Does Insurance Cost More for a Rebuilt Title Car?

May 26, 2026

TL;DR:

- Most major insurers will cover rebuilt title cars with standard liability at minimal additional cost. Full coverage premiums typically increase by 15% to 30%, but purchase savings help offset these higher expenses. Thorough documentation and proactive insurer communication are essential for affordable coverage and risk mitigation.

You’ve spotted a great deal on a rebuilt title vehicle and the price looks almost too good to pass up. Then the question hits you: does insurance cost more for a rebuilt title, and will it eat up all those savings? It’s one of the most Googled questions in the rebuilt title space, and honestly, the answers floating around online are all over the map. Some say you’ll pay a fortune. Some say you can’t get covered at all. The truth is more nuanced and a lot more encouraging than the internet wants you to believe.

Table of Contents

- Key Takeaways

- Does insurance cost more for salvage title and rebuilt title cars?

- How much more does insurance actually cost?

- Why insurers charge more for rebuilt title coverage

- How to get the best insurance deal on a rebuilt title car

- Weighing the total picture

- My honest take on rebuilt title insurance

- Find your next rebuilt title car on ReVroom

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Rebuilt titles are insurable | Once a car earns rebuilt title status, most major insurers will cover it with standard liability. |

| Full coverage costs more | Expect to pay 15% to 30% more annually for physical damage coverage versus a clean title car. |

| Liability rates stay close | Liability-only premiums for rebuilt titles typically run within 0% to 5% of clean title rates. |

| Purchase savings offset premiums | Rebuilt title cars cost 20% to 40% less than comparable clean title vehicles, which softens the insurance cost gap. |

| Shop smart before you buy | Confirm insurance availability with your provider before purchase to avoid unwelcome surprises. |

Does insurance cost more for salvage title and rebuilt title cars?

Let’s get the terminology straight first, because this matters a lot when you’re talking to insurance companies. A vehicle with an active pre-repair designation cannot be legally driven on public roads, and insurance is legally unavailable until the car is repaired, passes a state inspection, and receives a rebuilt title. These are two very different designations, and conflating them is where most of the confusion starts.

Once a car holds a rebuilt title, the insurance picture changes significantly. Here’s what coverage actually looks like:

- Liability coverage is broadly available from most major insurers and costs roughly the same as it does for a clean title car. The premium difference for liability only typically lands between 0% and 5%.

- Collision and comprehensive coverage (together called “physical damage” or full coverage) is where you’ll see a real price bump. These coverages are available but more limited, and not every insurer offers them for rebuilt title cars.

- State regulations matter. Coverage options and insurer policies vary by state, so what’s available in Texas may not be available in Michigan.

Pro Tip: Before you fall in love with a listing, call your current insurer and ask specifically whether they write full coverage policies for rebuilt title vehicles in your state. A five-minute phone call can save you a major headache.

The bottom line on eligibility? Getting a rebuilt title car insured is genuinely not that hard. The myth that these cars are impossible or nearly impossible to insure does not hold up. Major carriers including Progressive, GEICO, State Farm, and Nationwide offer policies for rebuilt title vehicles, though availability depends on your state and sometimes on individual agent discretion.

How much more does insurance actually cost?

This is the number everyone wants. So let’s talk dollars and sense.

For full coverage insurance on a rebuilt title car, expect to pay roughly 15% to 30% more annually compared to an equivalent clean title vehicle. Most of that increase lives in the physical damage portion of your policy, not the liability side.

| Coverage type | Rebuilt title vs. clean title cost difference |

|---|---|

| Liability only | 0% to 5% higher |

| Full coverage (collision + comprehensive) | 15% to 30% higher |

| Total loss claim payout | 20% to 30% lower due to diminished value clauses |

That third row deserves its own spotlight. Many policies for rebuilt title vehicles include diminished value clauses that cap total loss payouts at 70% to 80% of clean-title book value. So even if you’re paying for full coverage, a total loss claim may not pay out as much as you’d expect. This is a real consideration, not a dealbreaker, but something to understand before you sign.

Now put that in context. A rebuilt title car typically costs 20% to 40% less than a comparable clean title vehicle. If you’re paying $18,000 for a car that would cost $25,000 with a clean title, the math on a 20% insurance premium increase still looks pretty favorable. The numbers generally work in your favor when you do the full ownership cost calculation.

Why insurers charge more for rebuilt title coverage

Insurance is priced on risk, and insurers see a few specific risk factors with rebuilt title cars that push premiums up on physical damage coverage.

The biggest factor is the possibility of non-obvious structural concerns. A vehicle may pass a state inspection but still carry underlying issues that aren’t visible to the naked eye. From an insurer’s standpoint, that uncertainty justifies a higher premium on the coverage that would pay out if the car were totaled again.

“Vehicles may pass state inspections but still have underlying issues affecting insurability.” — GetCoverr, 2026

A few other factors that influence what you pay:

- Repair documentation. Insurers want to see that repairs were done properly. A state-approved rebuilt inspection certificate is often required before full coverage is approved. The more thorough and well-documented the repair history, the smoother your application goes.

- Resale value. Rebuilt title cars are worth less on the open market, which affects how an insurer calculates your claim settlement. Lower book value means lower maximum payouts, which is partly why diminished value clauses exist.

- Insurer appetite. Some national carriers restrict rebuilt title coverage entirely or require photo inspections and professional appraisals before they’ll approve a policy. This is insurer-by-insurer, not a universal rule.

Pro Tip: Gather all repair documentation and inspection certificates before you apply for coverage. Presenting thorough records upfront signals to underwriters that the vehicle was repaired properly, and it genuinely speeds up the approval process.

How to get the best insurance deal on a rebuilt title car

Getting covered doesn’t have to be a chore. Here’s how to approach it like someone who’s done this before.

-

Contact insurers before you buy. This is the single most effective step. Confirm that your preferred carrier will write a policy for the specific vehicle you’re considering, in your state, at the coverage level you want. Don’t assume.

-

Work with an independent insurance agent. Many buyers are surprised to find their current insurer won’t cover rebuilt title cars. Independent agents have access to multiple carriers, including niche providers that specialize in these policies. They can often find you coverage and pricing that a direct online quote simply won’t surface. You can explore a breakdown by insurer to get a head start on who’s most likely to work with you.

-

Organize your documentation. Have the rebuilt title certificate, repair records, and any inspection results ready before you start applying. This speeds up underwriting and builds credibility with the insurer.

-

Consider liability-only if full coverage doesn’t pencil out. If the premium on full coverage is steep relative to the car’s value, liability-only may be the smarter financial move. This is especially true on older vehicles where the car’s market value is modest anyway.

-

Run the full math before committing. Compare the insurance cost alongside the purchase price savings. For most buyers, the combined cost analysis still favors the rebuilt title vehicle when you account for the lower purchase price.

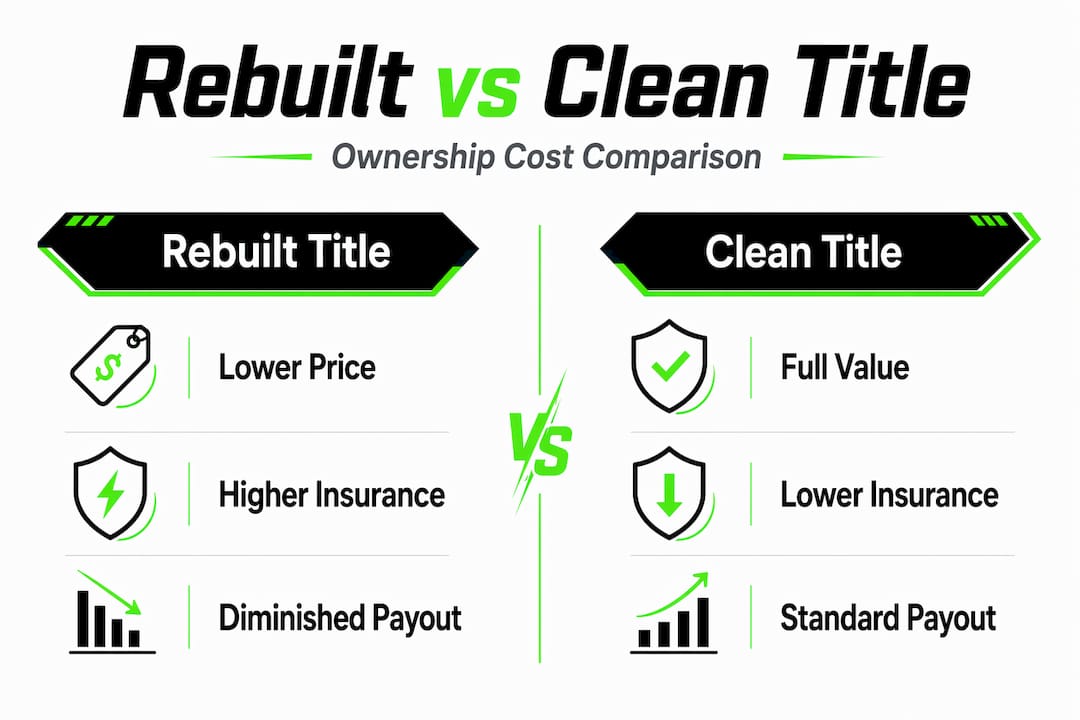

Weighing the total picture

Buying a rebuilt title car is a financial decision that goes well beyond the sticker price. Here’s a quick comparison to frame the real cost tradeoffs:

| Factor | Rebuilt title car | Clean title car |

|---|---|---|

| Purchase price | 20% to 40% lower | Baseline |

| Liability insurance cost | Roughly the same | Baseline |

| Full coverage premium | 15% to 30% higher | Baseline |

| Total loss claim payout | Potentially 20% to 30% lower | Baseline |

| Transparency on vehicle history | Varies widely by seller | Varies widely by seller |

The most important column in that table? Transparency on vehicle history. It’s the variable that can make or break the entire value proposition. A rebuilt title car with thorough, verifiable history and professional repairs is a very different purchase from one with murky documentation. Due diligence isn’t optional here. An in-person inspection by a trusted mechanic before you buy is always worth the cost.

Long-term ownership strategy matters too. If you plan to drive the car for years and prioritize low monthly costs, liability-only coverage on a well-documented rebuilt title car can be a genuinely smart financial choice. If you need full coverage for a loan or personal peace of mind, budget for the premium increase and shop multiple insurance options to find the best rate.

My honest take on rebuilt title insurance

I’ve spent a lot of time in the rebuilt title space, and if I’m being direct: the fear around insuring these cars is wildly overblown. The internet has a habit of amplifying worst-case scenarios, and rebuilt title insurance is a prime example.

Yes, full coverage costs more. Yes, total loss payouts can be lower. Those are real facts worth understanding. But the framing that rebuilt title cars are some kind of insurance nightmare? That’s not the reality I’ve seen. Most buyers who approach this with basic preparation, calling insurers in advance, gathering documentation, using an independent agent, find coverage without drama.

What I’ve learned is that the real risk isn’t the insurance cost. It’s buying a rebuilt title car without knowing its full history. A premium that’s 20% higher is manageable. A vehicle with undisclosed issues is not. That’s why transparency in the purchase process matters so much more than most buyers realize going in.

The buyers who get burned aren’t the ones paying slightly higher premiums. They’re the ones who skipped the inspection and bought without complete vehicle history in hand. Do the homework, and the insurance piece largely takes care of itself.

— Cameron

Find your next rebuilt title car on ReVroom

If the insurance picture is clearer now, the next step is finding a vehicle worth insuring. ReVroom is the only marketplace built specifically for rebuilt title cars, and every listing includes vehicle history information and photos of what the car looked like before it was repaired. You get the transparency upfront, so you can buy with confidence instead of crossed fingers.

Rebuilt title cars can be up to 50% less expensive than comparable clean title vehicles, and with the right documentation in hand, getting them insured is straightforward. Browse the ReVroom marketplace to find listings with the history transparency you need to make a smart, informed decision. Your next great car is probably already there.

FAQ

Can you get full coverage insurance on a rebuilt title car?

Yes. Major insurers including Progressive, GEICO, and State Farm offer full coverage for rebuilt title vehicles, though availability depends on your state and the insurer’s specific underwriting policies.

How much more does rebuilt title insurance cost?

Full coverage insurance for a rebuilt title car typically runs 15% to 30% more per year than a clean title equivalent. Liability-only coverage usually costs within 0% to 5% of clean title rates.

Who insures rebuilt title cars?

National carriers like Progressive, GEICO, State Farm, and Nationwide write policies for rebuilt title vehicles in many states. Working with an independent insurance agent increases your chances of finding the best coverage at a competitive rate.

Does a rebuilt title affect insurance payouts?

Yes. Many policies include diminished value clauses that cap total loss settlements at 70% to 80% of clean-title book value, meaning your payout on a total loss claim may be lower than the original purchase price.

Is it worth buying a rebuilt title car given higher insurance costs?

For most buyers, yes. Rebuilt title cars cost 20% to 40% less to purchase, which typically offsets the modest increase in insurance premiums when you calculate the full ownership cost.