Rebuilt title car from a dealer: risks, benefits, and tips

May 15, 2026

TL;DR:

- A rebuilt title indicates a vehicle was declared a total loss, repaired, and passed safety inspections, but its history remains permanent. Buying a rebuilt title car can offer significant savings and quality repairs if thoroughly inspected beforehand. Proper documentation, dealer transparency, and independent inspections are essential for a confident purchase.

You’ve spotted a listing that looks almost too good to be true. Same make, same model, similar mileage as the car next door, but the price is noticeably lower. Then you see those two words: rebuilt title. Your instincts say run. But what if your instincts are working with incomplete information? The truth is, a rebuilt title car bought from a dealer can be a genuinely smart purchase, or a regrettable one, and the difference almost always comes down to how much you know before you sign anything.

Table of Contents

- What is a salvage (rebuilt) title car?

- Pros and cons: Is buying a rebuilt title car worth the risk?

- Dealer transparency and inspection: What you should demand

- Financing and insurance: What to expect

- Our perspective: The smart way to buy a rebuilt title car

- Take the next step with ReVroom

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your titles | Rebuilt cars were total losses but can be made road-legal after repair and inspection. |

| Dealer transparency is crucial | Require proof of repairs, inspection results, and a full vehicle history before committing. |

| Insurance and loans are tough | Expect higher insurance rates and check financing options before making an offer. |

| Real savings are possible | A carefully vetted rebuilt title car can offer substantial savings if you follow key precautions. |

| Due diligence pays off | Getting complete documentation and an independent inspection reduces your risk dramatically. |

What is a salvage (rebuilt) title car?

Let’s clear up the vocabulary first, because this is where a lot of confusion starts. People often use the terms interchangeably, but a vehicle with a rebuilt title and one with a different designation are two very different things at two very different points in their story.

When an insurance company decides that repairing a vehicle would cost more than its market value, they declare it a total loss. At that point, the car receives a branded title, sometimes called a total loss designation. That’s the beginning of the story, not the end. Once a qualified repair shop restores the vehicle and it passes a government safety inspection, the title gets updated to reflect its rebuilt status.

As Experian explains, a rebuilt title generally means a vehicle that was previously declared a total loss has been repaired and passed a state inspection, so it’s legal to register and drive again, but it will permanently carry that branded history. That permanent record is important to understand. No matter how many owners the car has, that history travels with it.

You can learn more about how cars are retitled through the full process, state by state, if you want to go deeper on the mechanics.

Here’s a quick comparison to anchor the terminology:

| Title type | What it means | Drivable? | History stays? |

|---|---|---|---|

| Clean title | No major insurance events | Yes | Yes, if incidents occurred |

| Rebuilt title | Repaired after total loss, passed inspection | Yes | Yes, permanently |

| Other branded titles | Not yet repaired or inspected | No | Yes, permanently |

A few things stand out from that table. First, clean title does not automatically mean the car has a spotless past. Many clean title vehicles have been in incidents that were never reported to insurance. Second, rebuilt title cars are legally roadworthy, they have passed inspection, and their history is fully disclosed. That transparency is actually a feature, not a flaw.

Rebuilt cars can be up to 50% less expensive than comparable clean title vehicles. That’s a real number. And when you understand what you’re looking at, that discount starts to look a lot more like an opportunity.

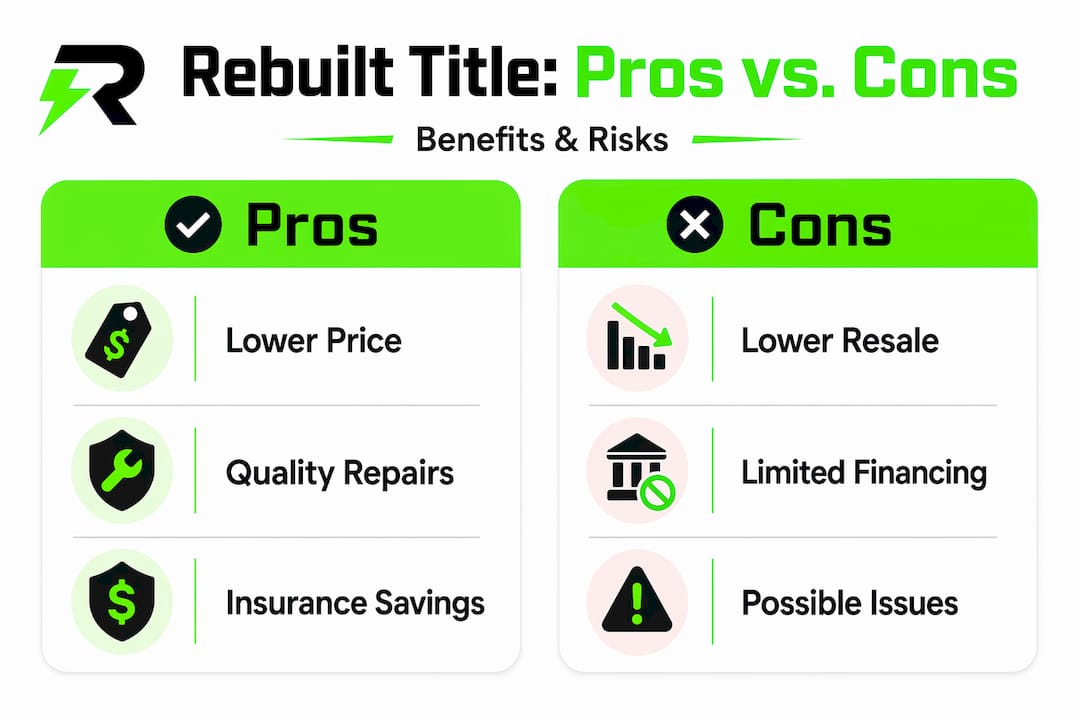

Pros and cons: Is buying a rebuilt title car worth the risk?

Here’s where we get honest. The price advantage is real. So are the tradeoffs. Knowing both sides is how you make a decision you won’t regret.

The case for buying a rebuilt title car

The most obvious upside is price. A well-repaired rebuilt title vehicle gives you access to makes and models that might otherwise be out of reach. Think about a midsize SUV or a well-equipped sedan at a fraction of the dealership sticker price. For a buyer who does their homework, that’s not a compromise. That’s a win.

Quality repairs matter here too. Many rebuilt vehicles have had major components replaced entirely rather than patched. Remanufactured car components often meet or exceed original factory standards, meaning some systems in a rebuilt car can actually be in better shape than the same systems in an older clean title car with deferred maintenance.

The benefits of rebuilt cars extend beyond the purchase price too. Lower insurance premiums compared to a newer clean title car, reduced depreciation (since the price has already been adjusted significantly), and access to newer technology and safety features that would cost far more in a clean title equivalent.

The case for caution

The rebuilt title car risks are real and worth naming directly. Resale value takes a hit. If you plan to sell the car in a few years, expect buyers to negotiate harder than they would on a clean title vehicle. Financing can be harder to secure. And some insurance providers will adjust their coverage terms.

The rebuilt title cons that catch buyers off guard most often are the ones that show up after purchase, particularly if the car was not properly inspected before the sale. That’s not a reason to avoid rebuilt cars. It’s a reason to inspect thoroughly before buying one.

Experian notes that rebuilt title vehicles can be less expensive than clean title cars but come with specific risks worth evaluating carefully. The key word is evaluating. Not avoiding. Evaluating.

“The goal isn’t to scare you away from a great deal. It’s to make sure the deal is actually great before you commit to it.”

Common mistakes to avoid when shopping for a rebuilt title car:

- Skipping a professional inspection because the car looks fine at first glance

- Trusting verbal assurances about repairs without seeing documentation

- Ignoring the vehicle history report and taking the seller’s word on the vehicle’s past

- Failing to check insurance costs before falling in love with a specific vehicle

- Not researching how rebuilt title savings vs risks stack up for your specific use case

Pro Tip: Before you fall for any specific car, run the VIN through a third-party history service and get an independent mechanical inspection. A few hundred dollars upfront can save you thousands later.

Dealer transparency and inspection: What you should demand

A reputable dealer selling a rebuilt title vehicle should have nothing to hide. In fact, the good ones will have paperwork ready before you even ask. If a dealer hesitates when you request documentation, that hesitation tells you something important.

Here’s what you should expect and demand from any dealer selling a rebuilt title car:

-

A clear explanation of what triggered the total loss designation. Not a vague “it was in an incident.” You want specifics: what happened, when, and how severe the event was. Different vehicle histories carry different implications, and you deserve the full picture.

-

Itemized repair records and receipts. Every major repair should be documented with parts used, labor performed, and the name of the shop that did the work. This isn’t just for your peace of mind. It’s also essential information for your insurance provider.

-

State inspection documentation. Most states require a safety inspection before a rebuilt title is issued. Ask to see the actual paperwork, not just the dealer’s assurance that it passed. Experian’s guidance specifically recommends requiring this documentation before you commit to a purchase.

-

A third-party VIN history and recall check. This should be a non-negotiable step in your process, regardless of how polished the dealer’s pitch is. A VIN check pulls the car’s full reported history and flags any open safety recalls that may not have been addressed.

Understanding dealer obligations on rebuilt cars and how dealers source rebuilt vehicles can also help you ask sharper questions and recognize when answers don’t quite add up.

Once you have all that documentation in hand, it’s also worth thinking about the cost picture beyond the purchase price itself. Smart buyers factor in repair strategies upfront. Proven strategies for managing vehicle repair costs can make a real difference over the life of ownership.

Pro Tip: Never skip a third-party inspection, regardless of how polished the dealer’s pitch sounds or how clean the car looks. A qualified mechanic sees things that are invisible to even the most experienced non-mechanic eye.

Financing and insurance: What to expect

Two things buyers often discover too late: their bank isn’t thrilled about the rebuilt title, and their insurance quote is higher than expected. Neither of these is a dealbreaker, but walking in unprepared makes both feel worse than they have to be.

On the insurance side:

Many buyers have been told that insuring a rebuilt title car is nearly impossible. That’s simply not accurate. Most major insurance providers do insure rebuilt title vehicles. The nuance is that coverage terms may differ. Rebuilt-title insurance can be more expensive than coverage for a clean title vehicle, and some insurers may limit the types of coverage available or require additional documentation and inspection before extending a full policy.

What that usually means in practice: you may pay roughly 20% more for comparable coverage, and some providers may be more restrictive about comprehensive or collision protection. That said, this is far from universal. Shopping around matters. Get quotes from multiple providers before you commit to any vehicle purchase.

Here’s what to ask your insurance company before you buy:

- Do you insure rebuilt title vehicles?

- What coverage types are available for this vehicle?

- Will you require an independent appraisal or inspection?

- How is the payout calculated if the car is totaled? Is it based on rebuilt title market value?

That last question is important. Because rebuilt title cars are priced lower than clean title equivalents, insurance payouts are calculated against that lower market value. If a dealer has marked the car up significantly beyond what the rebuilt title market supports, you could pay too much upfront and receive less than you expected if you ever file a claim. Transparency in pricing matters for this reason too. See more on insurance for rebuilt title cars in 2026 for a fuller breakdown.

On the financing side:

Some lenders are straightforward about rebuilt title vehicles: they won’t finance them. Others will, sometimes with stricter terms or higher interest rates. As Experian points out, financing can be harder for rebuilt title vehicles, and if your plan depends on a lender, you should confirm approval and insurance requirements before committing to any purchase price.

Before you fall in love with a specific car, make those calls. Check financing options for rebuilt cars and review a rebuilt title financing guide so you know exactly what to expect. The best deal on a car doesn’t feel like a deal at all if the financing falls apart at the last minute.

Our perspective: The smart way to buy a rebuilt title car

Here’s something we’ve noticed. Most buyers either dismiss rebuilt title cars outright without ever reading a single document, or they get so excited about the price that they skip the due diligence entirely. Neither approach serves you well.

The buyers who actually win in this market are the ones who treat the process like a puzzle. They want to see every piece. They read the repair records. They hire an inspector. They call their insurance company before they shake hands on anything. They are, frankly, a little bit obsessive about it. And that obsession pays off.

The “rebuilt” label makes some people panic. We understand that reaction. But the honest truth is that many clean title cars on dealer lots have incident histories that no one has bothered to document. At least with a rebuilt title, the history is out in the open. You know what you’re working with. That transparency is something you can actually use.

The mistake isn’t buying a rebuilt title car. The mistake is buying any car without doing your homework. Our rebuilt car safety guide for 2026 walks through this in detail, and it’s worth a read before you get too far into any search.

If the paperwork checks out, the inspection comes back clean, your insurance is lined up, and your financing is confirmed, then what you have in front of you is a real opportunity. Don’t let an unfamiliar label talk you out of a good deal.

Take the next step with ReVroom

Buying a rebuilt title vehicle is genuinely one of the smartest moves a budget-conscious buyer can make, but only when you have the right tools and information in your corner. That’s exactly what we built ReVroom to provide.

ReVroom is the only online marketplace built specifically for rebuilt title vehicles, and every listing comes loaded with vehicle history information and photos of what the car looked like before it was repaired. No scrambling for reports. No guessing. No $150 vetting costs per vehicle. We put everything you need front and center so you can find the best vehicles, ask the right questions, and buy with confidence. Ready to see what’s out there? Start your search at ReVroom and let the transparency do the talking.

Frequently asked questions

Can I get full coverage insurance for a rebuilt title car?

Full coverage may cost more or come with restrictions, and some insurers limit comprehensive and collision options for rebuilt title vehicles, so always shop multiple providers and ask specifically about your coverage options. Insurers often charge more and may require documentation or a separate inspection before extending a full policy.

Do all states require a safety inspection before issuing a rebuilt title?

Nearly all states do require an inspection after repairs are completed before granting a rebuilt title, though the specific requirements vary by state. Per Experian’s overview, passing that inspection is what makes the vehicle legal to register and drive again.

Is it harder to finance a rebuilt title vehicle?

Yes, some banks and lenders have stricter criteria or may decline loans on rebuilt title vehicles, so confirming your financing options before committing to a purchase is essential. Experian specifically advises checking lender approval and insurance requirements before you agree to any price.

What documents should a reputable dealer provide when selling a rebuilt title car?

A trustworthy dealer should provide a statement explaining the cause of the total loss designation, itemized repair records with receipts, the official state inspection certificate, and a third-party vehicle history and recall report. Experian’s framework outlines all four of these as non-negotiables before you pay a deposit on any rebuilt title vehicle.

Are rebuilt title cars always unsafe?

No. A rebuilt title car that has been properly repaired and has passed a state safety inspection can be a safe and reliable vehicle. As Experian explains, these cars have been through a documented repair and inspection process, though as with any used vehicle, thorough due diligence before purchase is always the right call.