How to buy rebuilt title vehicles wisely in 2026

March 16, 2026

Buying a car can stretch your budget to its limits, pushing many shoppers toward alternatives that promise significant savings. Rebuilt title vehicles offer an appealing solution, often priced 20 to 60 percent below comparable clean title cars. But these vehicles come with complexity and risks that demand careful evaluation. This guide walks you through everything you need to know about rebuilt title cars, from understanding what the designation means to executing a smart purchase that protects your investment and keeps you safe on the road.

Table of Contents

- Understanding Rebuilt Title Vehicles

- Preparing To Buy: What You Need To Check And Know

- Executing The Purchase: Step By Step Guide To Buying Rebuilt Title Vehicles

- Verifying Your Purchase And Planning For Ownership

- Explore Revroom For Rebuilt Title Vehicle Resources

- FAQ

Key takeaways

| Point | Details |

|---|---|

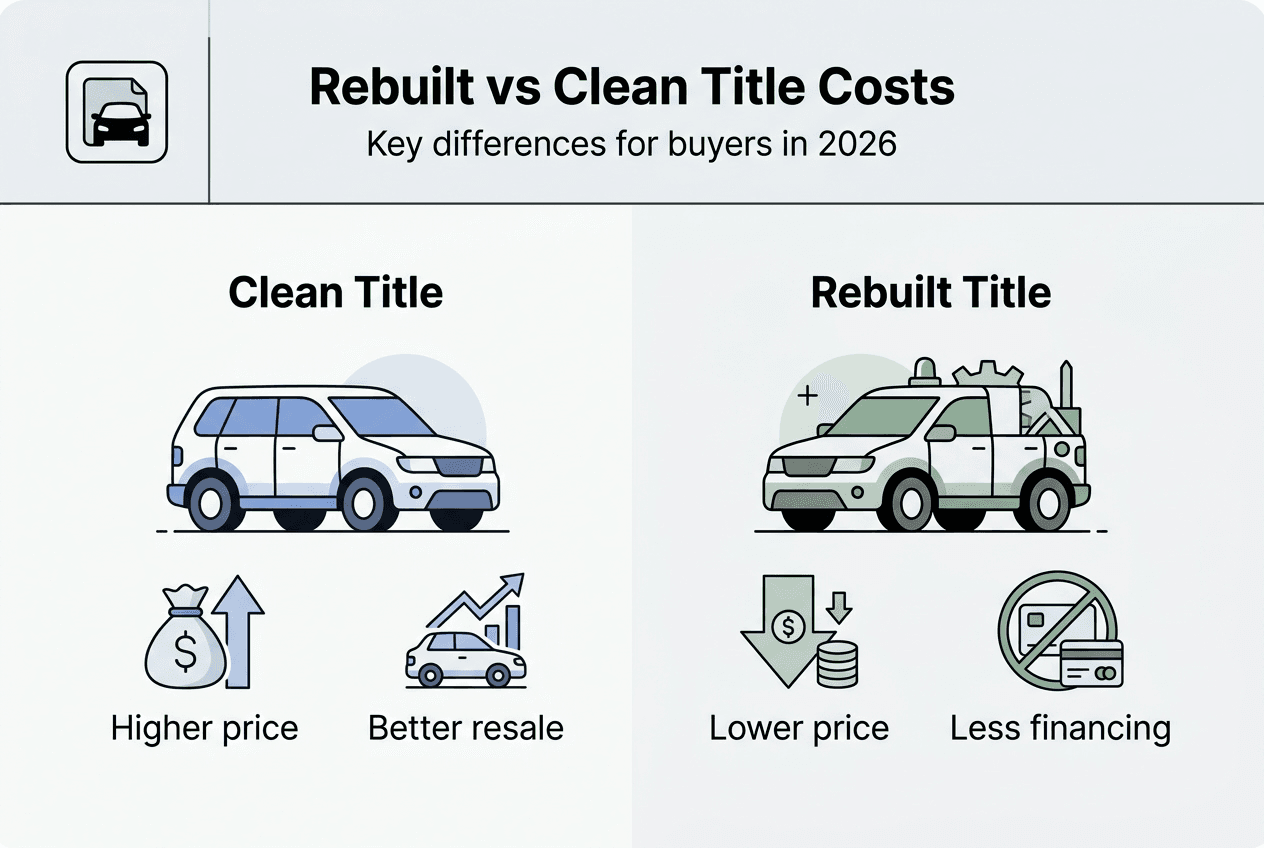

| Cost savings | Rebuilt title cars cost 20 to 60% less than clean title vehicles |

| Insurance challenges | Coverage options are more limited with higher premiums expected |

| Safety varies | Vehicle safety depends entirely on repair quality and thorough inspection |

| Lower resale value | Expect resale values 30 to 50% below comparable clean title cars |

| Due diligence essential | Thorough evaluation and independent inspection are non negotiable |

Understanding rebuilt title vehicles

A rebuilt title indicates a car was totaled and subsequently repaired to be roadworthy. Insurance companies declare vehicles total losses when repair costs exceed a certain percentage of the car’s value, typically 70 to 90 percent depending on state regulations. After repairs are completed, the vehicle passes a state inspection confirming it meets safety and operational standards.

The reasons behind rebuilt titles vary widely. Some vehicles earned their status through minor incidents like hail damage, paint defects, or theft recovery. Others went through more serious events like collisions or flood exposure. Not all vehicle history is equal. A car rebuilt after hail damage presents far different risks than one repaired following flood exposure, which can cause hidden electrical and mechanical problems that surface months or years later.

Once a vehicle receives a rebuilt title, it carries that designation permanently. The title can never revert to clean status, regardless of repair quality or how well the car performs over time. This permanence affects resale value and buyer perception for the vehicle’s entire life.

Common misconceptions cloud rebuilt title vehicles. Many people assume rebuilt equals unsafe or worthless, but salvage vs rebuilt titles represent very different categories. Rebuilt vehicles have passed inspections and are legally drivable, while their counterparts remain off limits for road use. Another myth suggests these cars are impossible to insure, but reality proves more nuanced. Coverage exists, though with limitations.

Understanding these fundamentals helps you approach rebuilt title vehicles with realistic expectations rather than unfounded fears or naive optimism.

Preparing to buy: what you need to check and know

Before you start shopping, set realistic expectations about pricing, insurance, financing, and ownership costs. Rebuilt title vehicles offer 20 to 60% savings compared to clean title equivalents, with actual discounts varying by make, model, and vehicle history. Economy cars might save you a few thousand dollars, while luxury vehicles can put $10,000 to $15,000 back in your pocket.

Insurance presents real challenges but not insurmountable ones. While some carriers refuse coverage entirely, others offer policies with restrictions. You’ll likely face higher premiums, sometimes 20 to 30 percent above standard rates. Many insurers limit you to liability coverage only, excluding collision and comprehensive options. About 20 percent of insurance companies will consider rebuilt title vehicles, so plan to shop around and get multiple quotes. Check out insurance for rebuilt titles to understand what coverage looks like in practice.

Financing options shrink considerably with rebuilt titles. Most banks hesitate to finance these vehicles due to lower collateral value and perceived risk. When financing is available, expect higher interest rates, sometimes 2 to 4 percentage points above standard auto loan rates. Lenders often require larger down payments, typically 25 to 50 percent of the purchase price, and offer shorter loan terms. Many buyers find paying cash simplifies the process significantly. Learn more about financing rebuilt cars to explore your options.

Pro Tip: Calculate total ownership costs before committing. Add higher insurance premiums, potential financing costs, and reduced resale value to your initial savings to see if the math still works in your favor.

Cost comparison: rebuilt vs clean title ownership

| Cost Factor | Clean Title | Rebuilt Title | Difference |

|---|---|---|---|

| Purchase price | $25,000 | $15,000 | Save $10,000 |

| Annual insurance | $1,200 | $1,500 | Pay $300 more |

| Financing rate | 6% APR | 10% APR | Pay 4% more |

| 5 year resale value | $15,000 | $7,500 | Lose $7,500 more |

Before viewing any vehicle, prepare your evaluation checklist. You need complete vehicle history reports showing the original incident that led to the rebuilt status. Request state inspection documents proving the car passed safety requirements. Arrange for an independent mechanic’s inspection, ideally someone experienced with rebuilt vehicles who knows what red flags to spot. Budget $150 to $300 for this inspection, money well spent to avoid a $15,000 mistake.

Resale values run 30 to 50% lower than comparable clean title vehicles. Factor this depreciation into your decision, especially if you plan to sell or trade the car within a few years. The rebuilt designation follows the vehicle forever, limiting your buyer pool when it’s time to move on.

Executing the purchase: step by step guide to buying rebuilt title vehicles

Start your search with sellers who specialize in rebuilt title vehicles. These dealers understand the market, typically provide more complete vehicle history information, and often have established relationships with inspectors and insurance providers. Private sellers can offer good deals, but they may lack documentation or transparency about repairs.

Request comprehensive documentation before scheduling a viewing. You want the complete vehicle history report, details about the original incident, repair invoices showing what work was done and by whom, and the state inspection certificate. Quality sellers provide this information upfront. Hesitation or incomplete records signal potential problems.

Arrange your independent inspection before negotiating price. Your mechanic should examine:

- Frame and structural integrity for proper alignment and repair quality

- All safety systems including airbags, seatbelts, and crash sensors

- Electrical systems for signs of water exposure or faulty repairs

- Engine and transmission performance under various conditions

- Suspension and steering components for wear or improper installation

- Paint and body work quality as indicators of overall repair standards

The inspection report becomes your negotiating tool. Document every concern, estimate repair costs for any issues found, and use these facts to justify your offer.

Pro Tip: Test drive the vehicle in varied conditions. Highway speeds, stop and go traffic, and rough roads reveal problems that don’t show up in parking lot test drives.

Negotiation framework for rebuilt title purchases

| Starting Point | Adjustment Factor | Your Offer |

|---|---|---|

| Comparable clean title price | Minus 40% rebuilt discount | Base offer |

| Inspection issues found | Minus estimated repair costs | Adjusted offer |

| Missing documentation | Minus 5 to 10% risk premium | Final offer |

| Excellent repair quality | Plus 5% quality premium | Maximum offer |

Compare your target vehicle’s asking price against clean title equivalents and factor in the risks of buying rebuilt vehicles. If a clean title version sells for $20,000, a rebuilt title should list around $12,000 to $16,000 depending on vehicle history and condition. Sellers pricing rebuilt vehicles at only 10 to 20 percent discounts either don’t understand the market or hope you don’t.

Negotiate based on documented facts, not emotions. Present your inspection findings, comparable pricing data, and total ownership cost calculations. Good sellers respect informed buyers and adjust prices for legitimate concerns.

Finalize the purchase with clear written agreements. The bill of sale must explicitly state the rebuilt title status. Include any seller warranties or guarantees in writing, though most rebuilt vehicles sell as is. Verify the title shows the rebuilt designation before signing anything. Transfer the title according to your state’s requirements, which may include additional inspections or documentation.

Verifying your purchase and planning for ownership

After completing the purchase, confirm everything is in order. Check that the title documents clearly show the rebuilt status and match the vehicle identification number. Verify all repair records are in your possession. Review the state inspection certificate to ensure it’s current and legitimate.

Secure insurance coverage immediately. Contact multiple carriers since options vary widely. Be prepared to provide detailed vehicle history and repair documentation. Some insurers require their own inspection before issuing policies. Rebuilt title insurance costs typically run higher than standard coverage, but shopping around can save you hundreds annually.

Establish a rigorous maintenance schedule. Rebuilt vehicles benefit from more frequent inspections to catch developing problems early. Change fluids on the conservative end of recommended intervals. Pay special attention to systems related to the original incident. If the car was rebuilt after front end collision, monitor alignment, suspension components, and steering systems closely.

Keep meticulous records of all maintenance, repairs, and inspections. This documentation serves two purposes. First, it helps you track the vehicle’s condition and identify patterns that might indicate underlying problems. Second, thorough records increase resale value by demonstrating responsible ownership and proper care.

Plan for eventual resale from day one. Hidden costs like higher insurance premiums and reduced resale value can offset initial savings if you don’t account for them. When selling time comes, be transparent about the vehicle’s history. Provide all documentation to potential buyers. Price competitively based on current rebuilt title market values, not what you wish the car was worth.

Monitor vehicle performance continuously. Strange noises, unusual vibrations, warning lights, or changes in handling require immediate attention. Problems in rebuilt vehicles can indicate repair quality issues or hidden concerns related to the original incident. Address issues promptly rather than hoping they’ll resolve on their own.

Budget for unexpected repairs. Even well repaired vehicles can develop problems, and rebuilt title cars carry higher risk of surprise issues. Setting aside $50 to $100 monthly creates a repair fund that prevents financial stress when maintenance needs arise.

Explore ReVroom for rebuilt title vehicle resources

Buying a rebuilt title vehicle wisely requires knowledge, transparency, and access to the right resources. ReVroom specializes in connecting budget conscious buyers with quality rebuilt title vehicles through a marketplace built on transparency and trust. Every listing includes comprehensive vehicle history information and photos showing what the car looked like before repairs, eliminating the $150 per vehicle investigation costs typical buyers face.

The platform provides detailed guides on financing rebuilt cars and understanding insurance coverage for rebuilt titles, helping you navigate the complexities of rebuilt vehicle ownership. Whether you’re researching your first rebuilt title purchase or you’re an experienced buyer looking for your next vehicle, ReVroom offers the transparency and resources you need to make confident decisions. Browse listings, compare prices, and access expert insights that turn rebuilt title complexity into straightforward value.

FAQ

Are rebuilt title vehicles safe to drive?

Rebuilt title vehicles can be safe if repairs were completed properly and the car passed required state inspections. However, safety depends on repair quality and the type of original incident. A vehicle rebuilt after minor hail damage presents different safety considerations than one repaired following a serious collision. Always arrange an independent mechanic’s inspection before purchasing to verify repair quality and identify any safety concerns.

Can I get insurance for a rebuilt title vehicle?

Yes, insurance is available for rebuilt title vehicles, though options are more limited than for clean title cars. Approximately 20 percent of insurance carriers offer coverage, often with restrictions. Expect higher premiums, typically 20 to 30 percent above standard rates, and many insurers limit coverage to liability only. Insurance can be challenging to find, so contact multiple carriers and be prepared to provide detailed vehicle history and repair documentation.

How much can I save when buying a rebuilt title car?

Savings vary significantly based on make, model, and vehicle history. Rebuilt title vehicles offer 20 to 60% savings compared to equivalent clean title cars. Economy vehicles might save you $2,000 to $5,000, while luxury models can deliver savings of $10,000 to $15,000 or more. The lower price reflects the vehicle’s history and reduced resale value. Calculate total ownership costs including higher insurance and reduced resale value to determine true savings.

Will I have difficulty financing a rebuilt title vehicle?

Financing rebuilt title vehicles is significantly more challenging than financing clean title cars. Most banks hesitate to provide loans due to lower collateral value and perceived risk. When financing is available, expect higher interest rates, often 2 to 4 percentage points above standard rates, along with larger down payments of 25 to 50 percent. Loan terms are typically shorter as well. Many buyers find that paying cash simplifies the purchase process considerably.

Recommended

- Are rebuilt title cars safe? A 2026 buyer’s guide | ReVroom

- Rebuilt title cars for sale: buyer’s guide to savings in 2026 | ReVroom

- How to Best Sell a Rebuilt Title Car in 2024

- How to Price a Rebuilt Title Car for Smart Buyers | ReVroom

- Master the car loan approval process in Australia 2026 | OptiCheck