Understanding title branding: a guide for budget buyers

March 23, 2026

Most budget-conscious car shoppers believe a branded title automatically means a dangerous, unreliable vehicle. That’s not always true. Title branding simply signals a vehicle’s history, and understanding these labels can unlock serious savings for families and students seeking affordable, dependable transportation. This guide breaks down what title branding really means, clarifies rebuilt title basics, and delivers practical tips to help you confidently navigate the market and find a safe, budget-friendly car that fits your needs without unnecessary risk.

Table of Contents

- Key takeaways

- What is title branding and why does it matter?

- Understanding rebuilt titles: repair, inspection, and state rules

- Risks and challenges: insurance, financing, and safety considerations

- Smart buying tips for budget-conscious families and students

- Explore dependable rebuilt title cars with ReVroom

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Branded titles signal history | Branded titles reveal that a car has a notable history beyond a clean title and signal the need for careful risk assessment. |

| Rebuilt means repaired and inspected | A rebuilt title means the vehicle was repaired after a total loss and passed state safety inspections, making it roadworthy when properly vetted. |

| Insurance and financing rules | Insurance and financing may carry special terms for branded vehicles, affecting premiums, coverage options, or loan eligibility. |

| Safety varies with vetting | Safety and reliability vary widely, so thorough vetting and independent inspections are essential. |

| Budget buyers weigh risks | Budget buyers can save money with branded vehicles but should weigh potential repair costs and long term reliability. |

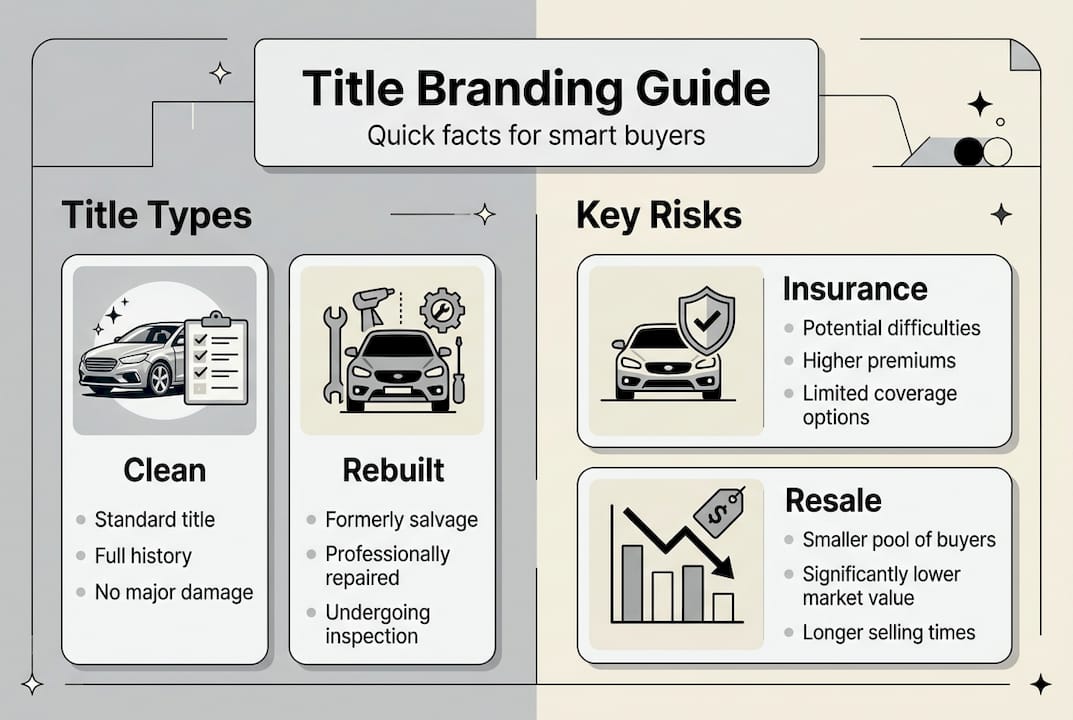

What is title branding and why does it matter?

Title branding refers to a vehicle title that carries a designation other than ‘clean,’ indicating significant past events, such as rebuilt, flood, or lemon law issues. These labels exist to inform buyers about a car’s history and help them make educated purchasing decisions. Not all branded titles are created equal. Some signal minor cosmetic repairs, while others indicate more complex histories.

The most common types of title branding include:

- Rebuilt: Vehicle was repaired after a total loss declaration and passed state inspections

- Flood: Car sustained water damage from natural disasters or flooding events

- Lemon law: Vehicle had repeated mechanical defects covered under manufacturer warranty

- Theft recovery: Car was stolen, recovered, and may have sustained minor issues

Understanding these distinctions matters because they directly affect a vehicle’s value, insurance costs, and long-term reliability. A rebuilt title from hail repair carries far different implications than one from flood exposure. Knowing the difference between salvage vs. rebuilt titles empowers you to assess risk accurately and avoid overpaying or buying a vehicle unsuited to your needs. Title branding isn’t inherently bad. It’s a transparency tool that, when properly understood, helps budget buyers access affordable cars while making informed choices about safety and value.

Understanding rebuilt titles: repair, inspection, and state rules

A rebuilt title tells a story of revival. A rebuilt title is issued to a vehicle previously declared a total loss by an insurer when repair costs exceed 50-90% of value, varying by state, after repairs and passing state safety inspections. This process transforms a vehicle from undrivable to roadworthy, but the journey from total loss to rebuilt involves several critical steps.

Here’s how a vehicle earns a rebuilt title:

- Insurance company declares the vehicle a total loss based on repair cost thresholds

- Owner or buyer purchases the vehicle and completes comprehensive repairs

- Vehicle undergoes state-mandated safety inspection to verify roadworthiness

- State DMV issues a rebuilt title once inspection requirements are satisfied

- Vehicle can be legally registered, insured, and driven on public roads

State regulations create significant variation in inspection rigor and branding practices. Inspection methodologies vary by state: e.g., NY brands ‘REBUILT SALVAGE’ for vehicles 8 years or newer with damage over 75% value; CA requires CHP inspection and smog checks; FL needs photos and receipts; focus on VIN, brakes, and structure, but not always long-term reliability. These differences mean a rebuilt title from one state may represent more thorough vetting than another.

| State | Inspection Focus | Branding Label | Key Requirements |

|---|---|---|---|

| New York | VIN, structure, brakes | REBUILT SALVAGE | Vehicles 8+ years, damage >75% value |

| California | CHP inspection, smog | REVIVED SALVAGE | Full mechanical and emissions testing |

| Florida | Photos, receipts, VIN | REBUILT | Documentation of repairs and parts |

Pro Tip: Research your state’s specific rebuilt title inspection standards before purchasing. States with stricter inspection protocols generally produce more reliable rebuilt vehicles. Understanding rebuilt cars retitling process helps you evaluate whether a vehicle meets your safety and quality expectations.

The variation in state rules means buyers must do extra homework. A rebuilt title alone doesn’t guarantee quality. It confirms a vehicle passed minimum safety standards in a particular state. Your job is to dig deeper, verify repair quality, and ensure the vehicle meets your personal standards for reliability and safety.

Risks and challenges: insurance, financing, and safety considerations

Owning a rebuilt title vehicle comes with unique hurdles that can impact your wallet and peace of mind. While the upfront savings are attractive, you need to understand the ongoing challenges before committing to a purchase. These obstacles aren’t dealbreakers, but they require realistic planning and careful evaluation.

Insurance and financing present the most immediate challenges:

- Limited insurance coverage: Only ~20% of companies fully cover rebuilt titles; often liability only, with higher premiums 20-40% above clean title rates

- Financing hurdles: Limited to credit unions or subprime lenders, with higher rates of 8-20% APR, 10-20% down payments required, and lower loan-to-value ratios of 70-80%

- Higher out-of-pocket costs: Reduced coverage means you’ll pay more for repairs if something goes wrong

- Fewer lender options: Many traditional banks refuse to finance rebuilt title vehicles entirely

Safety concerns add another layer of complexity. State inspections ensure basic roadworthiness, but experts like Consumer Reports advise caution due to variable repair quality and no re-crash tests; some maintain 4-5 star ratings post-repair. The inspection process verifies brakes, lights, and structural integrity, but it doesn’t guarantee the vehicle will perform reliably over years of ownership.

“Rebuilt title vehicles pass minimum safety standards, but inspection protocols vary widely. Buyers must verify repair quality independently through trusted mechanics and comprehensive vehicle history reports to avoid hidden issues like frame misalignment or flood exposure.”

Hidden problems pose real risks. Flood history can lead to electrical failures months after purchase. Frame repairs might compromise crash safety even if the car drives smoothly. Substandard bodywork can hide rust or structural weaknesses. These issues aren’t always visible during a test drive or casual inspection.

Pro Tip: Never skip a pre-purchase inspection by an independent mechanic experienced with rebuilt vehicles. This $100-200 investment can save you thousands by identifying hidden issues before you buy. Check out our rebuilt title car safety guide for detailed inspection checklists.

Long-term ownership considerations matter too. Resale values for rebuilt title vehicles remain lower than clean title equivalents, limiting your ability to recoup your investment. Future buyers will scrutinize the vehicle’s history just as carefully as you should now. Understanding financing rebuilt title vehicles helps you plan for both purchase and eventual resale scenarios.

Smart buying tips for budget-conscious families and students

Navigating the rebuilt title market successfully requires a strategic approach focused on transparency, verification, and realistic expectations. These actionable steps help you maximize savings while minimizing risk, ensuring you drive away with a vehicle that serves your family or student needs reliably.

Follow these essential steps when shopping for rebuilt title vehicles:

- Run comprehensive vehicle history checks: For budget families and students, prioritize NMVTIS checks, mechanic inspections, and review of repair documentation to verify accident history, title brands, and odometer readings across all states

- Get an independent mechanic inspection: Hire a trusted mechanic to perform a thorough pre-purchase inspection, focusing on frame integrity, electrical systems, and signs of flood exposure or poor repairs

- Review all repair documentation carefully: Request invoices, parts receipts, and before-and-after photos to verify the scope and quality of repairs performed

- Avoid flood and theft-branded vehicles: These histories carry higher risks of hidden electrical problems, mold, or missing components that surface months after purchase

- Plan for long-term ownership: Rebuilt title vehicles work best when you intend to keep them for years, minimizing resale challenges and maximizing your savings over time

- Assess your mechanical skills honestly: If you’re comfortable handling minor repairs and maintenance, rebuilt vehicles offer better value; if not, factor in higher repair costs

Pro Tip: Cross-reference multiple vehicle history sources including NMVTIS, Carfax, and AutoCheck. No single report captures everything, and discrepancies between reports can reveal hidden issues or incomplete repair histories.

Budget buyers should weigh the 20-50% savings against practical ownership realities. Insurance will cost more. Financing will be harder to secure. Resale value will remain lower. But if you’re buying a reliable daily driver to keep for 5-10 years, these tradeoffs can work in your favor. The key is matching the vehicle to your specific situation, needs, and comfort level with potential unknowns.

Consider your lifestyle and usage patterns. Families needing a dependable minivan for school runs benefit from rebuilt title savings if the vehicle passes rigorous inspection. Students seeking basic transportation for a few years can stretch limited budgets further with a well-vetted rebuilt sedan. The best rebuilt title cars for budget buyers align with your practical needs while minimizing exposure to high-risk vehicle histories.

Understanding the risks of rebuilt title vehicles helps you make informed decisions. Not every rebuilt vehicle is a smart buy, but with proper vetting, many offer exceptional value for budget-conscious buyers willing to do their homework.

Explore dependable rebuilt title cars with ReVroom

Now that you understand title branding and know how to evaluate rebuilt vehicles safely, it’s time to explore your options. ReVroom makes finding affordable, transparent rebuilt title vehicles easier than ever for budget-conscious families and students.

Unlike traditional marketplaces, ReVroom includes accident history information and before-repair photos in every listing, removing the $150 average vetting cost buyers typically face. You can easily compare vehicles, spot red flags, and identify the best options without expensive reports or guesswork. Our platform connects you with sellers offering properly repaired vehicles at prices that fit your budget, backed by the transparency you need to buy confidently. Explore our rebuilt title safety guide for expert insights, then browse listings to find your next dependable ride.

FAQ

What does a rebuilt title mean for insurance coverage?

Most insurers limit coverage to liability only, with premiums running 20-40% higher than clean title equivalents. Only about 20% of insurance companies offer full coverage for rebuilt title vehicles. Shop around with multiple providers and expect higher costs due to the vehicle’s history. Some insurers specialize in rebuilt title coverage and may offer more competitive rates.

Can a rebuilt title vehicle be financed like a clean title car?

Financing options are significantly more limited. You’ll typically need to work with credit unions or subprime lenders who charge 8-20% APR, require 10-20% down payments, and offer lower loan-to-value ratios of 70-80%. Traditional banks often refuse to finance rebuilt title vehicles entirely. Know your financing terms upfront and secure pre-approval before shopping to avoid surprises at purchase time.

How can I verify a vehicle’s title brand before purchase?

Use NMVTIS reports, state DMV checks, and comprehensive vehicle history services to verify title brands and accident history. Cross-check the VIN across multiple sources since no single report captures everything. Request detailed repair documentation, before-and-after photos, and inspection records from the seller. An independent mechanic inspection is essential to confirm the vehicle’s current condition matches its documented history.

Are rebuilt title cars reliable and safe for families and students?

They can be safe and reliable when properly repaired and thoroughly inspected, but quality varies widely between vehicles. State inspections ensure basic roadworthiness, but don’t guarantee long-term reliability or crash safety. Proceed cautiously by getting expert mechanic inspections, reviewing all repair documentation, and considering your long-term ownership plans. Budget buyers who do thorough homework can find excellent value, but due diligence is non-negotiable for family safety.

Recommended

- Branded Title Vehicles: Complete Guide for Buyers | ReVroom

- Branded Car Titles Explained: Costs, Myths, and Value | ReVroom

- Branded Title Explained: The Complete Buyer Guide | ReVroom

- Should I Buy a Branded Title Car? Complete Guide | ReVroom

- Budget voor Thuisstudio: Van Beginnersset tot Professionele Setup - https://i4studio.nl/