Rebuilt Title Insurance with GEICO: What to Know in 2026

June 5, 2026

TL;DR:

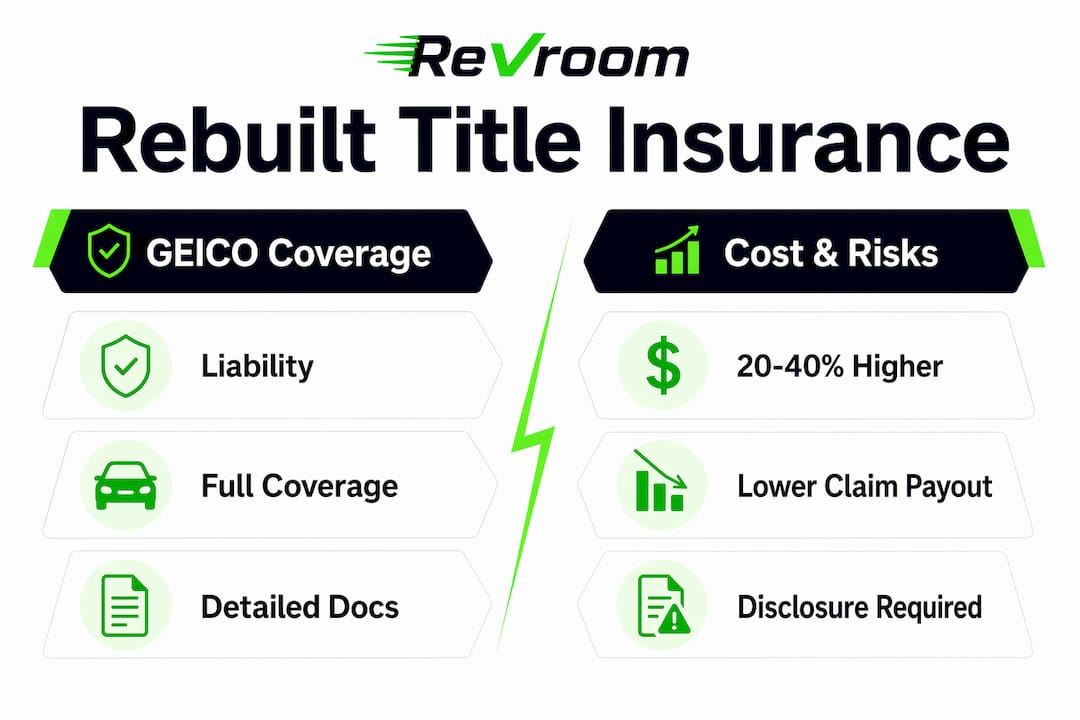

- GEICO offers rebuilt title vehicle coverage with stricter documentation requirements and premiums 20 to 40 percent higher than clean title policies. Proper repair records, photos, and transparency are essential for full coverage eligibility, which is handled through direct agent contact. Insuring rebuilt titles with GEICO improves with thorough preparation and organized documentation, making coverage accessible despite additional process steps.

Rebuilt title insurance with GEICO is available for vehicles that have been repaired and re-registered after being declared a total loss, but it comes with stricter documentation requirements and higher premiums than a standard clean title policy. GEICO offers both liability and full coverage options for rebuilt title vehicles, making it one of the more accessible major insurers in this space. The catch is that GEICO’s underwriting weighs your repair documentation heavily, including before and after photos, itemized receipts, and repair estimates. If you walk in prepared, the process is far more straightforward than most people expect. This guide breaks down exactly what GEICO covers, what it costs, and how it stacks up against State Farm and other major insurers.

What coverage does GEICO offer for rebuilt title vehicles?

GEICO offers rebuilt title vehicle coverage across two main tiers: liability only and full coverage, which includes both comprehensive and collision. Liability coverage is the easier path and is available to most rebuilt title vehicles without extensive documentation. Full coverage, however, requires additional steps before GEICO will bind the policy.

According to MoneyGeek’s analysis, GEICO’s underwriting process for rebuilt titles starts with a meticulous documentation review rather than a standard online quote. That means you typically cannot get a rebuilt title quote through GEICO’s website. You need to call directly and have your paperwork ready.

Here is what GEICO generally requires for full coverage consideration:

- Before and after repair photos showing the vehicle’s condition

- Itemized repair receipts from the shop that completed the work

- Written repair estimates from licensed mechanics

- A copy of the rebuilt title issued by your state’s DMV

- Proof of a passed state safety inspection

The distinction between a rebuilt title and a vehicle that has not yet been repaired matters here. Vehicles with unrepaired status cannot be legally driven or insured. Once a vehicle passes state inspection and receives a rebuilt title, GEICO and other major insurers can provide full coverage. That is a critical point that gets lost in a lot of online confusion about this topic.

Pro Tip: Organize your repair documentation into a single digital folder before calling GEICO. Having photos, receipts, and your title scanned and ready to share speeds up the underwriting process considerably.

Why does insuring a rebuilt title vehicle with GEICO cost more?

Rebuilt title insurance costs 20 to 40 percent more than a comparable clean title policy, which translates to roughly $180 to $300 more per year on average. That premium increase reflects two things: higher perceived risk and genuine difficulty in determining the vehicle’s actual cash value.

The valuation challenge is the bigger issue. Because rebuilt vehicles carry a vehicle history that affects their market value, insurers like GEICO cannot simply look up a Kelley Blue Book number and call it a day. Determining actual cash value for a rebuilt title car requires additional inspection or documentation, which is why GEICO’s underwriting process is more involved than it is for clean title vehicles.

The cost difference also shows up at claim time. Claim payouts for rebuilt titles can run 20 to 40 percent lower than for clean title vehicles because the payout reflects the diminished market value of the rebuilt car. This means the savings you get when purchasing a rebuilt title vehicle at a lower price should factor into your expectations for what you would recover in a total loss claim.

| Cost factor | What it means for you |

|---|---|

| Premium increase | Budget $180 to $300 more annually compared to a clean title policy |

| Claim payout reduction | Expect payouts 20 to 40 percent lower than clean title equivalents |

| Valuation difficulty | GEICO may require inspection to establish actual cash value before binding full coverage |

| Documentation quality | Strong repair records can improve your rate and coverage options |

Pro Tip: Before buying a rebuilt title vehicle, check the cost to insure rebuilt cars by getting a quote from at least two insurers. The premium difference between providers can be significant, and shopping around takes less than an hour.

How does GEICO’s documentation requirement compare to other major insurers?

GEICO and State Farm both insure rebuilt title vehicles, but they take meaningfully different approaches to underwriting. State Farm relies primarily on mechanic inspections, while GEICO leans on detailed repair documentation including photos and itemized receipts. Neither approach is better in every situation. It depends on what you have available.

If you bought a rebuilt title vehicle from a reputable shop that kept thorough records, GEICO’s documentation approach works in your favor. You hand over the paperwork, the underwriter reviews it, and the process moves forward. If your repair history is thin or informal, State Farm’s inspection model may be easier to satisfy. You can read more about how State Farm handles rebuilt titles to compare directly.

Here is how the major players generally line up:

| Insurer | Primary requirement | Full coverage availability |

|---|---|---|

| GEICO | Detailed repair documentation and photos | Yes, with documentation review |

| State Farm | Certified mechanic inspection | Yes, with inspection approval |

| Progressive | Photo inspection | Yes, case by case |

| Some regional insurers | Liability only | Limited or none |

A few things worth knowing about GEICO’s approach specifically:

- GEICO’s underwriting for rebuilt titles is handled by agents, not automated systems. Call rather than quote online.

- The quality of your documentation directly affects both your eligibility for full coverage and your premium level.

- Professionally rebuilt vehicles with complete repair packages have a significantly easier time securing favorable coverage from GEICO.

- GEICO may request an independent inspection even when documentation is provided, particularly for higher-value vehicles.

The takeaway is that GEICO rewards preparation. Buyers who arrive with organized, thorough repair records are in a much stronger position than those who show up with a title and a handshake.

What should you disclose to GEICO when insuring a rebuilt title car?

Disclosing your vehicle’s rebuilt title status to GEICO is not optional. Failure to disclose rebuilt title status risks coverage disputes and outright claim denial. This is one of those areas where transparency is not just the right move. It is the only move that protects you.

GEICO’s policy terms require full transparency about a vehicle’s history during the underwriting process and throughout the life of the policy. If you file a claim and GEICO discovers the vehicle had a rebuilt title that was not disclosed, the claim can be voided entirely. That is a painful outcome that is entirely avoidable.

Here is what to keep organized and accessible throughout your policy:

- A copy of the rebuilt title document from your state DMV

- All repair receipts and estimates from the shop that completed the work

- Before and after photos of the vehicle

- The state safety inspection certificate confirming the vehicle passed

- Any appraisal documents if you had the vehicle independently valued

Proactive disclosure and organized documentation throughout the life of the policy is the standard GEICO expects, and meeting that standard protects you at claim time. Think of your repair folder less like paperwork and more like your insurance policy’s best friend.

How does choosing GEICO for rebuilt title insurance compare to alternatives?

GEICO sits in a solid middle position among major insurers for rebuilt title coverage. It offers full coverage with the right documentation, which puts it ahead of providers that limit rebuilt title policies to liability only. It is more documentation-intensive than State Farm, which may be a consideration depending on your situation.

Here is a practical breakdown of GEICO’s strengths and limitations:

- Strength: Full coverage is genuinely available, not just liability, for well-documented vehicles

- Strength: GEICO is a nationally recognized insurer with strong claims infrastructure

- Limitation: Online quoting does not work for rebuilt titles. You must call an agent directly

- Limitation: Documentation requirements are higher than some competitors, which can slow the process

- Limitation: Valuation uncertainty means full coverage pricing can vary significantly between vehicles

If you have strong repair documentation, GEICO is a competitive choice. If your records are limited, exploring State Farm’s inspection-based model or comparing rebuilt title insurers side by side is worth the time. The myth that rebuilt title vehicles are difficult or impossible to insure is simply not accurate. Most major insurers, GEICO included, have clear pathways to full coverage.

Pro Tip: When calling GEICO, ask specifically about their rebuilt title underwriting process and what documentation they need before your appointment. This prevents back-and-forth delays and gets you to a quote faster.

Key takeaways

GEICO provides full coverage for rebuilt title vehicles, but the process requires thorough repair documentation, transparent disclosure, and an expectation of premiums that run 20 to 40 percent higher than clean title policies.

| Point | Details |

|---|---|

| Full coverage is available | GEICO offers comprehensive and collision for rebuilt titles with proper documentation. |

| Premiums run higher | Budget $180 to $300 more annually compared to a clean title equivalent policy. |

| Documentation drives outcomes | Before and after photos, receipts, and repair estimates directly affect eligibility and rates. |

| Disclosure is non-negotiable | Failing to disclose rebuilt title status risks claim denial and policy disputes. |

| GEICO vs. State Farm | GEICO favors documentation; State Farm favors mechanic inspections. Match your approach to what you have. |

My honest read on GEICO for rebuilt title coverage

I have spent a lot of time looking at how major insurers handle rebuilt title vehicles, and GEICO’s approach is genuinely one of the more transparent ones once you understand the rules. The documentation requirement that trips people up is actually the same thing that protects you as a buyer. If a vehicle has thorough repair records, it is a better vehicle. GEICO’s underwriting process essentially forces that quality check.

Where I think buyers get frustrated is the expectation mismatch. They assume rebuilt title insurance works like any other auto insurance quote, and then they hit a wall when the online system does not cooperate. Calling an agent directly is not a burden. It is just a different process, and knowing that going in removes most of the friction.

My honest advice is this: if you are buying a rebuilt title vehicle and you want GEICO coverage, start gathering documentation before you finalize the purchase. Ask the seller for every repair record, every photo, and every receipt. The GEICO rebuilt title process rewards buyers who do their homework. And if your documentation is thin, that is a signal worth paying attention to before you sign anything.

Shopping multiple insurers is always smart. But do not let the extra steps with GEICO discourage you from pursuing full coverage. The path is clear. You just need the paperwork to walk it.

— Cameron

Find your next rebuilt title vehicle with confidence

Knowing how rebuilt title insurance works with GEICO is only half the equation. The other half is finding a vehicle with the kind of repair history that makes the whole process smooth. That is exactly what ReVroom was built for.

ReVroom is the only marketplace built specifically for rebuilt title vehicles, with vehicle history information and pre-repair photos included in every listing. You get the transparency GEICO’s underwriting process rewards, before you even make an offer. No guesswork, no surprises, and no $150 vetting reports. Browse rebuilt title vehicles on ReVroom and find a car whose paperwork tells a story worth insuring.

FAQ

Does GEICO insure rebuilt title vehicles?

Yes. GEICO offers both liability and full coverage for rebuilt title vehicles, though full coverage requires detailed repair documentation including photos, receipts, and repair estimates before the policy is bound.

How much more does it cost to insure a rebuilt title car with GEICO?

Rebuilt title insurance typically costs 20 to 40 percent more than a clean title policy, which averages $180 to $300 more per year. Claim payouts may also run lower due to the vehicle’s diminished market value.

Does State Farm cover rebuilt titles differently than GEICO?

Yes. State Farm relies primarily on certified mechanic inspections, while GEICO requires detailed repair documentation. If your records are strong, GEICO may be the better fit. If you prefer an inspection-based process, State Farm’s approach may be simpler to navigate.

What happens if I do not disclose a rebuilt title to GEICO?

Failing to disclose rebuilt title status is a serious risk. GEICO can deny your claim and dispute your coverage if the vehicle’s history was not disclosed during underwriting. Always be upfront about your vehicle’s title status from day one.

Can I get a rebuilt title insurance quote from GEICO online?

No. GEICO’s online quoting system does not accommodate rebuilt title vehicles. You need to call a GEICO agent directly and have your repair documentation ready to begin the underwriting process.