How Much Is Insurance on Rebuilt Title

November 8, 2025

Over 60 percent of insurers limit coverage or charge higher premiums for vehicles with a rebuilt title. Buying one can seem like a smart way to save money on a car, but it brings a new set of insurance hurdles. Understanding how a rebuilt title changes your choices and potential costs helps you avoid costly surprises and plan smarter, whether you are insuring your investment or hoping to save in the long run.

Table of Contents

- What Rebuilt Title Means For Insurance

- Coverage Options And Limitations

- Typical Premium Increases Explained

- Documents Insurers Require

- How To Shop And Save On Coverage

- Resale Value And Claim Payout Impact

Key Takeaways

| Point | Details |

|---|---|

| Insurance Considerations | Rebuilt title vehicles often face limited coverage options and higher premiums, requiring thorough documentation to secure insurance. |

| Premium Increases | Expect premium hikes of 20% to 50% compared to clean title vehicles due to uncertainty in repair history and potential risks. |

| Required Documentation | Insurers require detailed records including repair invoices and inspection reports to evaluate a rebuilt vehicle’s insurability. |

| Resale Challenges | Rebuilt title vehicles typically have lower resale values and reduced claim payouts, making comprehensive maintenance records essential. |

What Rebuilt Title Means For Insurance

When it comes to rebuilt titles and insurance, understanding the landscape is crucial for budget-conscious car buyers. According to legalclarity.org, a rebuilt title indicates a vehicle that was previously deemed a total loss but has been repaired and passed state inspections. This unique status significantly impacts insurance coverage and potential premiums.

Insurers often approach rebuilt title vehicles with extra caution. As dmv.org explains, many insurance companies offer limited coverage options or charge higher premiums due to the vehicle’s complex history. This doesn’t mean insuring a rebuilt title car is impossible - it just requires more strategic planning and research.

Here are key considerations for obtaining insurance on a rebuilt title vehicle:

- Comprehensive Inspection: Most insurers will require a thorough professional inspection before providing coverage

- Limited Coverage Options: You might only qualify for liability insurance initially

- Higher Premiums: Expect to pay 10-30% more compared to similarly aged clean title vehicles

- Documentation is Critical: Maintain all repair and inspection records to demonstrate the vehicle’s roadworthiness

While challenges exist, many insurance providers are becoming more open to rebuilt titles, especially when buyers can demonstrate professional repairs and transparent vehicle history.

The key is preparation, documentation, and working with insurance agents who understand rebuilt title nuances.

The key is preparation, documentation, and working with insurance agents who understand rebuilt title nuances.

For a deeper understanding of navigating insurance with rebuilt titles, check out our comprehensive guide on rebuilt title insurance.

Coverage Options And Limitations

When it comes to insuring a rebuilt title vehicle, understanding the available coverage options is critical. According to autoinsurance.org, insurers are often hesitant to provide comprehensive coverage for rebuilt titles. Most insurance companies will typically limit their offerings to basic liability insurance, reflecting the inherent uncertainties surrounding these vehicles.

The limitations stem from significant challenges in assessing a rebuilt vehicle’s true value and potential hidden structural issues. Insurance providers face difficulty in determining the precise condition and reliability of a car that has previously been declared a total loss. This means you’ll likely encounter more restrictive insurance policies compared to standard clean title vehicles.

Typical insurance coverage options for rebuilt titles include:

- Liability Insurance: The most common and often the only available option

- Minimum State-Required Coverage: Typically the baseline protection

- Limited Comprehensive Coverage: May be available with extensive documentation

- Collision Insurance: Often challenging or extremely expensive to obtain

To improve your chances of securing better insurance, consider these proactive steps:

- Obtain a professional, detailed inspection report

- Maintain comprehensive repair and maintenance documentation

- Work with insurance agents specializing in rebuilt title vehicles

- Be prepared to pay higher premiums for limited coverage

For a more in-depth exploration of insurance strategies for rebuilt titles, check out our comprehensive guide on insurance options.

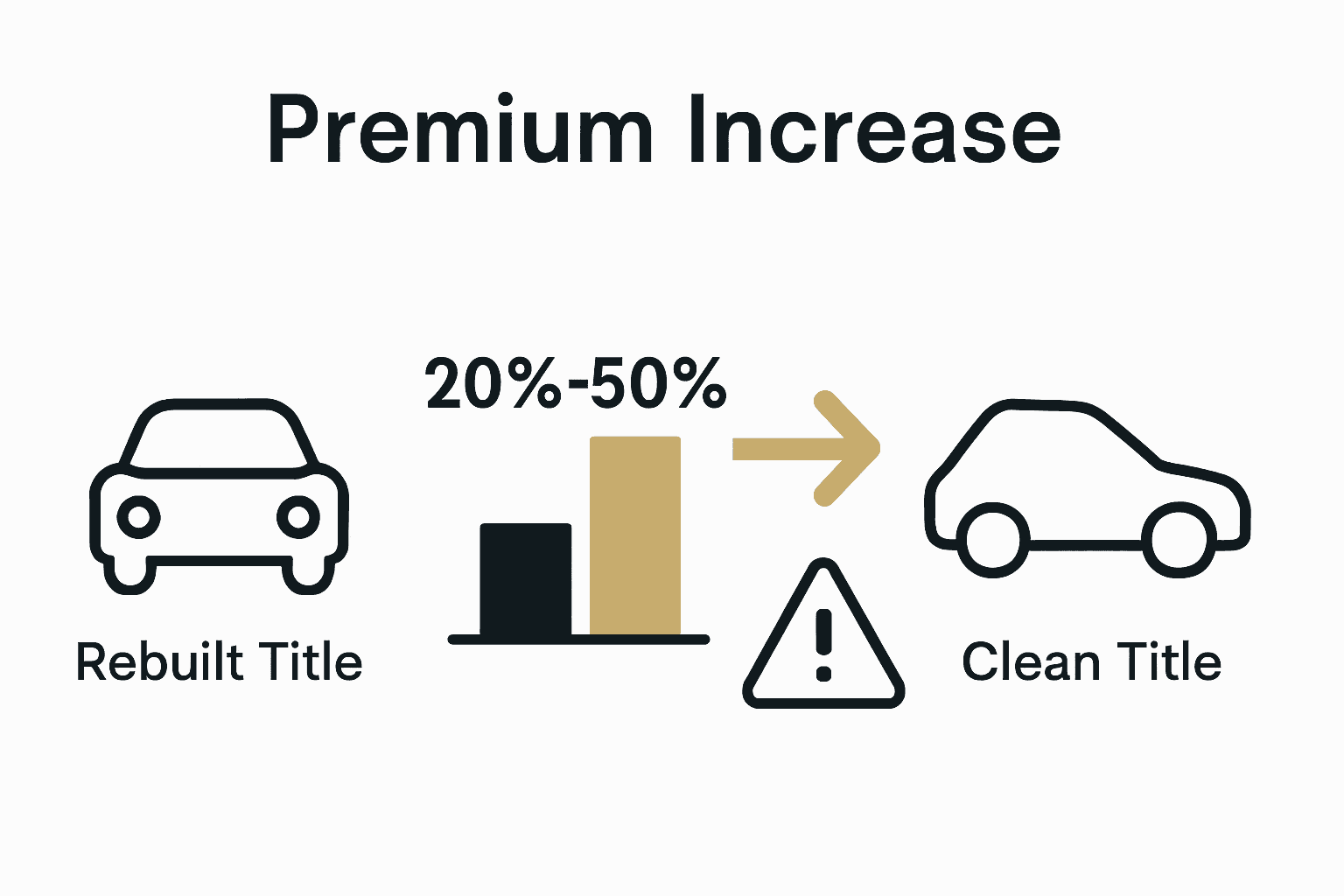

Typical Premium Increases Explained

Insuring a rebuilt title vehicle comes with unique financial considerations that can significantly impact your insurance costs. Premium increases for rebuilt title vehicles are not just a minor adjustment - they represent a substantial financial commitment that requires careful planning and understanding.

Typically, rebuilt title vehicles can expect premium increases ranging from 20% to 50% compared to similar clean title vehicles. These increases stem from several key risk factors that insurers carefully evaluate. The primary drivers of higher premiums include the vehicle’s uncertain repair history, potential structural weaknesses, and the increased likelihood of future mechanical issues.

Key factors influencing premium increases include:

- Repair Quality: Uncertainty about the thoroughness and professionalism of previous repairs

- Vehicle Age: Older rebuilt vehicles typically face more significant premium hikes

- Inspection History: Vehicles with comprehensive professional inspection records may see slightly lower increases

- Insurance Provider: Some companies specialize in rebuilt titles and offer more competitive rates

To mitigate these premium increases, consider these strategic approaches:

- Obtain a detailed, professional inspection report

- Choose insurance providers experienced with rebuilt titles

- Maintain meticulous vehicle maintenance records

- Consider higher deductibles to offset premium costs

For budget-conscious buyers, understanding these premium dynamics is crucial. While rebuilt titles offer significant cost savings on the initial purchase, insurance costs can quickly offset those initial savings if not carefully managed.

For a deeper dive into managing insurance costs for rebuilt titles, explore our comprehensive guide on insurance and rebuilt vehicles.

Documents Insurers Require

Navigating the insurance landscape for rebuilt title vehicles requires meticulous documentation. According to legalclarity.org, insurers are extremely detail-oriented when evaluating rebuilt title vehicles, requiring a comprehensive set of documents to assess the vehicle’s insurability.

Dmv.org emphasizes that the documentation process goes beyond simple paperwork - it’s about demonstrating the vehicle’s safety and roadworthiness. Insurance providers want concrete evidence that the vehicle has been properly restored and meets safety standards.

Essential documents you’ll need to prepare include:

- Rebuilt Title Certificate: The official legal document proving the vehicle’s status

- Comprehensive Repair Invoices: Detailed records of all repairs and parts replaced

- Professional Inspection Reports: Third-party assessments of the vehicle’s condition

- Photographic Evidence: Before and after photos of the vehicle’s restoration

- Vehicle Identification Number (VIN) History: Complete report showing previous damage and repairs

To maximize your chances of securing insurance, follow these preparation steps:

- Organize all repair documents chronologically

- Obtain a professional mechanical inspection

- Create a detailed folder with all vehicle history documentation

- Be prepared to provide additional information if requested

For budget-conscious buyers, thorough documentation isn’t just about insurance - it’s about protecting your investment and demonstrating the vehicle’s true value.

Want to dive deeper into preparing documentation for rebuilt title vehicles? Check out our comprehensive guide on insurance and rebuilt vehicles.

How To Shop And Save On Coverage

Shopping for insurance on a rebuilt title vehicle requires a strategic approach. According to autoinsurance.org, finding full coverage can be particularly challenging, with many insurers hesitant to provide comprehensive protection beyond basic liability insurance.

Navigating the insurance marketplace for rebuilt titles demands patience and thorough research. Insurers will scrutinize every detail of your vehicle’s history, making it crucial to be prepared with comprehensive documentation and a proactive approach to demonstrating your vehicle’s reliability.

Key strategies for saving on rebuilt title insurance include:

- Get Multiple Quotes: Compare at least 5-7 insurance providers

- Highlight Professional Repairs: Provide detailed documentation of high-quality restoration

- Consider Higher Deductibles: Offset premium costs by accepting more financial risk

- Bundle Insurance Policies: Negotiate discounts by combining auto insurance with other coverage

- Improve Vehicle Safety: Install additional anti-theft and safety devices

To maximize your insurance savings, follow these targeted approaches:

- Request specialized rebuilt title insurance quotes

- Obtain a professional, comprehensive vehicle inspection

- Maintain an immaculate driving record

- Take defensive driving courses

- Consider usage-based insurance programs

While insurance for rebuilt titles can be complex, a methodical approach can help you secure reasonable coverage. Budget-conscious buyers should view this as an opportunity to demonstrate their vehicle’s value and reliability.

For more insights on managing car buying costs, check out our guide to saving money when buying a car.

Resale Value And Claim Payout Impact

Rebuilt title vehicles come with unique financial considerations that dramatically impact their market value and insurance claims. According to autoinsurance.org, rebuilt title vehicles are inherently valued lower than clean-title counterparts, which creates significant challenges for owners when selling or filing insurance claims.

The reduced valuation isn’t just a minor inconvenience - it’s a substantial financial reality that can catch many buyers off guard. Insurers typically calculate payouts based on the vehicle’s diminished value, which means you’ll receive significantly less compensation in the event of an accident compared to a similar clean-title vehicle.

Key factors affecting resale value and claim payouts include:

- Perceived Reliability: Buyer skepticism about vehicle history

- Insurance Limitations: Reduced coverage options

- Market Perception: Automatic discount compared to clean-title vehicles

- Repair Quality: Direct impact on perceived value

- Documentation: Comprehensive repair records can mitigate value reduction

Strategies to maximize your rebuilt title’s value:

- Maintain meticulous repair and maintenance records

- Invest in professional, high-quality repairs

- Get regular professional inspections

- Provide detailed vehicle history documentation

- Be transparent about the vehicle’s reconstruction

While rebuilt titles come with financial challenges, informed buyers can still find significant value. Understanding these dynamics helps set realistic expectations about your vehicle’s worth and insurance potential.

Want to dive deeper into how rebuilt titles affect car value? Check out our comprehensive guide on rebuilt title car values.

Discover Smart Insurance Choices with ReVroom for Your Rebuilt Title Vehicle

Navigating insurance costs on a rebuilt title vehicle can feel like a maze full of questions about coverage limits, premiums, and documentation. This article highlights how higher premiums and limited insurance options often make buyers hesitate. ReVroom understands these challenges and offers a marketplace designed to bring clarity and confidence to your rebuilt car purchase.

With every listing on ReVroom, you get access to transparent vehicle history including accident information and pre-repair photos. This upfront transparency helps insurance providers better assess your vehicle, potentially smoothing the path toward coverage. It also empowers you to shop smarter, knowing exactly what you are buying and how to approach insurance providers with confidence.

Take control of your rebuilt title car journey now by exploring numerous vehicles vetted for safety and reliability at ReVroom. Go further with our unique platform that removes guesswork and lets your dollars stretch while ensuring you stay informed. Don’t wait to turn the page to your next reliable ride with confidence and transparency.

Frequently Asked Questions

How much higher are insurance premiums for rebuilt title vehicles compared to clean title vehicles?

Typically, premiums for rebuilt title vehicles can range from 20% to 50% higher than for similar clean title vehicles due to the vehicle’s uncertain repair history and potential risks.

What types of insurance coverage are available for rebuilt title vehicles?

Rebuilt title vehicles often only qualify for basic liability insurance. Limited comprehensive coverage and collision insurance may be hard to obtain and usually come with higher costs.

What documents are necessary to secure insurance for a rebuilt title vehicle?

Essential documents include a rebuilt title certificate, comprehensive repair invoices, professional inspection reports, photographic evidence of repairs, and a Vehicle Identification Number (VIN) history report.

How can I lower my insurance costs for a rebuilt title vehicle?

To lower insurance costs, consider obtaining multiple quotes, highlighting professional repairs, opting for higher deductibles, and maintaining a clean driving record. Additionally, bundling insurance policies can help you save money.