Purchasing a Salvage Title Car: Your 2026 Buyer's Guide

June 24, 2026

TL;DR:

- Buying a salvage title vehicle offers significant savings but involves permanent branding and resale challenges.

- Thorough research, independent inspections, and insurance confirmation are essential before purchase.

Purchasing a salvage title car is defined as buying a vehicle that an insurance company has declared a total loss, meaning repair costs exceeded a set percentage of the car’s market value. The upfront savings are real. Buyers routinely pay 20% to 50% less than market value on these vehicles. But the title branding is permanent, and the path from “great deal” to “great ownership experience” runs straight through thorough research, an independent inspection, and a clear-eyed look at insurance and resale realities. This guide walks you through every step so you can decide whether a branded title vehicle is the right call for your budget and your situation.

What is a salvage title and how does it differ from a rebuilt title?

A salvage title is a legal designation issued by a state DMV after an insurance company declares a vehicle a total loss. That declaration happens when estimated repair costs exceed a threshold, typically 75%–80% of the car’s actual cash value, though the exact percentage varies by state. A salvage-titled vehicle cannot be legally registered or driven on public roads until it is repaired and passes a state inspection.

A rebuilt title, sometimes called a reconstructed or branded title, is what a vehicle receives after it has been repaired and passed that state inspection. The rebuilt title signals road legality, but the original branding stays on the vehicle’s record permanently. That distinction matters enormously for insurance, financing, and resale.

Here is a side-by-side look at the two designations:

| Feature | Salvage title | Rebuilt title |

|---|---|---|

| Road legal | No | Yes |

| Registerable | No | Yes (most states) |

| Insurance available | Very limited | Generally available |

| Financing available | Rarely | Sometimes |

| Permanent brand | Yes | Yes |

State rules add another layer of complexity. Some states require a separate rebuilt title inspection beyond the standard safety check. Others allow registration with minimal documentation. Before you buy, confirm your state’s specific requirements with the DMV, because the process and costs vary widely.

- Salvage title: total loss designation, not road legal

- Rebuilt title: repaired, inspected, and road legal

- Both carry a permanent brand on the vehicle history

- State inspection requirements differ significantly by location

- Insurance and financing options expand considerably once a vehicle holds a rebuilt title

What are the main benefits and risks of buying a salvage title vehicle?

The financial case for buying a branded title vehicle is straightforward. Buyers save 20% to 50% off market value at purchase. That kind of discount can put a much newer or better-equipped car within reach for a budget-conscious buyer. The catch is that the resale value is permanently reduced by 20%–40% compared to a clean title equivalent. If you plan to keep the car for years, that resale hit matters less. If you expect to flip it in two years, the math gets harder.

Insurance is the area where buyers most often get surprised. Full coverage is harder to obtain for branded title vehicles, and some insurers charge surcharges up to 20% or decline coverage entirely. That does not mean insurance is impossible to find. It means you need to shop around and get written confirmation before you buy, not after.

Financing is the other major hurdle. Traditional auto loans are rarely available for salvage or branded title vehicles. Most buyers pay cash or use a personal loan. That limits the buyer pool to people with liquidity, which is worth knowing upfront.

Pro Tip: Before you fall in love with a specific vehicle, call your insurance provider and give them the VIN. Ask specifically whether they will write a full coverage policy on a rebuilt title vehicle. Get the answer in writing. This one step saves you from a very expensive surprise.

Experts are consistent on who this type of purchase suits best. Buying a branded title vehicle works best for buyers who have mechanical knowledge, can pay cash, and plan on long-term ownership. If you check all three boxes, the savings are real and the risks are manageable.

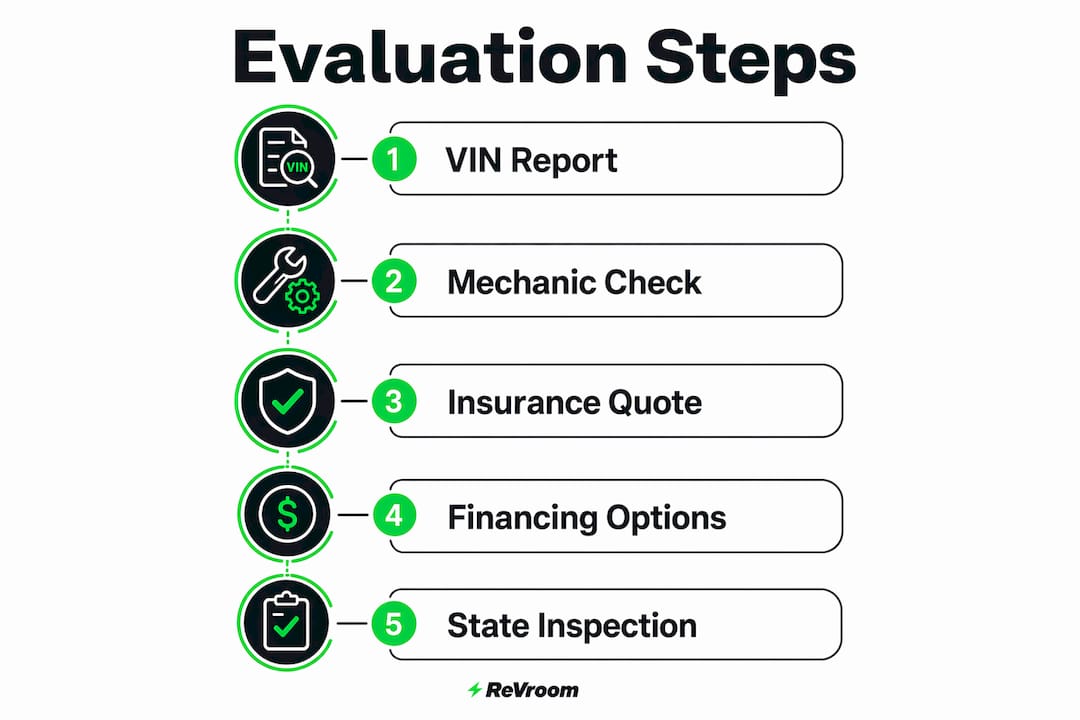

How to evaluate a salvage title car before you buy

Evaluation is where most buyers either protect themselves or leave money on the table. A structured approach makes the difference.

-

Pull a full vehicle history report. Use the VIN to run a report through a recognized service. A vehicle history report reveals the original loss event, prior owners, and any title transfers. Gaps in the history are a red flag.

-

Request original vehicle history photos and repair invoices. Ask the seller for photos of what the car looked like before repairs, along with itemized repair invoices. Absence of these documents often signals that the repair quality is something the seller would rather you not scrutinize.

-

Get an independent pre-purchase inspection (PPI). A state safety inspection is a baseline check. A comprehensive PPI by a trusted mechanic goes much deeper, covering structural integrity, frame alignment, airbag status, and electrical systems. These are the issues that state inspections routinely miss.

-

Verify the title authenticity. Title washing is a real fraud risk. It happens when a vehicle is registered across multiple states to obscure a branded title. Confirm the title is legitimate and matches the VIN history before you hand over any money.

-

Confirm insurance coverage before purchase. Get written insurer confirmation that they will cover the specific VIN under the policy type you need. Do this before the purchase, not after.

| Evaluation step | What it reveals |

|---|---|

| VIN history report | Prior loss events, ownership chain, title transfers |

| Original photos and repair invoices | Repair quality and scope of prior vehicle history |

| Independent PPI | Structural, electrical, and mechanical condition |

| Title authenticity check | Fraud risk and title washing |

| Insurer written confirmation | Coverage availability before you commit |

Pro Tip: Bring a mechanic you trust to the in-person inspection, not one recommended by the seller. An independent set of eyes on the frame rails, welds, and undercarriage is worth every dollar of the inspection fee.

How to handle financing, insurance, and registration

The financial and legal steps after you decide to buy are where deals fall apart for unprepared buyers. Knowing what to expect keeps you in control.

Financing options are limited. Traditional lenders, including most banks and credit unions, treat branded title vehicles as too risky to secure a loan against. Your realistic options are a cash purchase or an unsecured personal loan. Personal loans carry higher interest rates than auto loans, so factor that cost into your total budget before you commit.

Insurance requires active shopping. Not every insurer handles branded title vehicles the same way. Some offer full coverage without issue. Others add surcharges or limit you to liability only. The right move is to contact multiple insurers, provide the VIN, and ask specifically about comprehensive and collision coverage. Never assume your existing policy transfers automatically. Explicit insurer approval is mandatory before you finalize the purchase.

Registration involves state-specific steps. Most states require a rebuilt title inspection before they issue registration. That inspection has a fee, a wait time, and specific documentation requirements. Here is what to prepare:

- Proof of completed repairs and a passing inspection certificate

- A valid rebuilt or reconstructed title in the seller’s name

- Bill of sale and any required state forms

- Payment for title transfer and registration fees

- Proof of insurance before the DMV will register the vehicle

Timing matters here. Some states have inspection backlogs. Build extra time into your purchase timeline so you are not stuck with a car you cannot legally drive while waiting for a registration appointment.

Common mistakes to avoid when buying a branded title vehicle

The most expensive mistakes in this process are predictable. Knowing them in advance costs nothing.

- Relying only on the state inspection. State inspections confirm basic roadworthiness. They do not evaluate frame straightness, airbag deployment history, or repair quality. A private PPI is not optional if you want real confidence.

- Skipping the repair documentation. Buyers who accept a seller’s verbal assurances about repair quality without seeing invoices and photos are taking an unnecessary risk. Documentation is the only way to verify what was actually fixed.

- Assuming resale will be easy. Permanent title branding limits resale almost entirely to private party sales. Dealerships rarely accept branded title trade-ins. Price your exit strategy accordingly before you buy.

- Underestimating total ownership costs. Buyers frequently underestimate total costs including post-purchase repairs and reduced insurance payouts. Build a repair buffer into your budget from day one.

- Not verifying seller credibility. Ask for references, check reviews, and look for sellers who proactively share vehicle history and documentation. Transparency from the seller is one of the strongest signals that a deal is worth pursuing.

“A rebuilt title does not guarantee factory-quality restoration. Legal roadworthiness does not equal original condition.” — ClarityCheck

That quote captures the mindset every buyer needs. The car passed inspection. That is a starting point, not a finish line. Your due diligence is what fills the gap between those two things.

Key Takeaways

Buying a branded title vehicle rewards prepared buyers with real savings, but only when vehicle history, inspection, insurance, and financing are addressed before the purchase is final.

| Point | Details |

|---|---|

| Significant upfront savings | Branded title vehicles sell at 20%–50% below market value, making newer models accessible on a budget. |

| Permanent resale impact | Resale value is reduced by 20%–40% permanently, so plan for long-term ownership to maximize value. |

| Insurance requires active research | Contact multiple insurers with the specific VIN and get written coverage confirmation before buying. |

| Independent PPI is non-negotiable | A private mechanic’s inspection uncovers structural and electrical issues that state inspections miss. |

| Financing is mostly cash or personal loan | Traditional auto loans are rarely available; budget for a cash purchase or higher-rate personal loan. |

What we’ve learned from watching buyers get this right (and wrong)

Here is the honest truth we have picked up from watching this market closely. The buyers who walk away happy from a branded title purchase share one trait: they treated the evaluation process as seriously as the purchase itself. They hired their own mechanic. They read every repair invoice. They called their insurer before they fell in love with the car.

The buyers who regret it skipped steps. They trusted a seller’s word over documentation. They assumed insurance would sort itself out. They did not budget for anything going wrong after the purchase. The car itself was rarely the problem. The process was.

There is real value beneath the surface of a well-repaired vehicle with a branded title. We believe that fully. But we also know that the risks are real and the myths about these vehicles are everywhere. One of the most persistent myths is that rebuilt title cars are nearly impossible to insure. That is not accurate for most buyers who shop around and provide full vehicle history to their insurer. Another is that all branded title cars have severe histories. Many carry titles from hail events, paint defects, or theft recovery, not catastrophic collisions.

The opportunity here is genuine. So is the need for clear eyes and a good mechanic. Those two things together are what turn a great price into a great car.

— Revroom Editorial Team

Revroom makes the rebuilt title market work for you

Revroom is the only online marketplace built specifically for rebuilt title vehicles, and the difference shows up in every listing.

Properly vetting a rebuilt vehicle on your own typically costs buyers around $150 per vehicle in reports and investigations. Revroom includes vehicle history photos and pre-repair documentation directly in each listing, so you can compare vehicles with confidence before you ever contact a seller. Every listing is built around the transparency that makes a smart purchase possible. If you are ready to find a rebuilt title vehicle that fits your budget and your standards, browse current listings on Revroom and see what a fair, transparent marketplace actually looks like. You can also read more about how salvage becomes a rebuilt title to understand exactly what a vehicle goes through before it earns road-legal status.

FAQ

What does a salvage title mean for a car?

A salvage title means an insurance company declared the vehicle a total loss after its repair costs exceeded a set percentage of its market value. The vehicle cannot be legally driven or registered until it is repaired and passes a state inspection, at which point it receives a rebuilt title.

Should you buy a salvage title car if you are on a budget?

Buying a branded title vehicle can make sense for budget-conscious buyers who can pay cash, have access to a trusted mechanic, and plan to keep the car long term. The upfront savings of 20%–50% are real, but resale value is permanently reduced and financing options are limited.

How hard is it to get insurance on a rebuilt title car?

Insurance is available for most rebuilt title vehicles, though it requires shopping around. Some insurers add surcharges or limit coverage options, so contact multiple providers with the specific VIN and get written confirmation of coverage before you finalize any purchase.

What is the most important step before buying a branded title vehicle?

An independent pre-purchase inspection by a mechanic you hire yourself is the single most important step. State inspections confirm basic safety but do not evaluate frame integrity, airbag history, or repair quality. A private PPI covers all of that.

Can you get a loan to buy a salvage or rebuilt title car?

Traditional auto loans are rarely available for branded title vehicles. Most buyers pay cash or use an unsecured personal loan. Factor the higher interest rate of a personal loan into your total cost before committing to a purchase.