What does a prior salvage title mean? guide 2026

March 14, 2026

You’ve probably heard horror stories about cars with salvage titles, but here’s the surprise: these vehicles can save you 20-60% compared to clean title cars. The catch? Understanding what “prior salvage title” actually means is crucial before you hand over your hard-earned cash. This guide cuts through the confusion, explaining exactly what happens when a car gets branded with a salvage title, how it differs from a rebuilt title, and what you need to know to make a smart, safe purchase decision in 2026.

Table of Contents

- What Is A Prior Salvage Title And How Does It Happen?

- Understanding Rebuilt Titles: Repairing And Retitling Salvage Vehicles

- Benefits And Risks Of Buying Vehicles With Prior Salvage Or Rebuilt Titles

- How To Safely Buy And Finance A Rebuilt Title Vehicle In 2026

- Explore Rebuilt Title Vehicles And Expert Guidance At Revroom

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Salvage means total loss | A salvage title is issued when repair costs exceed 70-90% of the vehicle’s actual cash value, making it uninsurable and illegal to drive. |

| Rebuilt means repaired and inspected | A rebuilt title indicates a car was previously totaled but has been repaired and inspected to be roadworthy, allowing legal road use. |

| Significant savings available | Vehicles with salvage titles are often sold at 20%-50% lower prices, offering budget-conscious buyers substantial value. |

| Insurance costs increase | Insurance premiums for rebuilt title vehicles can be 20-40% higher and coverage options may be limited. |

| Inspection quality varies widely | State regulations and repair standards differ dramatically, making professional pre-purchase inspections essential for safety. |

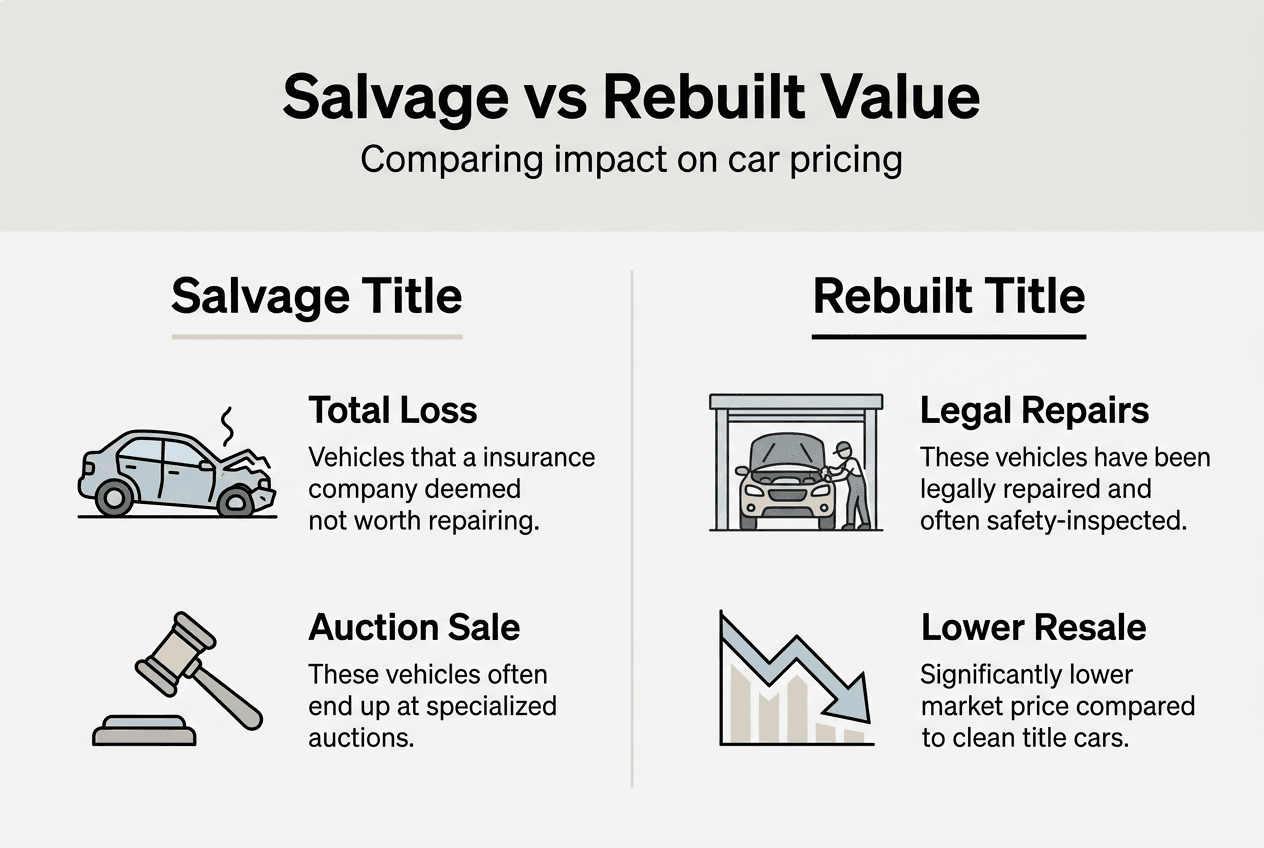

What is a prior salvage title and how does it happen?

A salvage title is a legal brand stamped on a vehicle’s record when an insurance company declares it a total loss. This doesn’t necessarily mean the car is destroyed beyond recognition. A salvage title is issued when an insurance company declares a vehicle a total loss, typically when repair costs exceed 70-90% of the vehicle’s actual cash value. The threshold varies by state, but the principle remains the same: fixing the car costs more than it’s worth in the insurer’s eyes.

Once branded with a salvage title, a vehicle cannot be legally driven on public roads or insured for regular use. It exists in automotive limbo, waiting for someone to either part it out or invest in repairs. This is where the path splits: some vehicles stay salvage forever, while others get a second chance through the rebuilding process.

Common events that trigger salvage titles include:

- Severe collision damage requiring extensive structural repairs

- Flood damage affecting electrical systems and mechanical components

- Theft recovery where the vehicle was stripped or damaged

- Hail damage causing widespread body panel replacement

- Fire damage compromising safety systems

Here’s what most people don’t realize: damage leading to salvage titles ranges from catastrophic crashes to relatively minor incidents that simply cost too much to fix given the car’s low market value. An older vehicle might get salvaged after a fender bender that would be easily repaired on a newer model.

The salvage title designation protects consumers by creating a permanent record of significant vehicle history, but it also creates opportunities for budget-conscious buyers willing to do their homework.

After receiving a salvage title, these vehicles typically end up at insurance auctions where repair shops, dealers, and individual buyers bid on them. The salvage title meaning is straightforward: this car has a documented history that requires disclosure, and it needs work before returning to the road. Understanding this foundation helps you evaluate whether a rebuilt vehicle is right for your needs and budget.

Understanding rebuilt titles: repairing and retitling salvage vehicles

The journey from salvage to rebuilt title represents a vehicle’s redemption arc. A rebuilt title indicates a car was previously totaled but has been repaired and inspected to be roadworthy, transforming it from an undrivable insurance write-off to a legal, functional vehicle. This transformation isn’t automatic or simple. It requires repairs, documentation, and official approval.

The typical process for obtaining a rebuilt title follows these steps:

- Purchase the salvage vehicle at auction or from an insurance company

- Complete all necessary repairs using quality parts and skilled labor

- Gather detailed receipts, photos, and documentation of all repair work

- Schedule and pass a state-mandated inspection verifying roadworthiness

- Submit application and documentation to your state’s motor vehicle department

- Receive the rebuilt title once approved

State requirements vary dramatically in their rigor and thoroughness. Some states conduct detailed inspections examining frame integrity, safety systems, and proper part installation. Others perform cursory checks that barely scratch the surface. This inconsistency creates a wide quality spectrum in the rebuilt title market, which is why understanding rebuilt cars retitling process matters for your safety and investment.

Pro Tip: Before buying any rebuilt title vehicle, request copies of the repair receipts and inspection documents. Quality rebuilders keep meticulous records and are proud to share them. If a seller hesitates or can’t produce documentation, that’s your signal to walk away.

Once a vehicle receives a rebuilt title, that brand stays with it forever. Unlike credit scores that improve over time, a rebuilt title never graduates back to clean status. This permanent designation affects insurance rates, resale value, and financing options throughout the vehicle’s remaining life. However, it also enables significant savings for informed buyers who understand the rebuilt vs salvage titles guide and know how to evaluate repair quality.

The rebuilt title definition and process emphasizes that these vehicles have met minimum legal standards for safety and operation. That’s the floor, not the ceiling. Smart buyers look beyond the title brand to examine actual repair quality, parts used, and the expertise of whoever did the work. A rebuilt title opens the door, but thorough due diligence determines whether you should walk through it.

Benefits and risks of buying vehicles with prior salvage or rebuilt titles

Let’s cut straight to what matters: money, safety, and long-term value. Buying a vehicle with history involves real tradeoffs that deserve honest evaluation.

| Factor | Clean Title | Salvage Title | Rebuilt Title |

|---|---|---|---|

| Purchase Price | Full market value | 50-80% discount | 20-50% discount |

| Insurance | Standard rates, full coverage | Cannot be insured | Higher premiums, limited coverage |

| Legal to Drive | Yes | No | Yes |

| Resale Value | Highest | Cannot be sold for road use | Significantly reduced |

| Financing | Easy approval | Not available | Difficult, higher rates |

The benefits that attract budget-conscious buyers include:

- Substantial cost savings that can put a newer vehicle within reach

- Access to makes and models otherwise outside your budget range

- Legal operation with proper rebuilt title and registration

- Opportunity to own a quality vehicle if repairs were done correctly

Vehicles with salvage titles are often sold at 20%-50% lower prices, offering potential savings for budget-conscious buyers. That discount translates to thousands of dollars staying in your pocket, money you could use for maintenance, upgrades, or simply building your savings. For many buyers, this makes the difference between owning a car or relying on unreliable transportation.

The risks you need to weigh carefully include:

- Hidden structural or mechanical issues that weren’t fully repaired

- Varying repair quality depending on who did the work and parts used

- Higher insurance costs and potential coverage limitations

- Reduced resale value when you eventually sell

- Difficulty obtaining financing from traditional lenders

Insurance premiums for rebuilt title vehicles can be 20-40% higher and may be harder to obtain. Some insurers refuse to offer comprehensive or collision coverage on rebuilt vehicles, limiting you to liability-only policies. This matters if you’re financing the purchase or want protection against theft or further damage.

Pro Tip: Before committing to any rebuilt title purchase, get insurance quotes from at least three carriers. Some specialize in rebuilt vehicles and offer competitive rates, while others won’t touch them. Knowing your insurance costs upfront prevents unpleasant surprises after purchase.

The salvage title vehicle value equation balances immediate savings against potential long-term costs. A well-repaired vehicle from a quality rebuilder can serve you reliably for years. A poorly repaired one becomes a money pit that erodes your initial savings through constant repairs. Understanding salvage title car insurance requirements and shopping carefully helps you make an informed decision.

The resale value of salvage title cars remains permanently affected, typically reducing what you can sell for by 20-40% compared to equivalent clean title vehicles. This isn’t necessarily a dealbreaker if you plan to drive the car for many years, but it matters for your long-term financial planning.

How to safely buy and finance a rebuilt title vehicle in 2026

Knowing the risks is step one. Managing them effectively is what separates smart buyers from those who learn expensive lessons.

Follow these steps when purchasing a rebuilt title vehicle:

- Obtain the complete vehicle history report including the original damage description and photos

- Hire a qualified mechanic to perform a thorough pre-purchase inspection focusing on frame integrity and safety systems

- Review all repair documentation, receipts, and photos from the rebuilding process

- Get insurance quotes from multiple carriers before committing to purchase

- Research your state’s specific rebuilt title regulations and disclosure requirements

- Compare financing options and prepare for higher down payments or interest rates

Additional tips for protecting yourself include:

- Verify the vehicle’s title status directly with your state’s motor vehicle department

- Budget an extra 20-40% for insurance compared to clean title equivalents

- Ask about any available warranties or guarantees from the seller

- Test drive the vehicle extensively in various conditions

- Have a trusted mechanic inspect the vehicle before finalizing purchase

Pro Tip: Negotiate the purchase price by factoring in the vehicle’s limited resale value and your higher insurance costs. A fair price accounts for these ongoing expenses, not just the initial discount. Use specific numbers from your insurance quotes and comparable vehicle listings to support your offer.

Financing rebuilt title cars often involves higher interest rates, larger down payments, and shorter loan terms. Traditional banks and credit unions frequently decline rebuilt title financing, pushing buyers toward specialized lenders or requiring cash purchases. If you need financing, start that conversation early. Some lenders specialize in rebuilt vehicles and understand how to evaluate them properly.

Insurance premiums for rebuilt title cars are typically 20-40% higher and many insurers only offer liability coverage. Shop aggressively for coverage, as rates vary widely between carriers. Some companies that insure rebuilt vehicles competitively include regional carriers and those specializing in non-standard auto insurance. Don’t assume your current insurer offers the best rebuilt vehicle rates.

Understanding financing a rebuilt car requirements helps you prepare financially. Expect to provide detailed vehicle documentation, possibly including the repair receipts and inspection reports. Lenders want assurance that the vehicle is truly roadworthy and worth their investment.

When you’re ready to move on, selling a rebuilt salvage title car requires transparency and realistic pricing. Full disclosure builds trust with potential buyers and protects you legally. The salvage title insurance and safety considerations you evaluated when buying become selling points when you market the vehicle honestly and thoroughly.

Explore rebuilt title vehicles and expert guidance at ReVroom

Now that you understand the landscape, finding the right rebuilt title vehicle becomes your next challenge. That’s where specialized marketplaces make all the difference.

ReVroom eliminates the guesswork by providing accident history information and photos of what each car looked like before repairs in every listing. No more paying $150 per vehicle for investigation reports or wondering what you’re really buying. You see exactly what happened and how it was fixed, giving you the transparency needed to make confident decisions. Whether you’re hunting for your first rebuilt title vehicle or you’re a seasoned buyer, having all the critical information upfront saves time, money, and stress. Visit the ReVroom homepage to explore current listings and discover how rebuilt title vehicles can stretch your automotive budget further than you thought possible.

Pro Tip: Use professional marketplaces that specialize in rebuilt vehicles rather than general classified sites. Specialized platforms understand the unique disclosure requirements and provide the detailed history information you need to evaluate vehicles safely and effectively.

The salvage vs rebuilt titles guide available through ReVroom helps you navigate the complexities with expert insights tailored to budget-conscious buyers. When you’re ready to take the next step, having access to comprehensive vehicle histories and repair documentation transforms rebuilt title shopping from risky gamble to informed investment.

Frequently asked questions

What does a salvage title mean in simple terms?

A salvage title is a legal designation indicating an insurance company declared the vehicle a total loss because repair costs exceeded a percentage of its value, typically 70-90%. The vehicle cannot be driven legally or insured until it’s repaired, inspected, and retitled as rebuilt. This permanent record protects future buyers by disclosing significant vehicle history.

Can a rebuilt title vehicle be insured and financed?

Yes, rebuilt title vehicles can be insured and financed, though with limitations. Insurance premiums for rebuilt title vehicles can be 20-40% higher and some insurers may refuse coverage. Many carriers offer only liability coverage rather than comprehensive protection. Financing typically requires larger down payments and higher interest rates through specialized lenders. Shopping multiple liability insurance for salvage cars providers helps you find competitive rates and adequate coverage for your needs.

How does a salvage or rebuilt title affect resale value?

Rebuilt title vehicles typically sell for 20-40% less than comparable clean title vehicles, and this discount persists throughout the vehicle’s life. The permanent title brand affects buyer confidence and limits your potential market when selling. However, if you purchase at an appropriate discount initially and drive the vehicle for many years, the reduced resale value becomes less significant to your overall cost of ownership.

Are all rebuilt title cars risky to buy?

No, risk varies dramatically based on repair quality, original damage severity, and how thoroughly you evaluate the vehicle before purchase. Poorly executed repairs on rebuilt vehicles can lead to mechanical failures and safety issues, but professional rebuilds using quality parts and skilled labor can result in reliable, safe vehicles. The key is thorough inspection, complete documentation review, and buying from reputable sellers who provide transparency about the vehicle’s history and repairs.

What should buyers check before purchasing a rebuilt title vehicle?

Obtain the complete vehicle history including original damage photos and description, then hire a qualified mechanic to inspect frame integrity, safety systems, and repair quality. Review all repair receipts and documentation to verify proper parts and professional work. Get insurance quotes before committing to ensure coverage availability and cost. Test drive extensively and verify the title status directly with your state’s motor vehicle department. This due diligence protects you from hidden issues and ensures you’re making an informed investment.

How much can I save buying a car with a prior salvage title?

Rebuilt title cars can offer savings of 20-60% compared to clean title vehicles, depending on the make, model, and extent of previous damage. These savings typically translate to several thousand dollars on most vehicles, making newer or higher-end models accessible to budget-conscious buyers. However, factor in higher insurance costs and reduced resale value when calculating your true savings. The best deals come from well-repaired vehicles purchased at fair prices that account for the title brand’s ongoing impact.