving you the time and cost of tracking it down yourself. For buyers who want to make smart, informed decisions on rebuilt title vehicles at fair prices, the ReVroom marketplace is the place to start. Browse current listings and see the transparency that makes rebuilt title shopping worth the trip.

FAQ

Does Kelley Blue Book have a rebuilt title value calculator?

KBB does not offer a dedicated rebuilt title value calculator. You apply a manual 20-40% reduction to the KBB clean title private party value based on the vehicle’s specific history and repair documentation.

How much does a rebuilt title reduce a car’s KBB value?

A rebuilt title typically means a vehicle sells for 20% to 40% less than its clean title equivalent. The exact figure depends on the type of vehicle history, repair quality, and state inspection standards.

Can you insure a rebuilt title car?

Yes. Liability is available essentially everywhere, and most major insurers write full coverage (collision and comprehensive) on rebuilt titles too — Progressive, USAA, and Geico among them. Premiums can run somewhat higher, so compare a few quotes.

Can you finance a rebuilt title car?

Yes. Plenty of banks and credit unions finance rebuilt title vehicles, with credit unions often the most flexible. Terms vary by lender, so it pays to shop around.

Is a rebuilt title permanent on a vehicle?

A rebuilt title is permanent and stays with the vehicle regardless of subsequent repairs or time. That permanence is what creates the up-front discount you benefit from as a buyer.

What should I check before buying a rebuilt title car?

Review all available vehicle history information and pre-repair photos, get a couple of insurance quotes, line up financing, and have the vehicle inspected in person by a qualified mechanic. For the full process, the how to buy a rebuilt car safely guide covers each step.