Liability insurance for salvage title cars: what you need to know in 2026

March 13, 2026

You’ve heard that cars with certain titles are nearly impossible to insure, and maybe you’ve avoided them entirely because of it. Here’s the truth: while insurance for these vehicles is more complex than for clean title cars, it’s far from impossible. If you’re a budget-conscious buyer considering a rebuilt title vehicle, understanding liability insurance options is critical. This guide cuts through the confusion, explains exactly what coverage you can expect, and shows you how to navigate the insurance landscape for vehicles with history. You’ll learn the key differences between title types, why insurers charge more, and practical steps to secure affordable coverage that protects you on the road.

Table of Contents

- Understanding Salvage And Rebuilt Titles: What They Mean For Insurance

- Why Is Liability Insurance For Salvage Title Vehicles Harder To Get And More Expensive?

- How Liability Insurance Coverage Works For Rebuilt Title Vehicles

- Finding And Securing Liability Insurance For Rebuilt Title Cars: Practical Tips

- Get Started With Reliable Rebuilt Title Insurance Today

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Title type determines coverage | Cars with certain title designations typically cannot get full coverage until repaired and retitled, but liability insurance is usually available. |

| Expect higher premiums | Liability insurance for these vehicles often costs 10 to 30 percent more than clean title equivalents due to perceived risk. |

| Vehicle value impacts insurance | These cars are worth 20 to 40 percent less than comparable clean title vehicles, affecting insurance payouts and resale options. |

| State and insurer variations | Coverage availability and rates differ significantly by state regulations and individual insurance company policies. |

| Specialty insurers help | Non-standard and high-risk insurers often provide options when major carriers decline coverage for these vehicles. |

Understanding salvage and rebuilt titles: what they mean for insurance

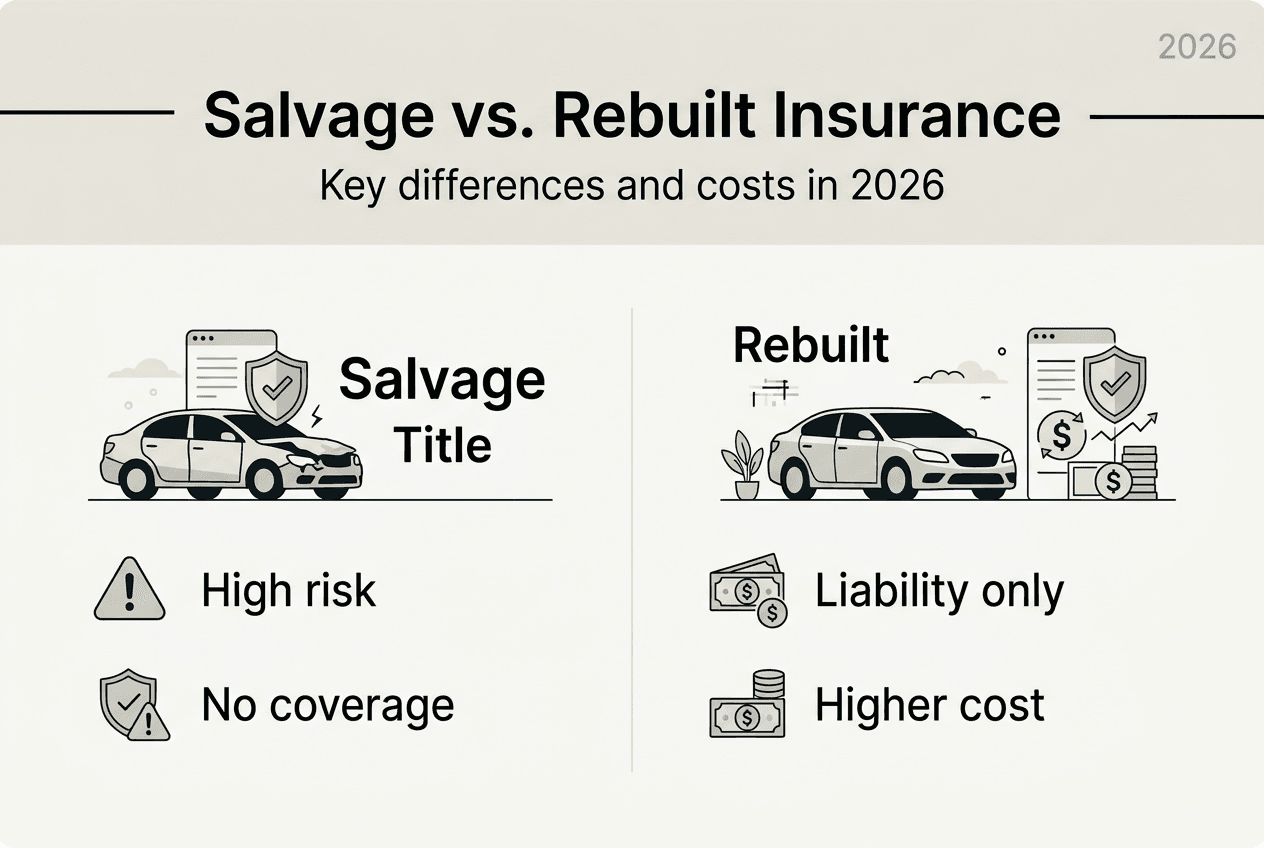

Before you can navigate insurance options, you need to understand exactly what you’re dealing with. A salvage title is assigned to a vehicle that an insurance company has declared a total loss, usually because repair costs exceed a certain percentage of the car’s value. These vehicles are typically undrivable and cannot legally be operated on public roads. You cannot insure a salvage title car for on-road use, period. Insurance companies simply won’t write policies for vehicles in this condition.

A rebuilt title, however, tells a different story. This designation means a vehicle that once had a salvage title has been repaired, inspected by state authorities, and deemed roadworthy. The difference between salvage and rebuilt title status is critical because it determines your insurance eligibility. According to Trusted Choice, car insurance companies won’t write a policy for a salvage title car unless it gets rebuilt and then officially inspected. Once a vehicle passes state inspection and receives a rebuilt title, liability insurance becomes available, though often with limitations.

State inspection requirements vary widely and directly impact insurance eligibility. Some states have rigorous multi-point inspections that verify structural integrity, safety systems, and proper repairs. Others have more lenient processes. The inspection documentation you receive becomes crucial when shopping for insurance, as it demonstrates the vehicle meets minimum safety standards. Insurers want proof that the car is roadworthy before they’ll consider coverage.

Here’s what you need to know about title types and insurance:

- Salvage title vehicles cannot be insured for road use and must remain off public roads

- Rebuilt title vehicles can typically secure liability insurance after passing state inspection

- Comprehensive and collision coverage remain difficult or impossible to obtain even with rebuilt titles

- State inspection certificates serve as essential documentation when applying for insurance

- The quality and thoroughness of repairs directly influence insurer willingness to provide coverage

Understanding these distinctions helps you set realistic expectations. If you’re considering a vehicle with history, make sure it has already been retitled as rebuilt. Buying a salvage title car with plans to repair and insure it later adds complexity, cost, and uncertainty to your purchase.

Why is liability insurance for salvage title vehicles harder to get and more expensive?

Insurers operate on risk assessment, and vehicles with history present unique challenges that translate directly into higher premiums and limited coverage options. The core issue is uncertainty. When an insurance company evaluates a rebuilt title vehicle, they’re looking at a car that was once damaged severely enough to be declared a total loss. Even after repairs and inspection, questions remain about the quality of those repairs, hidden damage, and future reliability.

According to Trusted Choice, insurance companies are hesitant to insure salvage title cars due to the high risk of pre-existing damage and potential for future claims. This hesitation doesn’t disappear just because the vehicle now has a rebuilt title. Insurers worry about fraud, where sellers might conceal serious structural issues or use substandard parts. They also struggle with valuation, since rebuilt title vehicles don’t follow standard depreciation curves and market values vary wildly based on repair quality and buyer perception.

Research from WalletHub confirms that liability insurance for rebuilt title vehicles is often more expensive and harder to obtain than for vehicles with clean titles. Premiums typically run 10 to 30 percent higher than comparable clean title cars. Some major insurance carriers refuse to cover rebuilt titles entirely, forcing buyers toward specialty or high-risk insurers who charge premium rates.

The Alibaba Car Interior Q&A explains that insurers view salvage title cars as higher risk due to valuation difficulty, fraud potential, safety concerns, and uncertain repair quality. These factors compound when insurers consider comprehensive and collision coverage, which would require them to pay out claims on a vehicle with unknown repair history and questionable resale value. Most insurers simply won’t take that risk.

Here’s why insurers charge more and limit coverage:

- Pre-existing damage concerns make future claims difficult to assess and attribute

- Valuation challenges create uncertainty about appropriate claim payouts

- Fraud potential increases when vehicle history is complex or poorly documented

- Safety concerns persist even after state inspection, especially regarding structural integrity

- Repair quality varies dramatically depending on who did the work and what parts were used

- Resale value uncertainty makes total loss calculations unpredictable

Pro Tip: When shopping for insurance coverage for rebuilt titles, focus first on liability coverage and accept that comprehensive and collision may not be available. This approach keeps you legal on the road while managing costs.

Understanding insurer perspective helps you negotiate better. If you have detailed repair documentation, quality parts receipts, and professional inspection reports, you can sometimes secure better rates by demonstrating the vehicle’s condition and repair quality.

How liability insurance coverage works for rebuilt title vehicles

Liability insurance is the most accessible coverage type for rebuilt title vehicles, but it comes with important limitations and considerations you need to understand before purchase. Liability coverage protects other people and their property if you cause an accident. It doesn’t cover damage to your own vehicle. For many budget-conscious buyers, liability-only coverage represents the most practical and affordable option for rebuilt title cars.

According to US News, insurers typically offer limited coverage, often only liability, for rebuilt title cars. This means you can legally drive the vehicle and protect yourself from financial liability if you cause an accident, but you won’t receive insurance money to repair your own car if it’s damaged. For a vehicle you purchased at a significant discount, this trade-off often makes financial sense.

Comprehensive and collision coverage remain elusive for most rebuilt title owners. Some insurers may allow these coverages after thorough inspection, but many refuse entirely. The Alibaba Car Interior Q&A notes that some insurers may allow comprehensive and collision coverage for rebuilt titles after inspection, but this is the exception rather than the rule. When available, premiums for these coverages are substantially higher than for clean title vehicles.

The financial impact of a rebuilt title extends beyond insurance premiums. Trusted Choice reports that the value of a car with a salvage title is typically 20 to 40 percent less than an equivalent, non-salvaged car. This reduced value affects insurance payouts if you do secure comprehensive or collision coverage. It also impacts resale options, as fewer buyers want vehicles with history and those who do expect significant discounts.

Here’s a breakdown of typical coverage and cost implications:

| Coverage Type | Availability | Cost Impact | Key Limitations |

|---|---|---|---|

| Liability | Widely available | 10-30% higher premiums | No coverage for your vehicle damage |

| Comprehensive | Rarely available | 30-50% higher if offered | Limited payouts based on reduced value |

| Collision | Rarely available | 30-50% higher if offered | May require independent appraisal |

| Uninsured Motorist | Usually available | 10-20% higher premiums | Standard coverage terms typically apply |

State inspection quality directly influences coverage options. Vehicles that pass rigorous inspections in states with strict standards often qualify for better coverage terms. Some insurers require independent mechanical inspections beyond state requirements before they’ll consider comprehensive or collision coverage.

Key considerations for rebuilt title insurance:

- Liability coverage protects others but leaves you financially exposed for your own vehicle repairs

- Comprehensive and collision coverage, when available, pay out based on reduced rebuilt title market value

- Insurance payouts may be 20 to 40 percent less than you paid if you overpaid at purchase

- Resale challenges compound insurance limitations, as future buyers face the same coverage restrictions

- State inspection documentation significantly impacts insurer willingness to provide coverage

Pro Tip: Calculate the total cost of ownership including higher insurance cost on rebuilt titles before purchase. If you’re paying $8,000 for a rebuilt title car that would cost $15,000 with a clean title, factor in the extra $300 to $500 annually for insurance over your expected ownership period.

Understanding coverage limitations helps you make informed decisions. For many buyers, the significant purchase price savings offset the insurance challenges and coverage restrictions. The key is knowing exactly what you’re getting into before you commit.

Finding and securing liability insurance for rebuilt title cars: practical tips

Securing insurance for a rebuilt title vehicle requires a more strategic approach than shopping for clean title coverage. You’ll face more rejections, need more documentation, and probably pay higher premiums. But with the right strategy, you can find affordable liability coverage that keeps you legal and protected on the road.

Start your search with an independent insurance agent who understands rebuilt title vehicles. According to Trusted Choice, an independent insurance agent can make finding rebuilt title insurance easy. These agents work with multiple carriers and know which companies are more flexible with rebuilt titles. They can save you hours of phone calls and online quotes that lead nowhere.

Follow these steps to secure the best coverage:

- Gather complete documentation before you start shopping, including the rebuilt title certificate, state inspection report, repair receipts, and photos of the completed repairs

- Contact independent insurance agents first, as they have access to multiple carriers and specialty insurers

- Request quotes from at least five different insurers to compare rates, coverage limits, and policy exclusions

- Be completely transparent about the vehicle’s history, providing all documentation upfront to avoid claims denial later

- Ask specifically about coverage limitations, exclusions, and whether comprehensive or collision coverage might be available

- Compare not just premiums but also liability limits, deductibles, and customer service ratings

- Review policy documents carefully for rebuilt title exclusions or special conditions before signing

Specialty and high-risk insurers often provide options when standard carriers decline. The Alibaba Car Interior Q&A confirms that specialty and high-risk insurers often cover vehicles that standard insurers decline. These companies specialize in non-standard situations and understand rebuilt title vehicles better than major carriers. While premiums may be higher, they offer coverage when others won’t.

Expect to pay 10 to 30 percent more for liability insurance compared to a clean title equivalent. This premium reflects the insurer’s perceived risk and the challenges of valuing and assessing rebuilt title vehicles. If quotes come in significantly higher than this range, shop around more aggressively or consider whether the vehicle’s purchase price savings justify the insurance costs.

Key strategies for success:

- Prioritize insurers and agents with specific rebuilt title experience and positive reviews

- Provide comprehensive documentation proactively to demonstrate transparency and vehicle quality

- Compare total annual costs including premiums, deductibles, and coverage limits across multiple quotes

- Consider state farm, progressive, and geico first, as they sometimes cover rebuilt titles in certain states

- Explore regional and specialty insurers if major carriers decline coverage

- Ask about discounts for safety features, low mileage, or bundling with other insurance policies

Pro Tip: Get quotes before you purchase the vehicle. Knowing your insurance costs upfront helps you calculate true ownership costs and negotiate a better purchase price. Use resources like insurance on salvage title step-by-step guides to prepare your documentation and approach.

Transparency is non-negotiable. Never hide or minimize the vehicle’s history when applying for insurance. Insurers will discover the rebuilt title during underwriting, and any misrepresentation can void your policy or lead to claims denial when you need coverage most. Honest disclosure from the start builds trust and ensures your coverage is valid when you need it.

Get started with reliable rebuilt title insurance today

Navigating insurance for rebuilt title vehicles doesn’t have to be overwhelming when you have the right support and resources. ReVroom specializes in helping budget-conscious buyers understand and overcome the unique challenges of vehicle history, including insurance considerations. Our platform provides the transparency you need to make informed decisions, with detailed history information and repair photos for every listing. This documentation becomes invaluable when shopping for insurance, as it demonstrates vehicle condition and repair quality to insurers.

Whether you’re researching your first rebuilt title purchase or comparing insurance options for a vehicle you already own, ReVroom offers expert guidance tailored to your situation. Our resources help you understand insurer requirements, prepare necessary documentation, and find coverage that fits your budget. With ReVroom, you’re not just buying a car. You’re gaining access to a community and marketplace built specifically for vehicles with history, where transparency and fair dealing come standard.

Frequently asked questions

What types of insurance can I get for a salvage title car?

You cannot get insurance for a salvage title car for on-road use. The vehicle must first be repaired, inspected, and retitled as rebuilt before any insurance company will provide coverage. Once retitled, liability insurance becomes available, though comprehensive and collision coverage remain difficult to obtain.

Why is liability insurance more expensive for rebuilt title cars?

Insurers charge 10 to 30 percent more because rebuilt title vehicles present higher risk due to unknown repair quality, valuation challenges, and potential hidden damage. These factors increase the insurer’s uncertainty about future claims and appropriate payout amounts.

Can I get full coverage on a rebuilt title vehicle?

Full coverage including comprehensive and collision is rarely available for rebuilt title vehicles. Most insurers offer only liability coverage. Some specialty insurers may provide comprehensive and collision after independent inspection, but premiums are substantially higher and payouts are based on the vehicle’s reduced market value.

How does a rebuilt title affect my insurance premiums?

Rebuilt titles typically increase liability insurance premiums by 10 to 30 percent compared to clean title equivalents. The exact increase depends on your state, the insurer, the vehicle’s repair quality, and available documentation. Some insurers refuse rebuilt title coverage entirely, limiting your options.

What should I disclose to my insurer about a rebuilt title?

Disclose everything, including the rebuilt title status, the original reason for the total loss designation, all repair documentation, state inspection results, and any available photos or reports. Complete transparency prevents claims denial and ensures your coverage remains valid. Hiding or minimizing vehicle history can void your policy.