Salvage Title Insurance: Everything You Need to Know

November 30, 2025

Most american drivers are surprised to learn that over 50 percent of rebuilt vehicles struggle to get full insurance coverage after receiving a salvage title. If you have considered buying or insuring a salvage vehicle, you already know the process comes with strict rules and unexpected hurdles. Understanding how salvage title insurance coverage works can help you protect your investment, avoid financial surprises, and make more confident choices when dealing with complex insurance options.

Table of Contents

- Understanding Salvage Title Insurance Coverage

- Types Of Vehicles Qualifying For Salvage Insurance

- How Salvage Title Insurance Works In Practice

- Legal Restrictions And State Requirements

- Costs, Payout Limits, And Common Pitfalls

- Comparing Salvage Insurance With Other Coverage

Key Takeaways

| Point | Details |

|---|---|

| Salvage Title Insurance Limitations | Coverage is often limited to liability only, with comprehensive and collision options typically unavailable. |

| Inspection Requirements | A detailed vehicle inspection is mandatory before policy approval, assessing repair quality and safety. |

| Increased Costs | Higher premiums and reduced actual cash value payouts are common due to the increased risk associated with salvage vehicles. |

| Legal Compliance | State regulations require comprehensive documentation and disclosure of vehicle history to protect buyers. |

Understanding Salvage Title Insurance Coverage

When it comes to rebuilt vehicles, insurance coverage can feel like navigating a complex maze. According to DMV.org, salvage title vehicles present unique challenges in obtaining comprehensive insurance protection.

Insurance companies approach salvage title vehicles with significant caution. Salvage title insurance typically involves more restrictive coverage options compared to standard vehicle policies. As LegalClarity explains, insurers conduct rigorous assessments to determine potential risks before offering coverage.

Here are key considerations for salvage title insurance coverage:

- Most insurers will only offer liability coverage

- Comprehensive and collision coverage are often limited or unavailable

- Detailed vehicle inspection is usually required before policy approval

- Actual cash value payouts are significantly reduced

The primary goal for insurance providers is risk mitigation. While obtaining full coverage might seem challenging, many insurance companies will work with rebuilt title vehicles if proper documentation and professional repair certifications are provided. Working with an experienced insurance agent who understands rebuilt titles can help you navigate these complex requirements.

When exploring salvage title insurance, prepare for potentially higher premiums and more stringent underwriting processes. What is a Salvage Title? provides additional context about these unique vehicle classifications and can help you understand the broader landscape of rebuilt vehicle insurance.

Types Of Vehicles Qualifying For Salvage Insurance

Not every damaged vehicle automatically qualifies as a salvage title vehicle. According to VIN Lookup, each state has unique criteria for determining when a vehicle receives a salvage designation, typically involving specific damage thresholds and assessment processes.

Iowa Legal Aid highlights that salvage title classifications generally depend on the percentage of damage relative to a vehicle’s fair market value. Most states consider a vehicle salvage when repair costs exceed 75% of the car’s total value, though exact percentages can vary significantly by jurisdiction.

Typical vehicles that might qualify for salvage insurance include:

- Vehicles damaged in major accidents

- Cars with extensive flood or water damage

- Vehicles recovered after theft with significant structural damage

- Cars with severe hail or weather-related damage

- Vehicles with frame or structural damage exceeding repair cost thresholds

Understanding these nuanced classifications is crucial for potential buyers and insurers. While some vehicles might seem heavily damaged, they could still be repairable and insurable with proper documentation. Salvage Title Vehicle Value Guide provides additional insights into evaluating these unique vehicles and understanding their potential insurance implications.

How Salvage Title Insurance Works In Practice

Insuring a vehicle with a salvage title is a complex process that requires careful navigation. According to LegalClarity, insurers have specific underwriting criteria that significantly impact coverage options for these unique vehicles.

DMV.org explains that the insurance process for salvage title vehicles typically involves multiple critical steps. Comprehensive inspection is the first and most crucial requirement, where insurance providers thoroughly assess the vehicle’s current condition, repair quality, and overall safety before considering any coverage.

The practical insurance process for salvage title vehicles usually follows these steps:

- Initial professional vehicle inspection

- Detailed repair documentation review

- Verification of structural and mechanical integrity

- Limited coverage determination

- Potential premium rate adjustments

Most insurance companies will only offer liability coverage for salvage title vehicles, which means comprehensive and collision protections are often unavailable. This limitation stems from the increased uncertainty surrounding the vehicle’s previous damage and potential future risk. Potential buyers should understand that insurance providers are primarily concerned with minimizing their financial exposure when dealing with rebuilt vehicles.

Navigating the insurance landscape for salvage title vehicles requires patience and thorough documentation. Salvage Title Defined: Complete Guide for Buyers can provide additional insights into understanding the nuanced world of salvage title insurance and help buyers make informed decisions about their vehicle coverage.

Legal Restrictions And State Requirements

Legal regulations surrounding salvage title vehicles are complex and vary significantly across different states. According to GovInfo, federal and state governments have implemented strict consumer protection measures to ensure transparency and safety in the rebuilt vehicle market.

Nebraska DMV provides insight into the intricate legal framework governing salvage titles. Each state maintains unique requirements for vehicle title branding, with most jurisdictions mandating comprehensive documentation and disclosure processes to protect potential buyers.

Key legal restrictions typically include:

- Mandatory vehicle damage disclosure

- Required professional inspection before registration

- Specific title branding and documentation protocols

- Restrictions on selling vehicles without proper reconstruction certification

- Limitations on transferring ownership without complete repair documentation

State regulations often impose significant penalties for misrepresenting a vehicle’s salvage history. Sellers must provide complete repair records and undergo stringent verification processes to legally rebrand a vehicle. These requirements aim to prevent fraud and ensure public safety by creating a transparent mechanism for tracking and documenting vehicle reconstruction.

Understanding these nuanced legal landscapes can be challenging for individual buyers. Salvage Title Defined: Complete Guide for Buyers offers additional resources to help navigate the complex world of salvage title regulations and protect your interests when considering a rebuilt vehicle.

Costs, Payout Limits, And Common Pitfalls

Navigating the financial landscape of salvage title insurance requires careful understanding of unique economic challenges. According to LegalClarity, salvage vehicles present complex valuation issues that significantly impact insurance costs and potential claim payouts.

DMV.org highlights that insurance premiums for salvage title vehicles can be substantially different from standard vehicle coverage. Insurers typically assess these vehicles with heightened scrutiny, resulting in higher rates and more restrictive coverage options due to perceived increased risk.

Common financial pitfalls for salvage title vehicle owners include:

- Dramatically reduced market value compared to similar clean title vehicles

- Limited insurance coverage options

- Higher insurance premium rates

- Potential disputes during claim settlements

- Significant depreciation in vehicle value

Most insurance providers calculate payouts based on the vehicle’s actual cash value before the damage occurred, which can be substantially lower than the owner’s initial investment. This means that even with insurance, owners might receive significantly less compensation than expected. Potential buyers must carefully evaluate the long-term financial implications of purchasing a salvage title vehicle, understanding that the initial cost savings might be offset by future insurance and repair challenges.

Salvage Title Defined: Complete Guide for Buyers can help you understand the intricate financial landscape of salvage title vehicles and make more informed decisions about your potential investment.

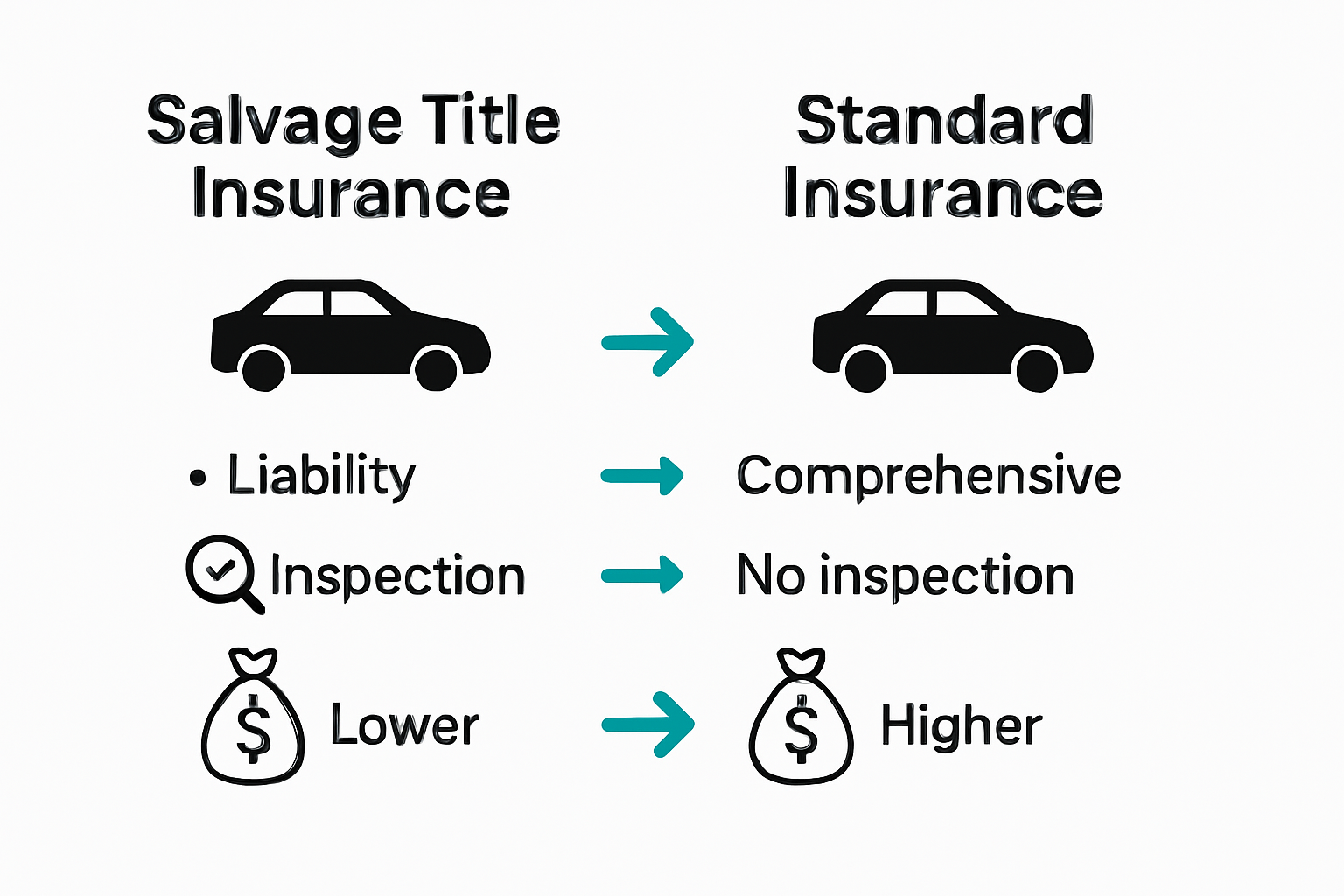

Comparing Salvage Insurance With Other Coverage

Salvage title insurance presents a dramatically different landscape compared to standard vehicle coverage. According to LegalClarity, the underwriting process for salvage vehicles involves unique risk assessments that fundamentally alter traditional insurance approaches.

DMV.org highlights key differences between salvage insurance and conventional vehicle coverage. While standard insurance policies typically offer comprehensive protection, salvage title insurance is characterized by significant limitations and more stringent requirements.

Key comparison points between salvage and standard insurance include:

- Restricted comprehensive and collision coverage

- Higher premium rates for salvage vehicles

- More extensive documentation requirements

- Limited claim settlement options

- Significantly reduced actual cash value assessments

Most standard insurance policies provide full-value protection and straightforward claims processes. In contrast, salvage title insurance focuses primarily on liability coverage, with insurers meticulously evaluating the vehicle’s reconstruction quality and potential future risks. Potential buyers must understand that these differences can dramatically impact long-term financial protection and vehicle value.

What Insurance Covers Rebuilt Titles offers additional insights into navigating the complex world of salvage and rebuilt title insurance, helping buyers make informed decisions about their vehicle coverage.

Go Further With Confidence in Rebuilt Title Vehicles

Understanding salvage title insurance is a crucial step in making smart vehicle decisions. The article highlights common challenges such as limited coverage options, higher premiums, and detailed inspections that can complicate insurance for vehicles with complex histories. If you are navigating these obstacles, you want more than just information—you want transparency and peace of mind when buying or selling a rebuilt title vehicle.

At ReVroom, we meet this need head on. Unlike typical marketplaces, we focus exclusively on rebuilt title cars, not salvage titles, providing complete accident history and clear photos of a vehicle before repairs. Our platform removes the guesswork and costly investigations, empowering you to find reliable cars at significant savings—up to 50% less than clean title counterparts.

Explore our carefully curated listings and see why thousands of buyers trust ReVroom to deliver upfront transparency and fair deals. Ready to avoid the common pitfalls of salvage title insurance and discover vehicles with stories and savings? Visit ReVroom today and enjoy a smarter, safer, and more confident way to buy rebuilt title cars. To dive deeper into how rebuilt titles compare insurance wise, check out What Insurance Covers Rebuilt Titles and for a complete understanding of vehicle classifications visit Salvage Title Defined: Complete Guide for Buyers. Going further starts here.

Frequently Asked Questions

What is salvage title insurance?

Salvage title insurance is a specific type of insurance designed for vehicles that have been deemed salvage due to significant damage. It typically offers limited coverage options compared to standard vehicle policies, primarily focusing on liability insurance.

How does obtaining insurance for a salvage title vehicle work?

Obtaining insurance for a salvage title vehicle typically involves a detailed inspection of the vehicle, review of repair documentation, and assessment of the vehicle’s current condition. Insurers often require thorough verification before offering coverage.

What are the typical coverage limitations of salvage title insurance?

Coverage limitations for salvage title insurance often include restricted comprehensive and collision coverage, and higher premiums compared to standard vehicle insurance. Many insurers will only offer liability coverage, limiting overall financial protection.

Why might my salvage title vehicle’s insurance have higher premiums?

Salvage title vehicles are viewed as higher risk by insurance providers due to their history of significant damage. This perceived risk leads to higher premiums and more stringent underwriting processes compared to vehicles with clean titles.