USAA rebuilt title insurance: what buyers need to know

May 4, 2026

TL;DR:

- Most rebuilt title cars can be insured with USAA after passing inspection and receiving a rebuilt title.

- Coverage options include liability, and possibly comprehensive and collision, but are case-dependent.

- Proper documentation and persistence are essential for securing insurance and acceptable premiums.

You’ve found a great rebuilt title car at a price that actually fits your budget, and now you’re wondering if USAA will cover it. Here’s the thing: most people assume rebuilt title vehicles are nearly impossible to insure, especially with a major carrier like USAA. That assumption has scared off plenty of perfectly good buyers from perfectly good cars. The reality is more nuanced, more navigable, and honestly more encouraging than the internet would have you believe. Let’s clear the air, walk through what USAA actually looks for, and give you a practical roadmap for getting covered.

One more prep tip before you call: insurers respond well to documentation, and so should you. A ReVroom History Report gives you the vehicle’s full history, how severe it was, and a fair-price check in one $15 document — useful for your own decision and handy backup when the underwriter asks what happened to the car.

Table of Contents

- Understanding rebuilt titles vs salvage titles

- Can you get USAA insurance on a rebuilt title car?

- What documentation and inspections does USAA require?

- Coverage types and limitations for rebuilt title cars

- What most buyers overlook about USAA and rebuilt title insurance

- Looking for affordable, reliable rebuilt title options and insurance help?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Rebuilt vs. salvage | Only rebuilt titles—never salvage—are eligible for insurance from USAA and other major insurers. |

| Documentation is critical | Proof of ownership, inspection reports, and rebuilt title paperwork are needed for USAA insurance approval. |

| Coverage varies | USAA may offer liability or broader coverage depending on inspection results, but it’s not guaranteed. |

| Direct contact matters | Call or email USAA with your full documentation for case-specific decisions and written confirmation. |

| Compare before you buy | Use checklists and expert guides to ensure your rebuilt title vehicle meets safety and insurance eligibility. |

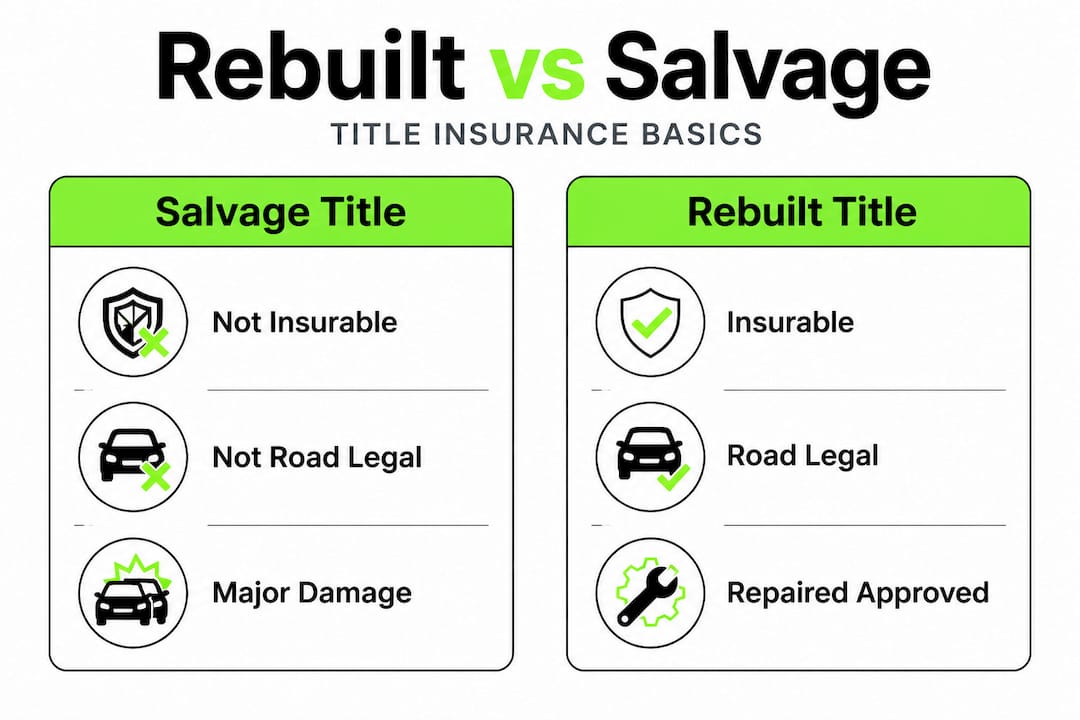

Understanding rebuilt titles vs salvage titles

To separate fact from myth, it’s essential to first understand what makes a vehicle’s history impact your ability to get insurance. These two titles get mixed up all the time, and that confusion costs buyers real money and real opportunities.

A vehicle receives a pre-rebuild designation when an insurance company declares it a total loss, meaning the estimated repair cost exceeded a certain percentage of the car’s market value. At that point, the car carries a title that marks it as not road-legal and not insurable for driving purposes. You simply cannot put plates on it, drive it legally, or get standard auto insurance on it in that state. As US News notes, you generally cannot insure a vehicle while it holds this pre-rebuild designation because it is not legally drivable.

A rebuilt title, on the other hand, is a completely different document. It is issued by a state DMV after a vehicle has been professionally repaired and passed a state-mandated safety inspection. Once a car receives a rebuilt title, it is legally road-worthy. It can be registered, licensed, plated, and yes, insured. Understanding the salvage to rebuilt process makes this journey a lot less mysterious.

Here is a quick side-by-side to make this crystal clear:

| Feature | Pre-rebuild designation | Rebuilt title |

|---|---|---|

| Road legal | No | Yes |

| Can be insured | Typically no | Yes, varies by insurer |

| State inspection required | Not yet | Yes, completed |

| Eligible for registration | No | Yes |

| Eligible for USAA coverage | No | Possibly yes |

The single most common mistake buyers make is assuming these two categories are interchangeable. They are not. Insurance companies, including USAA, make their decisions based on this distinction. If your car has already received its rebuilt title and passed inspection, you are starting from a completely different position than someone trying to insure a car that has not yet been through that process.

A few other missteps to watch out for:

- Assuming the title type alone guarantees or disqualifies coverage

- Forgetting to gather repair documentation before calling your insurer

- Expecting the same coverage limits and premiums as a clean title vehicle

Understanding the title distinction is your starting line. Everything else follows from there.

Can you get USAA insurance on a rebuilt title car?

Now that you know the paperwork difference, you can focus on how USAA and similar insurers actually treat rebuilt title cars. And here is where things get interesting.

USAA will not insure a vehicle while it holds a pre-rebuild designation. That part is firm. But USAA coverage for rebuilt title vehicles becomes available once the vehicle has been repaired, inspected, and officially received a rebuilt title. That is the threshold. Cross it with your paperwork in order, and the conversation changes.

What you will not find is a clean, publicly posted USAA underwriting policy for rebuilt titles. Searching for one turns up third-party Q&A content rather than an official rulebook. This is not a red flag; it simply means the decisions happen case by case, based on internal review of your vehicle’s documentation and condition. Expect variability. Expect questions. Expect the process to take some back and forth.

Here is what coverage typically looks like for rebuilt title vehicles with USAA:

- Liability coverage is the most common starting point. This covers damage you cause to others and is the easiest type to obtain for a rebuilt title vehicle.

- Comprehensive coverage (theft, weather, non-collision events) may be available depending on the vehicle’s condition and documentation provided.

- Collision coverage is possible but less consistent. It depends heavily on the inspection results and what the underwriter decides.

- Full coverage combining liability, comprehensive, and collision is the hardest to lock in and is never guaranteed.

For more detail on USAA rebuilt title rules and how they compare to other insurers, you will want to dig into the specifics before you call. And speaking of calling, that is exactly what you should do. Contact USAA directly with your VIN and full documentation ready before assuming anything.

Pro Tip: Do not just ask “Can you insure my rebuilt title car?” Ask specifically what types of coverage are available for your vehicle’s VIN, your state, and your documentation. The more specific your question, the more useful the answer.

There is also a broader picture worth seeing here. USAA is just one option. You can explore all of your rebuilt title insurance options to compare how different providers approach this. Some are more flexible than USAA. Some are less. Shopping around is always smart.

What documentation and inspections does USAA require?

Understanding USAA’s general stance helps, but the right paperwork is genuinely make-or-break when seeking coverage. This is where a lot of buyers drop the ball, not because they lack the right car, but because they show up to the conversation unprepared.

Multiple sources confirm that you may need to provide documentation and a vehicle inspection to insure a rebuilt title vehicle with USAA. Here is what you should have ready before you pick up the phone:

- Proof of ownership: Your name on the title, clear and current.

- Vehicle registration: Current registration in your state.

- Rebuilt title certificate: The actual title document issued after inspection, not any prior version.

- Repair documentation: Records from a licensed mechanic or body shop showing what work was performed.

- State inspection certificate: The official result of your state’s safety inspection that triggered the rebuilt title issuance.

- Photos of completed repairs: Before-and-after documentation of the vehicle’s condition.

USAA may also require an independent inspection of their own before granting broader coverage like collision or comprehensive. This is not unusual and not a reason to panic. It is their way of verifying the vehicle is in the condition you say it is.

Understanding the rebuilt title retitling process in your state is important here because requirements vary. What satisfies an inspector in Texas may differ from what is required in Ohio. Make sure the documentation you have is state-specific and complete.

A few common bureaucratic stumbling blocks buyers run into:

- Missing repair receipts because they assumed verbal confirmation was enough

- Submitting an outdated title version instead of the rebuilt title certificate

- Not having the inspection certificate separate from the title document itself

- Providing incomplete repair records that skip certain work that was done

Pro Tip: Scan every document related to your vehicle’s repair history and save it in a dedicated folder, both on your device and in the cloud. Name each file clearly (for example: “rebuilt-title-certificate-2023-honda-civic.pdf”). When USAA or any insurer asks for documentation, you can send it immediately without scrambling. Speed and organization signal that you are a prepared, low-risk client.

Want a structured way to approach this? The inspection checklist for rebuilt cars and the rebuilt title buyer checklist at ReVroom are built exactly for this kind of preparation.

Coverage types and limitations for rebuilt title cars

Once your paperwork is organized and you are ready to submit, it is important to know what kind of protection you can realistically expect. Let us be straight with you here, because honest expectations are more useful than wishful thinking.

As confirmed by WalletHub’s analysis, coverage for rebuilt title vehicles with USAA only becomes available after the car has been fully repaired, inspected, and issued a rebuilt title. From there, here is what the coverage landscape typically looks like:

- Liability only: The most consistently available option. Covers third-party property damage and bodily injury you cause in an accident.

- Comprehensive: Available in many cases but not guaranteed. Covers non-collision events like hail, theft, or fire.

- Collision: Possible but often the hardest to unlock. Covers your vehicle in a collision regardless of fault.

- Full coverage: The full package is available in some cases but depends heavily on the vehicle, repair quality, and underwriter discretion.

There are also real limitations to keep in mind:

“Rebuilt title cars may face higher premiums, coverage exclusions related to prior vehicle history, or outright denial of certain coverage types depending on the insurer’s internal review process.”

That is not a reason to walk away. It is a reason to go in with eyes open. Premiums on rebuilt title vehicles can run higher than on comparable clean title cars because insurers factor in the vehicle’s history and a potentially lower resale value. You are still likely paying far less overall when you consider that rebuilt title cars are often priced up to 50% below their clean title equivalents.

It is also worth noting that payout amounts in a total loss scenario may reflect the rebuilt title market value, which is lower than a clean title equivalent. This is something worth discussing with your insurer before you commit, not after. Learn more about the full picture of rebuilt car insurance details so you can budget accordingly.

What most buyers overlook about USAA and rebuilt title insurance

Here is the honest, been-around-the-block take: most buyers underestimate just how variable insurer rules are for rebuilt title vehicles. They search online, find a few articles, and assume the experience will follow a predictable script. It often does not.

There is no published USAA underwriting rulebook for rebuilt titles. That means the front-line representative you speak with may not have crystal-clear guidance either. We have seen buyers call three times and get three different answers. That is not a knock on USAA specifically; it reflects the reality that rebuilt title underwriting is handled case by case, with a lot of discretion left to individual reviewers.

What this means practically: your persistence and your records matter as much as the car itself. A buyer with a spotless documentation folder who follows up consistently will move through this process faster and with better results than someone who calls once, gets discouraged, and gives up. The car did not change. The outcome did.

Here is the other thing most buyers miss: a rebuilt title is not a magic key that unlocks any specific coverage level. The quality of the repairs, your state’s inspection standards, the vehicle’s make and model, and the specific underwriter reviewing your file all factor in. Two people with the same car in the same state can get different answers. That is just the reality of navigating real-world insurance challenges for rebuilt vehicles.

The takeaway? Never assume eligibility. Never assume denial either. Get confirmation in writing, or at the very minimum document the date, time, and name of the representative you spoke with. Treat this like the financial decision it is, because it is.

Looking for affordable, reliable rebuilt title options and insurance help?

If you are ready to apply these tips and shop with confidence, ReVroom was built for exactly this moment.

ReVroom is the only online marketplace built specifically for affordable rebuilt vehicles, and the platform is designed to give you the transparency you need before you ever call an insurance company. Every listing includes vehicle history information and pre-repair photos so you can see exactly what you are getting. That kind of upfront documentation is also exactly what insurers like USAA want to see. And for a car listed anywhere else, a $15 ReVroom History Report gives you the same upfront clarity before you commit. Ready to find a vehicle you can feel great about and insure with confidence? The ReVroom platform is the place to start. Better car. Smarter buy. Go further.

Frequently asked questions

Can I get full coverage from USAA on a rebuilt title car?

USAA may offer comprehensive or collision coverage on rebuilt title cars, but it is not guaranteed and depends on their internal inspection and underwriting review.

What paperwork do I need for USAA rebuilt title insurance?

You will need proof of ownership, current registration, a rebuilt title certificate, and typically repair and inspection documentation from a licensed mechanic or body shop.

Why can’t I insure a pre-rebuild vehicle with USAA?

Cars that have not yet been repaired and retitled are not legal to drive and are generally uninsurable until the repair and inspection process is complete and a rebuilt title is issued.

Are premiums higher for rebuilt title cars?

Premiums for rebuilt title cars can be higher than comparable clean title vehicles because insurers account for the vehicle’s history and a lower estimated market value.

Does USAA publish a public underwriting policy for rebuilt titles?

No. There is no official underwriting guide from USAA for rebuilt title vehicles, and most information circulating online comes from third-party sources rather than USAA directly.

Recommended

- Rebuilt Title Documentation: What Buyers Need to Know | ReVroom

- Rebuilt Title Insurance Explained – What Utah Buyers Need | ReVroom

- Rebuilt title myths: what budget-savvy buyers need to know

- Does USAA insure rebuilt titles in 2026? Guide for buyers | ReVroom

- Tailor Your Auto Warranty: Steps to Custom Coverage