Navy Federal Rebuilt Title Loan: What Members Must Know

July 6, 2026

TL;DR:

- Navy Federal considers rebuilt title loans on a case-by-case basis, requiring thorough documentation and strong credit.

- Higher interest rates and strict loan-to-value limits make preparation and timing crucial for approval.

A Navy Federal rebuilt title loan is rarely approved under standard automated underwriting, but it is not impossible. Rebuilt title vehicles, which are cars repaired and restored to drivable condition after an insurance company declared them a total loss, can be up to 50% cheaper than clean title equivalents. That price gap makes financing one genuinely attractive. Navy Federal Credit Union does evaluate rebuilt title applications on a case-by-case basis, and knowing their specific requirements, documentation rules, and the 90-day title submission deadline can be the difference between approval and rejection.

Does Navy Federal finance rebuilt title vehicles?

Navy Federal Credit Union does not have a blanket policy approving rebuilt title loans, but it does not have a blanket rejection policy either. Applications go through a review process that weighs your membership history, credit profile, and the vehicle’s documentation. That nuance matters a lot.

Navy Federal membership is open to active-duty and retired DoD and Coast Guard personnel, veterans, civilian employees, and their families. You must be a member before you can apply for any auto loan. Membership itself is a meaningful factor because loan officers can see your full relationship with the credit union, including your account history and payment record.

The credit union uses automated underwriting as a first pass. Rebuilt titles often trigger a flag in that system because lenders verify vehicle history through the National Motor Vehicle Title Information System (NMVTIS), a federal database that confirms title status and flags prior total-loss designations. An automated decline is not the end of the road. A loan officer can manually review your application, especially if you have a strong credit history and a clean relationship with Navy Federal.

How Navy Federal evaluates rebuilt title loan applications

Navy Federal’s evaluation process for a rebuilt title auto loan goes deeper than a standard used-car loan. Here is what they look at and what you need to prepare.

Membership and credit profile

Your credit score, debt-to-income ratio, and account standing at Navy Federal all feed into the decision. Members with longstanding accounts and strong credit history have a significantly higher chance of approval because loan officers have the discretion to manually override an automated decline. Think of it as having a track record that speaks for you before you even walk in the door.

Vehicle documentation requirements

Rebuilt title loans require more paperwork than standard auto loans. You will need:

- The official rebuilt or reconstructed title issued by your state’s DMV

- A professional vehicle appraisal from a certified appraiser

- Repair records showing the scope and quality of work performed

- A vehicle inspection report confirming roadworthy condition

- Photos of the vehicle before and after repairs, when available

The 90-day title submission rule

This is the rule that catches most buyers off guard. Navy Federal requires the car title to be submitted within 90 days of loan funding. If DMV processing delays push that deadline, the lender may require refinancing or accelerate the loan balance. Start the title transfer process the same day you close the purchase.

Loan-to-value limits

Rebuilt title loans carry stricter loan-to-value (LTV) ratios than clean title loans. Expect Navy Federal to lend against 60%–80% of the vehicle’s appraised value, not the purchase price. That gap means you need a larger down payment ready.

Pro Tip: Get your vehicle appraised by a certified appraiser before you apply, not after. An appraisal that aligns with Navy Federal’s collateral standards removes one of the biggest friction points in the review process.

What are typical rebuilt title loan rates and terms?

Rebuilt title loan rates run higher than standard used-car loans, and the gap is not trivial. Rebuilt title loans typically carry interest rates between 13% and 16%, compared to average used-car loan rates of around 10.5% in early 2026. That 2–5 percentage point premium reflects the lender’s higher perceived risk on a vehicle with a prior total-loss history.

The stricter LTV limits compound the cost. If a lender will only finance 70% of a $20,000 appraised value, you need $6,000 as a down payment before the loan even starts. Buyers who come in underprepared often stall at this stage.

| Feature | Rebuilt title loan | Clean title loan |

|---|---|---|

| Typical interest rate | 13%–16% | 8%–11% |

| Loan-to-value ratio | 60%–80% | Up to 100% |

| Down payment required | Higher (20%–40%) | Lower (0%–10%) |

| Gap insurance available | No | Yes |

| Full coverage required | Yes | Yes |

Insurance requirements add another layer. Lenders require full comprehensive and collision coverage for rebuilt title vehicles. Gap insurance, which covers the difference between what you owe and what the car is worth if it is totaled, is not available for rebuilt titles. Insurance companies exclude rebuilt vehicles from gap coverage because the vehicle’s value is harder to establish. That means if the car is totaled, you could owe more than the insurance payout covers.

Pro Tip: Shop for full coverage insurance quotes before you apply for the loan. Some insurers charge significantly more for rebuilt titles, and knowing your premium upfront helps you budget accurately for the full cost of ownership.

What are the alternatives if Navy Federal won’t approve your loan?

Many national banks refuse rebuilt title loans outright because their automated systems flag non-standard titles and reject applications without human review. Navy Federal is more flexible than most large banks, but if they decline, you have real options.

Here are the most practical alternatives:

- Local credit unions. Smaller credit unions often use manual underwriting as a default, not an exception. A loan officer who knows your community and your financial history can approve a rebuilt title loan that a national bank’s algorithm would never touch. Check out how credit unions approach rebuilt titles for a closer look at their flexibility.

- Personal loans. Personal unsecured loans are often the best path for borrowers with good credit who cannot get a rebuilt title auto loan. They require no vehicle collateral, which sidesteps the appraisal and title complications entirely. The trade-off is a slightly higher interest rate and no vehicle-specific protections.

- Specialty lenders. A small number of lenders specialize in non-standard title financing. These lenders understand rebuilt vehicle valuations and build their underwriting around them. Rates tend to be higher, but approval rates are better.

- Dealer financing programs. Some dealers who specialize in rebuilt title vehicles have relationships with lenders who accept non-standard titles. Ask the dealer directly whether they offer in-house financing or have preferred lender partners.

The rebuilt title market is growing, and lender options are expanding with it. Persistence and preparation pay off here.

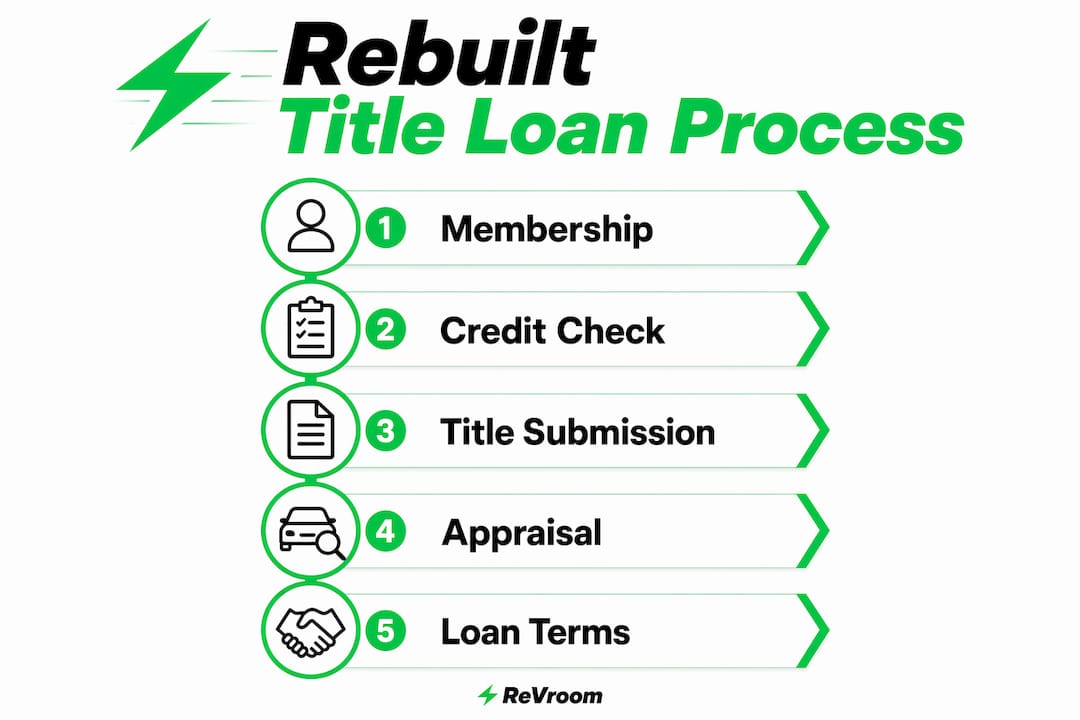

How to apply for a Navy Federal rebuilt title loan step by step

Getting approved for a rebuilt title loan at Navy Federal takes preparation. Follow these steps to give yourself the best shot.

-

Confirm your Navy Federal membership. You must be an active member before applying. If you are eligible but not yet a member, open an account and establish a positive history before you apply for the loan.

-

Gather your vehicle documentation. Collect the rebuilt title, all repair records, a certified appraisal, and a current inspection report. Review the full rebuilt title documentation checklist so nothing is missing when you submit.

-

Get a professional appraisal. The appraisal must reflect the vehicle’s current market value as a rebuilt title car, not its pre-loss value. Navy Federal uses this figure to calculate the LTV ratio and determine how much they will lend.

-

Apply and prepare for a hard credit inquiry. Navy Federal performs a hard credit pull when you apply for an auto loan. Know your credit score beforehand and address any errors on your report before submitting.

-

Start the title transfer immediately after purchase. The 90-day title submission deadline is firm. File the paperwork with your DMV the same week you close the deal. DMV processing times vary by state, and delays are common.

-

Follow up with Navy Federal on collateral documentation. After the DMV processes the title, confirm that Navy Federal has received and recorded it as the lienholder. Do not assume the paperwork moved on its own.

Pro Tip: Call Navy Federal’s loan servicing team directly after submitting your title to the DMV. Confirming receipt before the 90-day window closes protects you from an unexpected loan acceleration.

Key Takeaways

A Navy Federal rebuilt title loan is possible for well-prepared members, but the 90-day title rule, stricter LTV limits, and higher interest rates make documentation and timing the deciding factors.

| Point | Details |

|---|---|

| Navy Federal membership required | You must be an eligible member before applying for any auto loan. |

| 90-day title submission rule | Submit the rebuilt title to Navy Federal within 90 days of funding or risk loan acceleration. |

| Higher rates and lower LTV | Rebuilt title loans run 13%–16% interest with LTV limits of 60%–80%, requiring larger down payments. |

| Manual underwriting is your ally | Longstanding members with strong credit can request manual review to override an automated decline. |

| Alternatives exist | Local credit unions, personal loans, and specialty lenders offer viable paths if Navy Federal declines. |

The honest truth about rebuilt title financing at Navy Federal

From where we sit at Revroom, the biggest mistake buyers make with rebuilt title financing is treating it like a standard auto loan application. It is not. The paperwork burden is real, the timeline is tight, and the 90-day title rule is a genuine trap for buyers who close a deal and then assume the administrative side will sort itself out.

Navy Federal is one of the better large credit unions for this type of financing precisely because they allow manual underwriting. That human element matters. If you have been a member for years, paid your bills on time, and walk in with a clean appraisal and a complete documentation package, a loan officer has real room to say yes. That is not true at most national banks, where the algorithm has the final word.

The rate premium on rebuilt title loans is the other thing worth being honest about. Paying 13%–16% on a car that cost you 40% less than its clean-title equivalent can still be a great financial decision. Run the numbers on total cost of ownership, not just the sticker price. A rebuilt title vehicle with a solid repair history, full coverage insurance, and a reasonable loan rate can be one of the smartest buys in the used-car market right now.

Start with your Navy Federal relationship. If that door closes, walk to your nearest local credit union and ask for a loan officer by name. The personal relationship still counts in this corner of the lending world.

— Revroom Editorial Team

Rebuilt title vehicles worth financing: find them on Revroom

Financing a rebuilt title vehicle starts with finding the right car. That part is harder than it sounds when you are shopping on general marketplaces with no vehicle history context.

Revroom is the only marketplace built specifically for rebuilt title vehicles. Every listing includes vehicle history information and pre-repair photos so you can evaluate what actually happened before you commit. You can also run a Revroom History Report on any rebuilt title vehicle for $15, giving you a full picture of the vehicle’s history, repair severity, and fair market value compared to clean-title cars in your area. When you know exactly what you are buying, financing conversations with Navy Federal or any lender go much smoother. Browse rebuilt title cars for sale on Revroom and find a vehicle worth financing.

FAQ

Will Navy Federal finance a rebuilt title vehicle?

Navy Federal does not automatically approve rebuilt title loans, but applications are reviewed on a case-by-case basis. Members with strong credit history and complete vehicle documentation have the best chance of approval through manual underwriting.

What is the 90-day rule for Navy Federal auto loans?

Navy Federal requires the car title to be submitted within 90 days of loan funding. Missing this deadline can trigger loan acceleration or a required refinancing, so start the DMV title transfer process immediately after purchase.

What interest rates should I expect on a rebuilt title loan?

Rebuilt title loans typically carry interest rates between 13% and 16%, which is 2–5 percentage points higher than standard used-car loan rates. The exact rate depends on your credit score, loan term, and the lender’s LTV assessment.

Can I get gap insurance on a rebuilt title vehicle?

Gap insurance is not available for rebuilt title vehicles. Insurance companies exclude rebuilt titles from gap coverage, so if the car is totaled, you may owe more than the insurance payout covers.

What are the best alternatives if Navy Federal declines my application?

Local credit unions with manual underwriting policies, personal unsecured loans, and specialty lenders focused on non-standard titles are the strongest alternatives. A step-by-step financing guide can help you evaluate which path fits your credit profile and budget.