Does State Farm insure rebuilt title vehicles? What to know

May 5, 2026

TL;DR:

- Many major insurers, including State Farm, do insure rebuilt title vehicles, countering common myths about coverage difficulties.

- To qualify, owners must provide repair records, mechanic inspections, and photos demonstrating the vehicle’s safety and roadworthiness.

You’ve probably heard it before: “Good luck getting insurance on a rebuilt title.” It’s one of those automotive myths that gets repeated so often it starts to feel like fact. But here’s the truth most budget buyers never discover — State Farm does insure rebuilt title vehicles, making it one of the most accessible major insurers for this category of car. If you’ve been holding back from a rebuilt title purchase because you worried about coverage, it’s time to shift gears and see what’s actually on the table.

Table of Contents

- What is a rebuilt title and can you insure it?

- How State Farm covers rebuilt titles: Key requirements and coverage types

- The true cost: Premiums, value, and hidden trade-offs

- Common hurdles, edge cases, and expert advice for rebuilt title buyers

- A smarter approach: What most buyers miss about State Farm and rebuilt titles

- Find the right rebuilt title car — start your search confidently

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| State Farm insures rebuilt titles | State Farm is one of the few major insurers open to offering coverage for rebuilt title vehicles, unlike many competitors. |

| Higher premiums expected | Insurance on rebuilt titles typically costs 20-40% more than for clean titles due to increased risk. |

| Documentation is critical | Repair records, mechanic inspections, and photos are mandatory for getting insured. |

| Agent discretion matters | Coverage eligibility, especially for full coverage, depends heavily on your local State Farm agent and state rules. |

| Resale value is lower | Rebuilt cars often sell for 20-40% less, which can offset insurance hikes for value-focused buyers. |

What is a rebuilt title and can you insure it?

Let’s start with the basics, because this is where most of the confusion lives.

A vehicle earns a rebuilt title after it was previously declared a total loss by an insurance company and then professionally repaired and restored to roadworthy condition. The key word there is repaired. Before a rebuilt title is issued, the vehicle must pass a state DMV inspection to prove it meets safety standards. As WalletHub explains, rebuilt titles result from vehicles that have been repaired and passed state DMV inspections; a vehicle cannot be legally driven or insured until that process is complete.

This is a critical distinction that many people miss. The vehicle has cleared a formal hurdle. It isn’t in limbo. It is a roadworthy car with documented repairs and a new legal status. This is completely different from an unrepaired, uninspected vehicle. If you want to go deeper on how that process works, check out this salvage to rebuilt title guide that walks through the full journey step by step.

Here’s a quick breakdown of what separates these two title types:

- Pre-inspection vehicle: A vehicle that was declared a total loss but has not yet been repaired or inspected. It cannot be driven legally and is not insurable.

- Rebuilt title vehicle: That same vehicle after professional repairs and a passed state inspection. It can be titled, registered, driven, and insured.

“A rebuilt title is not a scarlet letter. It’s a graduation certificate. The car went through something, got fixed, got checked, and came out the other side ready to drive.”

Understanding this distinction is what separates buyers who find incredible value in rebuilt titles from those who leave deals on the table out of unnecessary fear. If you’re still sorting out the differences between these two title types, getting clear on them will change how you shop.

How State Farm covers rebuilt titles: Key requirements and coverage types

Once you understand what a rebuilt title is, the next step is knowing how State Farm actually handles insuring these vehicles and what you’ll need for success.

Here’s the headline: State Farm insures rebuilt titles while many competitors, including Geico, Allstate, and Progressive, often refuse. That alone makes State Farm worth your attention if you’re seriously shopping rebuilt title cars.

But State Farm doesn’t hand out policies without doing their homework first. To get coverage, you’ll typically need to bring the following:

- Repair records documenting all work done on the vehicle

- A certified mechanic inspection confirming the vehicle is in safe, roadworthy condition

- Photos of the vehicle in its current repaired state

- Repair reports showing what was addressed and how

According to documentation requirements outlined by insurers, these repair records, certified mechanic inspections, photos, and repair reports are specifically required to prove roadworthiness. Think of it as showing your work. State Farm wants to see the receipts, literally and figuratively.

As for coverage types, here’s how the landscape looks:

| Coverage type | Availability for rebuilt titles | Notes |

|---|---|---|

| Liability only | Generally available | Covers damage you cause to others |

| Collision | Limited, case by case | Depends on state and agent |

| Comprehensive | Limited, case by case | Depends on vehicle history |

| Full coverage (collision + comprehensive) | Not guaranteed | More documentation required |

Liability is the most accessible option, while collision and comprehensive coverage may be offered but are evaluated case by case, with outcomes varying by state and the discretion of your local agent. That last part matters more than most buyers realize.

State Farm operates through a network of local agents, and those agents have real influence over what gets approved. An agent in one state may be more experienced with rebuilt title policies than an agent in another. This variation isn’t a flaw in the system. It just means your experience shopping for coverage will depend partly on who you’re talking to.

Pro Tip: Before you commit to a vehicle, call two or three local State Farm agents and describe the car’s specifics. Ask directly about coverage availability for that type of vehicle history. You’ll get a much clearer picture of what to expect, and you might find that one agent is far more familiar with rebuilt title coverage than another. This single step can save you real frustration down the road.

For a fuller breakdown of what State Farm offers, the State Farm coverage guide on ReVroom is a solid place to continue your research. And if you want to compare all your insurance options for rebuilt titles more broadly, that resource lays it all out clearly.

The true cost: Premiums, value, and hidden trade-offs

Understanding requirements is crucial, but most buyers care deeply about real costs and value — here’s what the data says about those numbers.

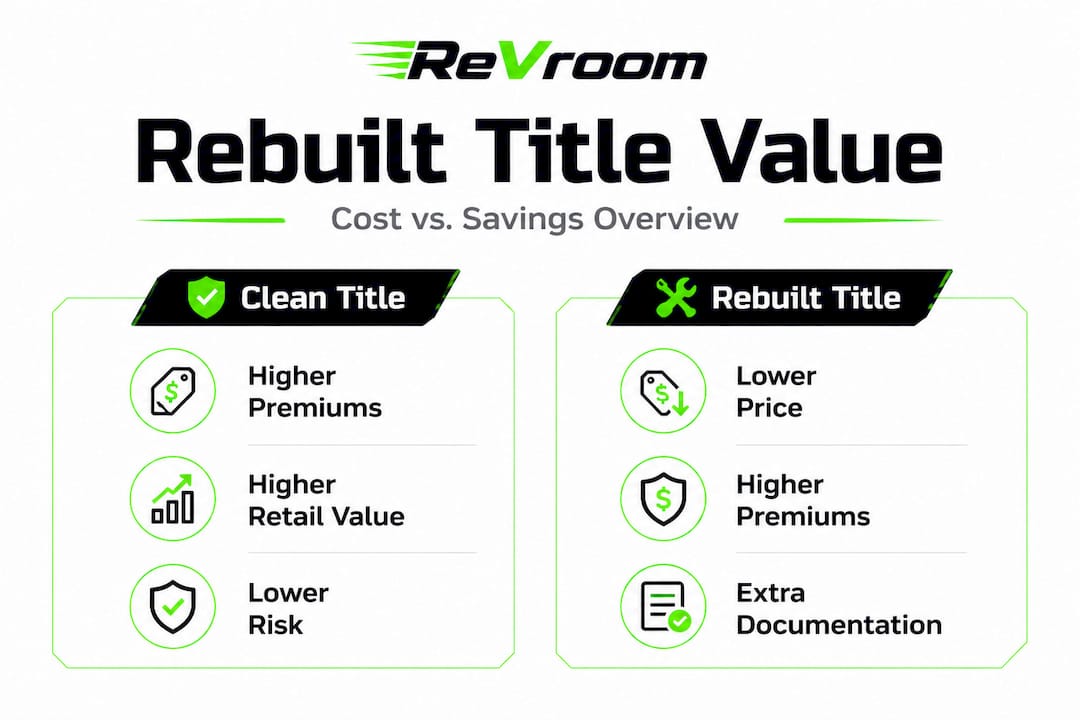

The honest answer is that insuring a rebuilt title costs more than insuring a clean title vehicle. Premiums run 20 to 40% higher on average for rebuilt title vehicles compared to their clean title counterparts, largely because insurers perceive a higher risk of undisclosed issues or future claims.

But here’s where the math gets interesting. Rebuilt title vehicles also sell for 20 to 40% less than comparable clean title vehicles. So you’re paying less upfront for the car, and yes, paying a bit more to insure it. For many buyers, those two forces offset each other in a way that still makes the purchase a genuinely smart financial decision.

Here’s a simplified look at how those numbers can shake out:

| Scenario | Clean title vehicle | Rebuilt title vehicle |

|---|---|---|

| Purchase price (example) | $20,000 | $12,000 to $14,000 |

| Annual insurance premium (est.) | $1,200 | $1,440 to $1,680 |

| 5-year insurance cost difference | Baseline | +$1,200 to +$2,400 |

| 5-year purchase price savings | Baseline | $6,000 to $8,000 |

Even with higher premiums, the purchase price difference often puts the rebuilt title buyer significantly ahead over the life of the vehicle. The savings don’t evaporate because insurance costs a little more.

That said, there are factors that most buyers overlook when it comes to the cost picture:

- Actual cash value (ACV) claims: If your rebuilt title car is totaled, State Farm will pay out its ACV, which reflects the market value of a rebuilt title car, not a clean title car. That means a lower payout. Period.

- Full coverage restrictions: Vehicles with certain types of vehicle history may not qualify for full coverage at all, which limits your protection.

- Resale value: When it’s time to sell, the rebuilt title stays with the car forever. Buyers will expect a discount, just as you received one.

- Agent knowledge gap: Some agents aren’t experienced with rebuilt titles and may quote you conservatively or incorrectly.

- Documentation quality: Gaps in repair records can result in higher premiums or denied coverage.

For a detailed breakdown of how these costs play out in practice, the rebuilt title insurance costs article on ReVroom breaks down real numbers in a way that makes the decision much clearer.

Common hurdles, edge cases, and expert advice for rebuilt title buyers

With the numbers in mind, let’s look at the pitfalls, exceptions, and expert strategies that separate savvy rebuilt title buyers from frustrated ones.

Common hurdles buyers face:

- Incomplete repair documentation from the seller

- Local agents who lack experience with rebuilt title policies

- Collision or comprehensive coverage being denied based on the vehicle’s prior history

- Lower claim payouts than expected when the ACV is applied

- Difficulty reselling the vehicle later at a fair price

Which vehicles are more likely to get full coverage?

Not all rebuilt titles are equal in insurers’ eyes. Full coverage is harder to obtain for vehicles with flood or fire history compared to those with collision history. Newer vehicles in excellent repaired condition are more likely to be approved for comprehensive and collision coverage. If the vehicle you’re considering was rebuilt after minor cosmetic or theft-related issues, your chances are better.

“Across states like Oklahoma and Michigan, State Farm agents report providing comprehensive and collision coverage on rebuilt titles, which shows this isn’t a blanket refusal policy — it’s a case-by-case evaluation.”

Expert advice worth following:

Some experts caution that while State Farm is flexible, claim payouts use lower ACV figures, which can complicate repairs if your car is damaged again. A few advisors suggest proceeding carefully given the resale and insurability considerations. That’s fair advice, and we’d never ask you to ignore it. But it’s worth noting that those same concerns apply to many used vehicles with complicated histories that carry clean titles, too.

Pro Tip: Before purchase, take the time to photograph every inch of the vehicle in its current repaired state. Get a written mechanic’s report confirming its condition. Keep digital copies of everything. This documentation doesn’t just help you with insurance. It actually makes the vehicle easier to sell someday, because future buyers see a complete, trustworthy paper trail. Good records transform a car with history into a car with proven history.

If you want a practical walkthrough of the entire process, the rebuilt title insurance step-by-step guide and this overview of insurance coverage for rebuilt titles are both worth bookmarking.

A smarter approach: What most buyers miss about State Farm and rebuilt titles

Here’s a perspective that most articles in this space never give you.

The biggest mistake rebuilt title buyers make isn’t choosing the wrong insurer. It’s focusing so narrowly on whether they can get insured that they forget to ask whether they’re making the right overall decision for their situation. Insurance approval is just one piece of a larger picture.

The true value of a rebuilt title vehicle comes from balancing three things together: a significantly lower purchase price, slightly higher insurance costs, and a clear-eyed understanding of long-term considerations like resale value and claim settlements. When buyers focus only on “Will State Farm approve me?”, they miss the forest for the trees.

Here’s what actually moves the needle: repair quality and documentation. A rebuilt title vehicle with thorough repair records, a certified inspection, and detailed photos is not just more insurable — it’s a fundamentally better asset. The documentation doesn’t just satisfy State Farm’s checklist. It tells the complete story of the car in a way that builds confidence at every stage: purchase, insurance, and eventual resale.

We’ve seen buyers approach this the right way — choosing a specific vehicle because they could verify the quality of its repairs, lining up a knowledgeable local agent before committing, and walking into the deal with their paperwork organized. Those buyers tend to come out ahead. The ones who struggle are usually those who treat insurance as an afterthought.

Choosing the right local agent often makes more difference than choosing the right insurer. A State Farm agent who has successfully written rebuilt title policies before is more valuable to you than any national branding. Ask your agent how many rebuilt title policies they’ve written. That one question will tell you a lot.

If you’re ready to make a smart, informed move, what buyers need to know about navigating this space is right there waiting for you.

Find the right rebuilt title car — start your search confidently

You’ve done the reading. You know rebuilt titles can be insured. You know State Farm is one of the better options out there. You know what documents to gather and what questions to ask your agent. Now the real fun begins: finding a vehicle worth insuring.

ReVroom is the only online marketplace built specifically for rebuilt title vehicles. Every listing comes with vehicle history information and photos of what the car looked like before repairs, so you can evaluate each vehicle with real transparency before spending a dime on independent reports. No guessing. No $150 investigation fees. Just clear, upfront information that lets you shop smarter. Browse ReVroom’s listings to find rebuilt title vehicles paired with the information you need to make a confident, well-informed purchase.

Frequently asked questions

Can I get full coverage on a rebuilt title car with State Farm?

Full coverage may be available on rebuilt titles through State Farm, but it’s not guaranteed. Approval varies by state, agent experience, and the specific vehicle’s repair history, so collision and comprehensive coverage are evaluated case by case.

How much more is insurance for a rebuilt title?

On average, premiums run 20 to 40% higher for rebuilt title vehicles compared to clean title vehicles. The exact increase depends on your location, insurer, vehicle type, and repair documentation.

What documents do I need for State Farm to insure my rebuilt car?

You’ll typically need repair records, a certified mechanic inspection, current photos of the vehicle, and proof that the car passed a state DMV inspection. Having all of this organized before contacting an agent speeds the process considerably.

Are rebuilt cars harder to sell after insurance?

Rebuilt title vehicles typically resell for 20 to 40% less than comparable clean title cars. That’s worth factoring into your long-term plan, though for buyers prioritizing upfront value over resale profit, it often still makes financial sense.

Why does State Farm require so much documentation for rebuilt vehicles?

The extra documentation helps State Farm verify that repairs were done properly and that the vehicle is genuinely road-ready. It’s their way of reducing uncertainty before committing to coverage, and honestly, it’s the same due diligence you’d want as a buyer too.